Open skies

Interest rates have started to head south again and investors are bracing themselves for another bout of late-cycle volatility. If the Federal Reserve (Fed) continues to cut interest rates, the current cycle’s peak – a mere 2.5% – will be the lowest in the history of the federal funds rate.1 And while the injection of liquidity appears to have calmed markets, uncertainty about the length and outcome of the US-China trade war is likely to cause turbulence.

We think that a flexible approach can help investors access the most attractive parts of the credit spectrum in this low-yield environment. Investors can search credit classes and capital structures to invest in the most attractive instruments with conviction and establish defensive positions amid the constant threat of volatility.

The returns of flexible-credit funds have drivers across geographies, sectors and instruments, which allows investors to access an increasingly globalised credit market. In a world where the global stock of negative-yielding bonds stands at $17tn, investors need access to a variety of instruments to capture income.

Flexibility can also help investors achieve a level of downside protection during periods of instability and reduced liquidity. Unconstrained strategies can preserve capital by allocating to less risky parts of the market or using defensive option-based strategies during sell-offs, enabling them to take advantage of opportunities when valuations inevitably become distressed.

Investors taking a flexible approach have been rewarded by superior risk-adjusted returns. The aggregate Sharpe ratio2 of flexible bond funds is higher than that of government, corporate and high-yield bonds (see figure 1).

Figure 1: Looking Sharpe

Bond funds, 2009-2019, % | ||

|---|---|---|

Annualised returns | Sharpe ratio | |

Government | 2 | 0.3 |

Corporate | 4.4 | 0.8 |

High yield | 8.4 | 1.1 |

Flexible | 4.8 | 1.2 |

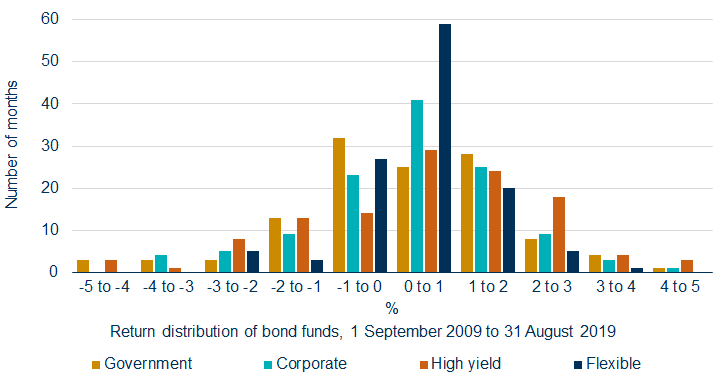

Moreover, a flexible approach adds value more consistently. While high-yield funds have the potential to generate larger returns, flexible bond funds have made more frequent gains and delivered positive returns in a greater number of periods over the past decade (see figure 2).

Figure 2: A smoother journey

Asset flows: floods and drought

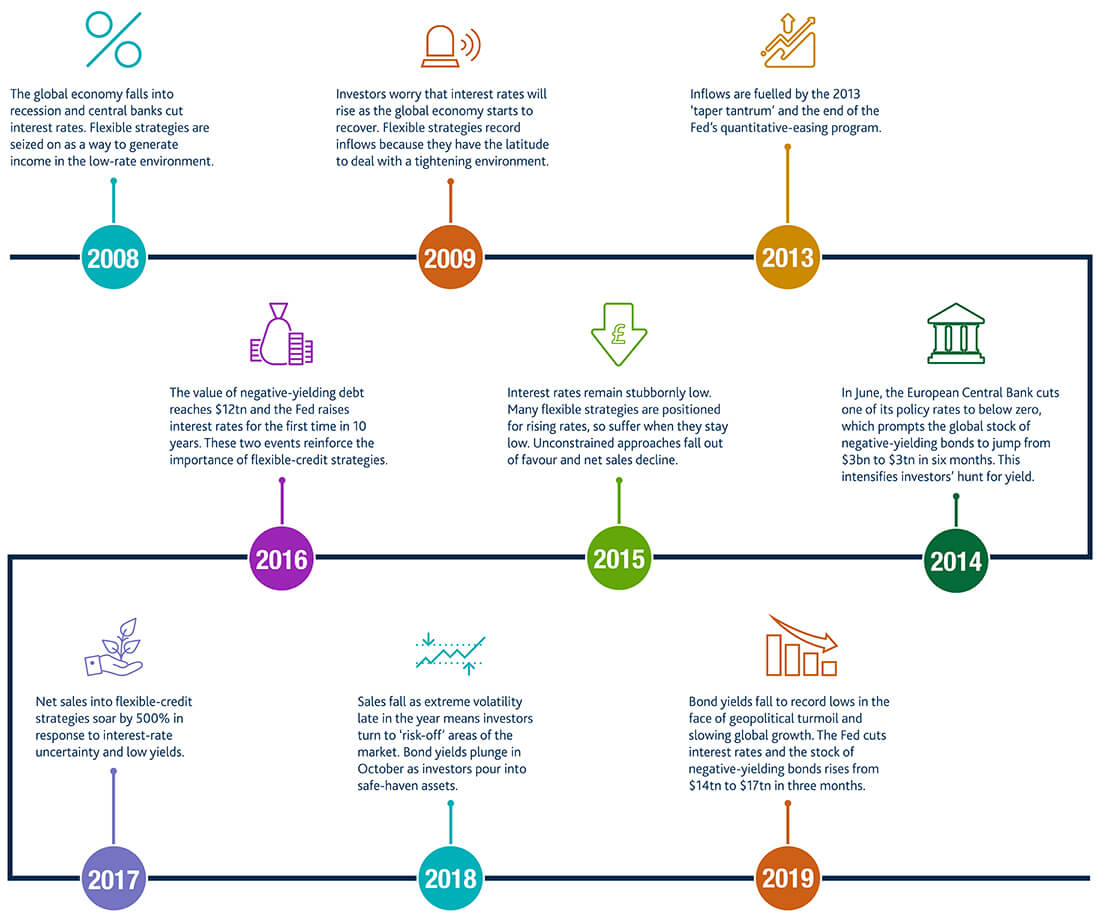

Many investors focused on flexible strategies after the financial crisis. Central banks across the world cut interest rates, prompting investors to search for ways to generate income in the low-yield environment. When interest rates hit rock bottom in 2009, anxiety about tightening monetary policy boosted further inflows into flexible strategies as investors sought to manage duration risk (see timeline).

Freedom: the evolution of flexible credit

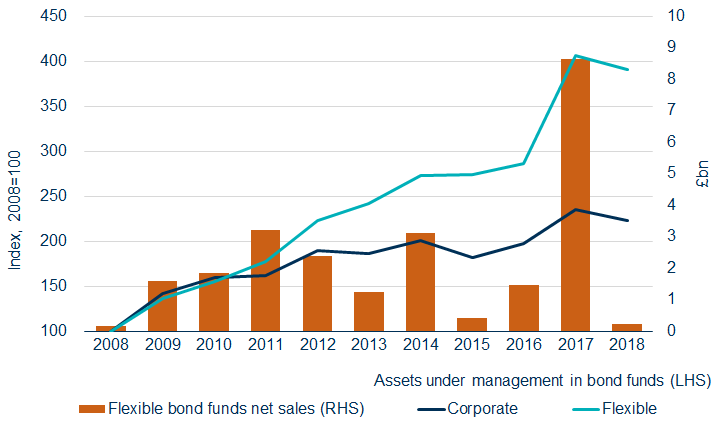

While sentiment towards flexible strategies has fluctuated over the past decade, their go-anywhere approach has boosted their overall popularity. The assets under management in flexible-credit strategies have risen at almost double the pace of those in corporate bond funds over the past decade (see figure 3).

Figure 3: Flex appeal

Storm clouds gathering?

A flexible approach is more relevant than ever in a world where the stock of negative-yielding debt has reached $17tn, jumping by 20% since the Fed cut interest rates in July. The Fed’s move also allows the European, Chinese and Japanese central banks to continue with monetary-policy easing, which suggests the lower-for-longer environment is here to stay for some time. Demand for spread products has risen, as investors scan the length and breadth of the credit spectrum for instruments that have the potential to deliver income.

As well as helping to generate incremental yield, a flexible approach can offer value during periods of uncertainty by using downside protection and capturing dislocation in the market. This was apparent at the end of last year, when the late-2018 sell-off created opportunities for active managers to seek alpha by investing throughout different regions, sectors and instrument types.

Although volatility eased over the first half of this year, calm might not prevail. We are in the latter stages of the macroeconomic cycle, with a classic recessionary indicator – US 10-year bond yields falling below two-year yields – flashing for the first time since 2007. Realised volatility has exceeded implied volatility on several occasions this year, a phenomenon that typically precedes a crisis. It seems increasingly possible that there will be another bout of panic in credit markets before 2019 is over.

The reduction in liquidity across credit markets since the financial crisis is also likely to exacerbate any sell-off. The ability to preserve capital is important, as long-term government-bond yields are unlikely to provide much of a cushion in the event of a liquidity shock. We believe that flexibility always has a place, but its capacity to provide downside protection and enhanced liquidity makes it particularly important in this late-cycle environment.

While volatility is likely to rise, a sustained downturn could be some way off. CCC-rated instruments have underperformed this year, as investors have been unwilling to lend to lower-rated issuers in the face of macroeconomic uncertainty. This discipline among lenders is a welcome sign, particularly given that the hunt for yield is more intense than at any point in history given the record-high volume of negative-yielding debt and historically low levels of interest rates.

Last year’s sell-off also prompted issuers to take creditor-friendly actions and cut dividends and sell assets. The dispersion of spreads among instruments has increased, and we see opportunities for active managers to seek alpha by distinguishing between lower-rated issuers and mid-quality companies that have taken steps to preserve capital. The outlook may be uncertain, but we think that a flexible approach will help investors identify and capture the opportunities that exist late in the cycle.

All weather: our approach to flexible credit

At Hermes, we look for opportunities across the global credit spectrum, targeting attractive returns throughout market cycles while preserving capital. We believe that security selection is as important as finding the right company and search the capital structures of issuers for attractive instruments. Our large-cap bias helps us access better liquidity, while our persistent emphasis on downside protection means we are able to find opportunities when markets are fearful. There are four main aspects to our approach to credit investing (see figure 4).

Figure 4: The defining themes of Hermes’ flexible approach to credit investing

Source: Hermes, as at August 2019.

Through seasons and cycles

In these late-cycle conditions, a flexible approach to credit investing can help investors navigate – and benefit from – turbulence in order to generate attractive capital returns and income. And once this stage of the cycle has ended, these strategies can adapt to the next. Now that we have assessed the main drivers of flexible-credit investing, we will focus on unconstrained allocation across the credit spectrum – which is the second instalment of this series.

Share:

Risk profile

Past performance is not a reliable indicator of future results.

The value of investments and income from them may go down as well as up, and you may not get back the original amount invested.

Targets cannot be guaranteed.

It should be noted that any investments overseas may be affected by currency exchange rates.

This information does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.

Where the strategy invests in debt instruments (such as bonds) there is a risk that the entity who issues the contract will not be able to repay the debt or to pay the interest on the debt. If this happens then the value of the strategy may vary sharply and may result in loss. The strategy makes extensive use of Financial Derivative Instruments (FDIs), the value of which depends on the performance of an underlying asset. Small changes in the price of that asset may cause larger changes in the value of the FDIs, increasing either potential gain or loss.