Fast reading

- US interest rates were reduced by 50bps on Wednesday, with further loosening expected before the end of the year.

- The move marks the first cut in US borrowing costs since the Covid-19 pandemic in 2020.

- The Bank of England, meanwhile, held rates steady at its meeting on Thursday.

The first cut is the deepest

The US Federal Reserve (the Fed) slashed interest rates by 50bps on Wednesday, initiating its first easing cycle since the start of the Covid-19 pandemic. The move lowers the federal funds rate to a range of 4.75% to 5%.1

It follows other central banks, including the European Central Bank (ECB), which last week reduced borrowing costs to 3.5%, its second 25bps cut of the year. On Thursday, the Bank of England (BoE) voted to leave rates unchanged at 5%, after reducing rates by 25bps at its meeting in August.

While the Fed was widely expected to loosen policy, there has been debate about the size of the reduction at this week’s Federal Open Market Committee (FOMC) meeting. US inflation fell to 2.5% in August, according to data released last week.

Fed Chair Jerome Powell said the bold action was needed to stop high borrowing costs from negatively impacting the US economy. The timing of the Fed’s move is significant – with the US presidential election in less than two months.

A shot in the arm

Stock markets rallied following the move. The blue-chip S&P 500 Index gained 1.2% to close at 4,839.80 on Thursday, hitting an all-time high, while the tech-heavy Nasdaq Composite closed above 15,300 for the first time since 2022. In Europe, FTSE 100 closed at 8,318.77 and the pan-European Eurostoxx 600 ended the day at 521.42.2

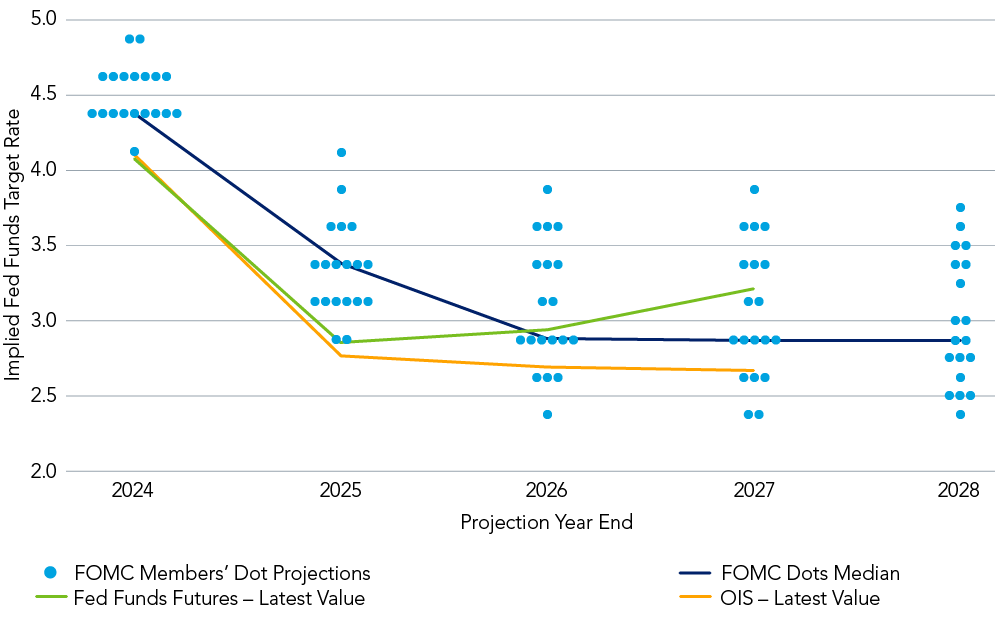

The Fed’s ‘dot plot’ – which illustrates where FOMC officials anticipate rates are heading – suggests further loosening is on the cards before the end of the year (see Figure 1).

Figure 1: Implied Fed funds target rate

When rates are gradually lowered, money market funds typically lag behind the direct market, and institutional clients, in particular, tend to increase their holdings.

A falling rate environment

Despite the cut in US rates, the outlook for money market funds remains buoyant, says Deborah Cunningham, Chief Investment Officer for Global Liquidity Markets at Federated Hermes.

“When rates are gradually lowered, money market funds typically lag behind the direct market, and institutional clients, in particular, tend to increase their holdings in these funds while decreasing their exposure to direct securities,” she says.

“We do not expect a mass exodus of cash from money market funds as rates fall and the historical data supports this — unless interest rates approach zero, which we don’t anticipate in the current climate,” she says.

“Should rates fall to around 3% — or even 2.5% in the euro area — we anticipate an increase in assets under management for money market products globally.”

Mini budget lessons

Elsewhere, investors are looking ahead to the first budget statement under the UK’s new Labour government on 30 October.

“The sensitivity of markets was exposed by the fallout from the mini-budget (under former prime minister Liz Truss in Autumn 2022) even in a strong and stable economy like the UK,” notes Louise Dudley, Portfolio Manager for Global Equities at Federated Hermes Limited, as she reflects on lessons learned from the crisis two years on.

“The instability and the geopolitical risks were heightened to levels unseen following Brexit, and the period was a difficult one to navigate with the cost-of-living crisis underway and energy prices at elevated levels. The uncertainty around the persistence of the inflationary environment had investors on high alert and the mini-budget did nothing to promote confidence in the government’s decision-making going forward,” she adds.

“Markets have certainly moved on from this period and the UK economy has resumed a more stable path with investment resilient through 2024. However, the upcoming UK Autumn budget is currently hanging over the market and banks as we await the changes from the new government which are likely to squeeze voters’ pockets.”

For further insights on global equities please see: Global Equity ESG, H1 2024 Report.