- Major Chinese cities, including Beijing, Wuhan and Shanghai, witnessed protests and demonstrations over the weekend, as citizens expressed frustration at Beijing’s handling of virus containment.

- On Thursday, a decision to ease lockdown measures in parts of the Southwestern trade and transport hub, Guangzhou, despite a surge in cases, indicates a change in policy direction.

- Market reaction has been cautiously positive amid evidence Beijing government may be listening to civilian concerns.

Investor faith faltered after the weekend’s events, with the Hang Seng Index dropping by 4.5% on Monday1. Financial markets have since changed course, interpreting the unrest as a possible catalyst for less draconian lockdown measures. Asian currencies rose in the early hours of Thursday morning, with the yen climbing 0.9% to ¥136 per US dollar2.

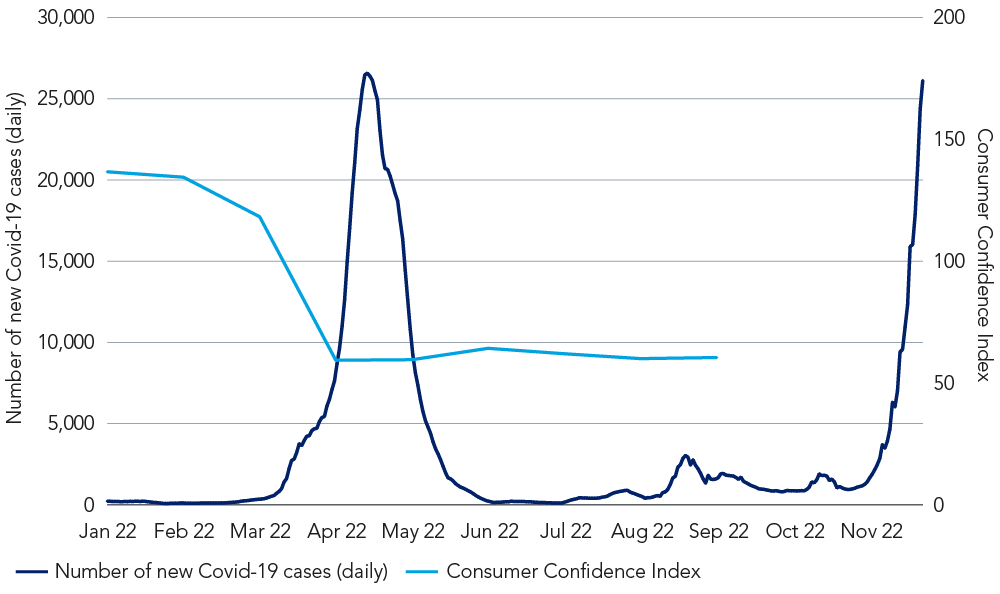

Consumer confidence in China has been on the wane as a result of the zero-Covid policy and its damaging impact on the economy. The consumer confidence index experienced a sharp drop in April following the Shanghai Covid outbreak, and has lingered in similar territory since.

Figure 1: China’s consumer confidence takes a nose-dive, while Covid cases spike

NB: The most recent available China Consumer Confidence Index data is from August 2022.

Source: Trading Economics, National Bureau of Statistics China, as at August 2022, and Our World in Data, as at 22 November 2022.

Silvia Dall’Angelo, Senior Economist at Federated Hermes Limited, believes current events will leave the Chinese government no choice but to consider a more serious pandemic ‘exit-plan’.

“The process will likely be gradual and bumpy over the year ahead, due to low immunisation of the population and unpreparedness of the health system to deal with a possible surge in cases. That said, and bar any major reversals, re-opening should gain traction in the second half of next year,” she says.

It will be crucial to see how the Chinese economy performs beyond the reopening event, as a lack of meaningful private sector investment and participation will hurt the economy over the medium to long term.

And while this move is positive for overall market sentiment, Kunjal Gala, Head of Global Emerging Markets at Federated Hermes Limited, says corporates are cautious about expansion plans. The focus, he says, will remain on managing costs and enhancing profitability as companies are likely to be less aggressive on growth even when the market stabilises. “It will be crucial to see how the Chinese economy performs beyond the reopening event, as a lack of meaningful private sector investment and participation will hurt the economy over the medium to long term,” he explains.

Elsewhere in global markets...

November has seen the headline rate of inflation decline in the eurozone for the first time in 17 months3, boosting hopes that the peak for price rises might be in sight and bolstering expectations the European Central Bank (ECB) will shift to smaller interest rate hikes next month.

Louise Dudley, Portfolio Manager, Global Equities at Federated Hermes Limited, warns investors to not be blinded by the marginally brighter outlook. “Though interest rate hikes seem to have achieved their goal of tempering inflation, we worry that higher borrowing costs and cost-of-living squeezes in major economies will lead to regional recessions in 2023. There could still be challenges ahead and we recommend maintaining a diversified portfolio partnered with diligent management of risk exposures.”

For Dall’Angelo, however, the broader inflationary outlook is positive. “Inflation should come down over 2023, and in particular in the second half of the year, owing to a stabilisation in energy prices and related base effects, the continued easing of global supply constraints and, crucially, a sharp demand slowdown, all of which should provide downward pressures.”

For further insights into global equities, please see our Sustainable Global Equity, Q3 2022 report.

1 The Financial Times, as at 28 November 2022.

2 The Financial Times, as at 1 December 2022.

3 The Financial Times, as at 30 November 2022.