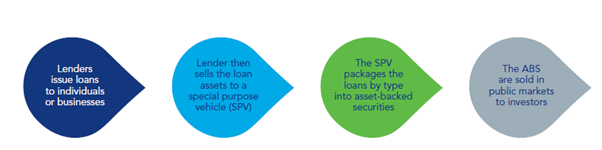

ABS are financial instruments backed by a pool of assets, such as loans, leases, credit card debt or receivables. These assets generate cash flows, which are used to pay investors in the securities. ABS are created through a process called securitisation, where the assets are pooled together and sold to a special purpose vehicle (SPV), which then issues the securities. These securities then trade in fixed-income markets.

The value of ABS

Asset-backed securities are an important part of the financial system, providing liquidity and funding for a range of consumer and commercial loans and leases.

ABS offer a way for lenders to free up capital and for investors to gain exposure to different types of assets. They play a crucial role in the financial ecosystem by enhancing liquidity and providing investment opportunities.

What value can ABS bring to low duration portfolios?

- Reduced principal risk: ABS have strong structural features such as excess interest, overcollateralisation, reserve accounts and subordination designed to protect bondholders from collateral losses.

- Liquidity: These securities are typically structured to provide regular cash flows, which can make them suitable for portfolios with liquidity objectives.

- Competitive yields: ABS can offer higher yields compared to other short-term fixed-income instruments, providing an attractive return for low duration portfolios.

- Maturities: The weighted average life (WAL) of ABS tends to be relatively short, usually 1-4 years. The combination of the short WAL and amortising bonds that receive monthly payments can be an appropriate fi t for short duration portfolios.

Figure 1: ABS creation process

Understanding asset-backed securities (ABS)

BD016086