- Investor fears grow that pace of monetary policy tightening will tip the US into a recession, the impacts of which could outweigh the risks of inflation.

- The BoE forecast the UK is facing a two-year recession that could see unemployment almost double by 2025.

The Bank of England and the US Federal Reserve both raised interest rates by 75 basis points this week, following the European Central Bank’s 75bps hike last week, as central banks around the world resort to increasingly aggressive policy responses as they battle to contain runaway inflation.

The Fed’s move on Wednesday was the fourth 75bps rise in a row, bringing the federal funds rate to a target range of 3.75% to 4%1. The BoE’s rise on Thursday was the largest increase in three decades, bringing UK interest rates to 3% as the central bank warned the country faced a two-year recession that could see unemployment almost double by 20252.

“Central banks are in aggressive tightening mode across the board, as the fight against high inflation is not over. They are acting forcefully to prevent second-round effects – high and persistent inflation risks becoming entrenched against the backdrop of a tight labour market,” says Silvia Dall’Angelo, Senior Economist at Federated Hermes Limited. “Ever-evolving data will continue to define not only the pace of tightening across the board but also the destination for the current tightening cycle.”

Following the 75bps hike, BoE governor Andrew Bailey signalled he did not expect rates to rise too much further as the energy price shock and UK government fiscal tightening add to downward pressure on inflation. The market expects rates to peak at about 4.75% during autumn next year, a forecast Mr Bailey suggested may be too high.

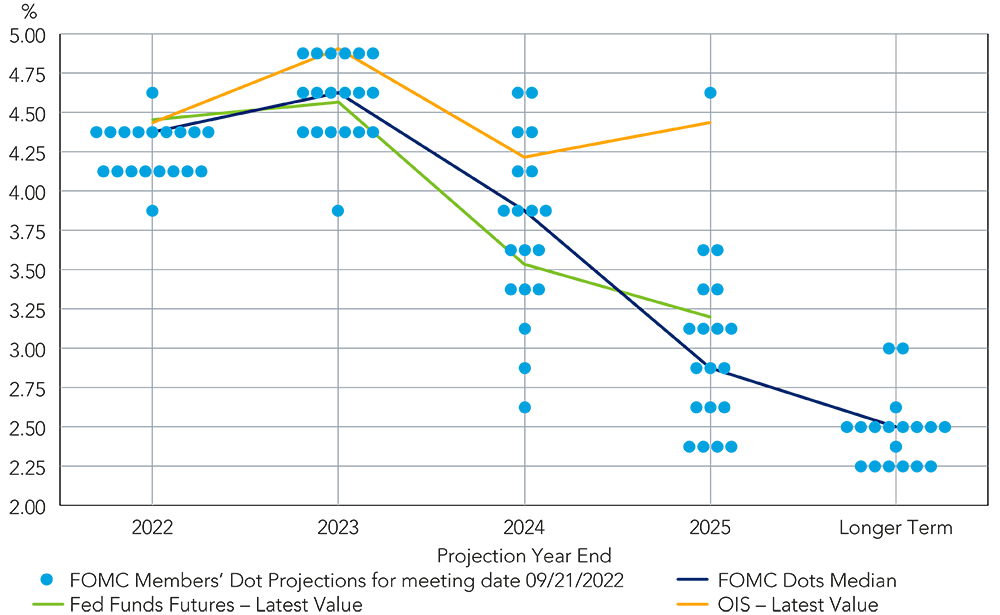

The Federal Reserve, meanwhile, looks likely to hike rates by a slower pace of 0.5% in December to a year-end range of between 4.25% and 4.5%, followed by one or two 0.25% rate hikes in early 2023 to a terminal rate of almost 5%, according to Dall’Angelo. However, it’s unlikely the Fed will be able to start an easing cycle next year, as inflation will likely remain above target through 2023, she says.

Figure 1: Implied Fed funds target rate

Market unease

The S&P 500 closed down 2.5% on Wednesday, following hawkish comments from Fed chair Jay Powell, while the yield on the two-year US treasury note stood at 4.7% at 16:30 GMT on Thursday, its highest level since 20073.

“Investors are worried that the pace of tightening of monetary policy will tip the US into a recession, the impacts of which they fear would far outweigh the risks of inflation,” says Geir Lode, Head of Global Equities, Federated Hermes Limited.

Following the BoE’s hike, the UK blue-chip FTSE Index closed up 0.54% on Thursday while the pan-European Stoxx Europe 600 fell 0.93%. The FTSE 100 is down 2.73% year to date. The yield on the 10-year UK gilt edged up to 3.51%4.

“This monetary policy tightrope-walk of inflation vs. recession faced by central banks is a key driver in most developed markets at the moment, and we are seeing larger-than-expected factor movements compared to historic returns,” Lode says.

“This macro risk and heighted factor volatility confirm our view that a diversified investment approach is key to navigating these markets.”

For further insights on global credit markets, please see the latest Q3 360° report on rates, recovery and recession.

1 The Fed hikes US interest rates to fresh 14-year high – BBC News

2 Bank of England raises interest rates by 0.75 percentage points | Financial Times (ft.com)

3 Bloomberg as at 3 November

4 Bloomberg as at 3 November