Emerging markets have lagged developed markets this year by 6%, with China reflecting the most notable drag at -26%. However, China stocks are enjoying something of a ‘Santa rally’ amid hope Beijing will relax its strict Covid-19 measures and fully reopen its economy.

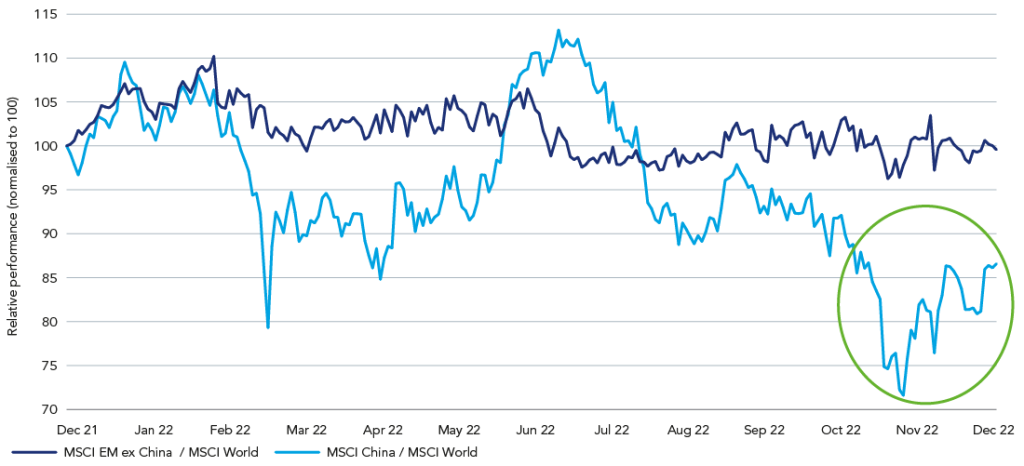

The MSCI China Index jumped by 29% in November1 to deliver its best monthly return since 2009, shown in figure 1 below; a ‘perceived U-turn’ in the country’s draconian Covid policies drove the market. While markets were initially volatile following the 20th Party Congress last month, which saw President Xi Jinping reinstated for an unprecedented third term, the Beijing government has since made clear moves to better support the economy.

Figure 1: MSCI EM ex-China Index and China relative, year-to-date

Source: Datastream, as at 2 December 2022.

Reopening and stabilisation of property sector are key near-term drivers

We have seen constructive policy changes on multiple fronts, including a major push on vaccinations, more flexible quarantine rules in several major cities including Beijing and Guangzhou, removal of regular PCR testing requirements in selective cities, and seemingly better cross-province mobility with less onerous checks at major airports and train stations. While current Covid-19 guidelines in China appear inconsistent, with municipalities adopting different approaches to loosening lockdown, and on differing timeframes, it is clear overall the country is preparing for a more meaningful reopening.

Investor sentiment has also been boosted by recent measures announced to support China’s ailing property sector. A 16-point rescue plan2 was jointly issued by the People’s Bank of China (PBOC) and the China Banking and Insurance Regulatory Commission (CBIRC), directed at supporting financing for developers. Last month’s meeting between US President Joe Biden and Xi Jinping also bolstered hope that better cooperation between the two countries could reduce the risk of delisting of hundreds of Chinese companies from the US.

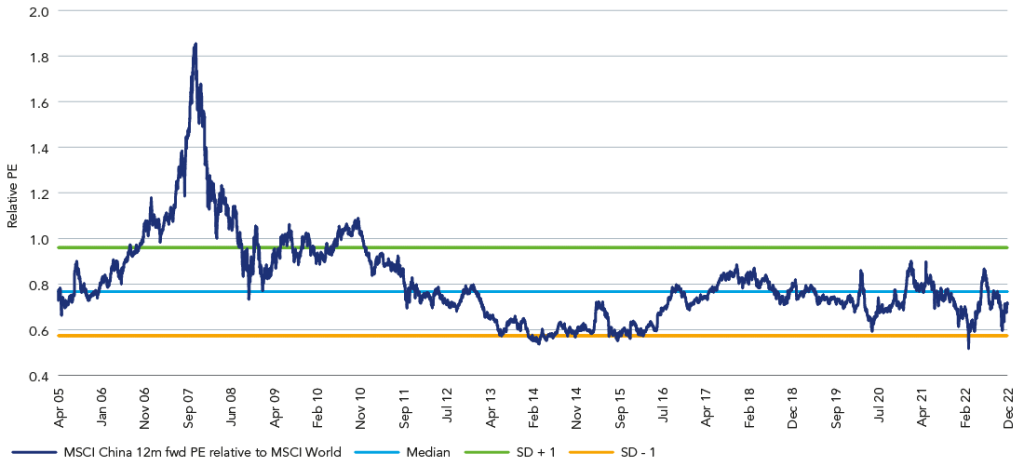

Despite this, investors have had many reasons to sell China. The risk-reward for Chinese equities looks attractive, with the region down 15% relative on the year, as shown in figure 2 below, despite its recent rebound.

Figure 2: MSCI China Index 12-month relative to MSCI World Index

Source: Datastream, as at 2 December 2022.

Corporate decoupling

While reopening and cheap valuations are important for market sentiment, most corporates are cautious about expansion plans. The focus seems to be on managing costs and enhancing profitability. With the Communist Party policy favouring state-owned enterprises (SOEs), private companies are likely to be less aggressive on growth even when the environment normalises. It will be crucial to see how the Chinese economy performs beyond the reopening event, as a lack of meaningful private sector investment will hurt the economy over the medium to long term.

The Chinese economy is undergoing a deeper transformation that is exciting and presents unique investment opportunities for long-term investors

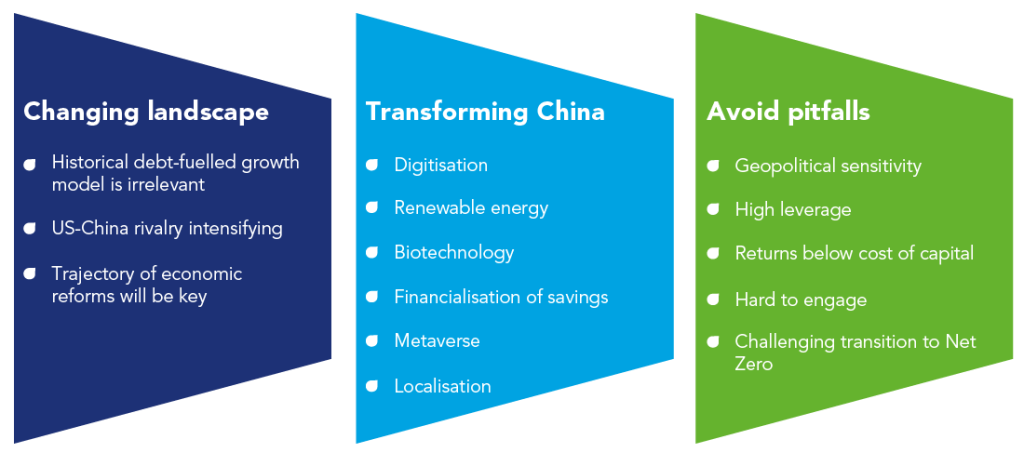

Transforming China

China is at a crucial junction with multiple challenges including geopolitical rivalry with the US, outbreaks of Covid and stress in the property sector to name a few. These are immensely challenging issues that will test the resolve of the Chinese leadership. In any case, the debt-fuelled growth model of the past is irrelevant now and historical valuation less meaningful. We are focused on how China is likely to evolve beyond the post-Covid re-opening trade. We believe that China at best can achieve a mid to low single digit real GDP growth considering the constraints under which the economy is operating.

Despite these challenges, underneath the surface, the Chinese economy is undergoing a deeper transformation that is exciting and presents unique investment opportunities for long-term investors. We believe focusing on the following themes will offer a long runway for growth in an economy that is largely ex-growth:

- Digitisation

- Renewable technologies and energy

- Biotechnology

- Financialisaton of savings

- Metaverse

- Localisation of critical technologies

Figure 3: Despite geopolitics and policy shifts, the Chinese economy will continue to transform

Source: Federated Hermes Limited, as at December 2022.

While the opportunity in these sectors is likely to be meaningful, it is important for investors to avoid pitfalls, some which are unique to China. This includes any sectors that can be associated with geopolitics, such as the US entity list. In addition, we are avoiding companies in cyclical industries as these are typically loaded with excessive leverage and generate returns below their cost of capital. Over time, we believe that such companies will likely find the transition to net zero very challenging.

While China has made commendable progress in multiple fields, there is potential for the economy to achieve more. However, progress in the future will depend on the pace of economic reforms and further opening of the economy. This will heavily depend on how quickly the Chinese leadership is able to reform its state-owned enterprises (SOE’s), making them competitive and relevant for the future.

Globally, economies rarely cross the USD 10,000 per capita income without reforms at an institutional level. China has already crossed this level thanks to its previous growth model, focus on exports, and infrastructure. As some of these drivers unwind, including property and excessive leverage, China will have to quickly assemble new drivers to sustain income levels and ensure a higher quality of life for its people.

For more information on Global Emerging Markets Equity please click here.

1 MSCI China Index, as at November 2022.

2 Bloomberg, as at 13 November 2022.