“America,” according to the US Cricket Board, “has one of the richest cricketing histories of any countries in the world, dating back over 300 years.” 1

While that statement might come as a surprise to fans of the modern game, the bold historical claim by the recently formed governing body of the sport in America speaks to the boundless optimism and commercial savvy the country is built on.

The US Cricket Board notes that 10-20m Americans could follow the game, and “with the commercial maturity of the US sporting landscape and the relative affluence and digital connectivity of our cricket fans, there is great potential to grow and engage with new and existing fans and players”.

But the cricket body’s plan to hit ambitious targets by pitching to US shoppers is likely more than spin. Over the last few decades, the US consumer has been (and still is) one of the strongest drivers of the world economy. There’s no reason why cricket can’t help boost this run rate.

And the consumer – or more specifically, consumer debt – offers investors a good way to test the health of the US economy.

The most recent data show that in one of the most disruptive years in living memory, the US consumer is playing remarkably well. For example, consumer-loan asset quality remained solid during Q3 despite high unemployment and the end in July of the $600 special COVID-19 benefit top-up to those out of work.

Overall, the firm performance of US consumer debt during the September quarter reflects large-scale loan forbearance programs, direct stimulus payments to individuals and reduced spending.

As we move into the last innings of 2020, however, US consumers could be about to face a tougher pitch as the economic cracks exposed throughout the year widen further.

Marking out the field: loans cross new boundaries

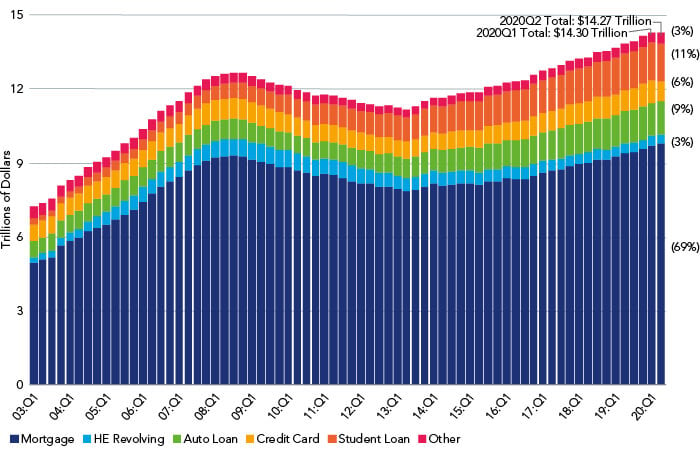

As the end of June this year, the New York Federal Reserve reported outstanding US consumer debt of $14,27tn.

Figure 1. Big hitters: volume and composition of US consumer debt

Source: New York Consumer Credit Panel and Equifax as at December 2020.

Both banks and non-bank financial firms have large exposures to the US consumer-debt market, but the latter sector provides a more illuminating view of underlying risks.

The global high-yield (GHY) index, for example, includes three large US ‘specialist lenders’ 2 that require thorough due diligence from credit investors, namely:

- ALLY, a $180bn bank regulated by the Federal Reserve and active mostly in the auto-loan market (62% of loans);

- OneMain Financial (OMF), a $23bn nationwide franchise of personal loans; and,

- Navient, the $81bn student loan giant.

Due to their diverse product mixes, it can be difficult to categorise these all-rounder firms in the non-bank sector. However, by focusing on the vertical product lines of instalment lending and student loans we can glean some insight into the state of play in the market. For instance:

- Instalment or personal loans can either be secured (by auto or title), or unsecured.

- At 68%, mortgage debt is the largest of the household balance sheet items, followed by student loans with 11%, auto loans at 9% and 6% for credit-card debt.

- Both student and auto debt have grown significantly since June 2010, when the two sectors each represented 6% of the US consumer loan pile.

According to TransUnion, a US consumer-credit reporting agency, banks held 30% of auto-loan originations at the end of June this year, almost on par with the 31% carried by auto manufacturer-linked lending. Credit unions, with 20%, and ‘non-captive’ finance companies, at 12%, made up the difference.

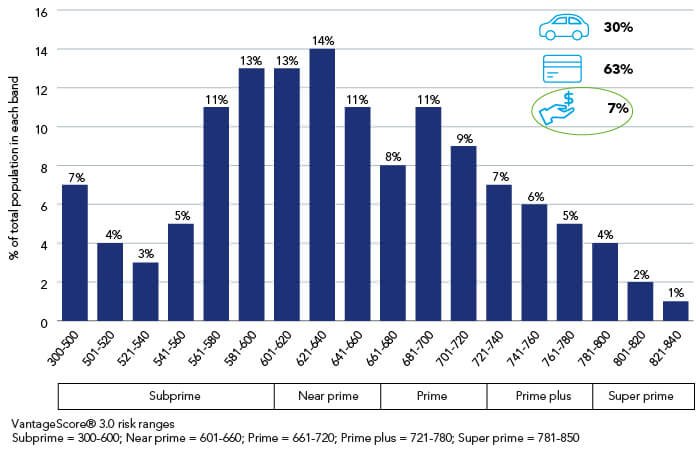

At the end of 2018 most US personal loans fell into the sub-prime to near-prime categories (see figure 2).

Figure 2. Sub-prime borrowers at the crease

Source: TransUnion at November 2020.

Experian, another company specialising in monitoring consumer debt, calculated that the average FICO score – a popular measure of US consumer creditworthiness produced by a private company – stood at 703 as at June 2019. A good FICO score “starts at 670”, the company says, while consumers with a rating above 740 “can generally expect lenders to offer [them] better-than-average interest rates”. (See references for FICO score ranges.)

Figure 3. Keeping score: growth in US consumer debt across sectors since 2009

Growth by debt type since 2009 | |||

|---|---|---|---|

Type | Total debt 2009 | Total debt 2019 | % change |

Mortgage | $8.4tn | $9.6tn | +14% |

Auto loan | $716bn | $1.3tn | +81% |

Student loan | $658bn | $1.4tn | +113% |

Credit card | $700bn | $829bn | +18% |

HELOC | $729bn | $420bn | -42% |

Personal loan | $237bn | $305bn | +29% |

Retail card | $59bn | $90bn | +51% |

Source: Experian as at November 2020.

As figure 3 shows, almost all US consumer-debt sectors reported year-on-year growth during the 2019 financial year. Experian tells us that consumers ended play with the following per capita averages:

- mortgage balance: $203,000;

- student debt: $36,000;

- auto loans: $19,000; and

- personal lending: $16,000.

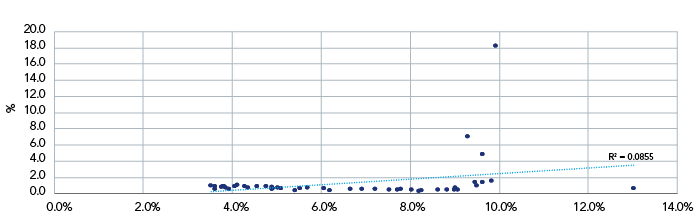

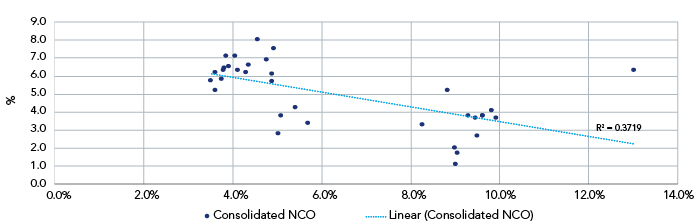

Economic theory (and common sense) holds that, similar to the likelihood of bowling out a tail-ender in an entire session of play, there should be a strong correlation between the unemployment rate and asset-quality deterioration in the non-prime credit sector.

Correlations typically increase in times of stress, after all. Contrary to theory, our analysis of asset quality for both ALLY (featuring a higher proportion of near-prime loans) and OneMain Financial (which leans more to the sub-prime sector) since the second half of 2009, failed to find a strong correlation between unemployment and asset quality as measured by net charge-off rates, or NCO, which is a proxy for expected unrecoverable debt (see figure 4).

In fact, based on regression analyses (R-squared), we found only weak correlations of 0.08 and 0.37 for ALLY and OneMain Financials respectively over the period under review (see references for calculations).

Figure 4. Solid run rates, so far: non-prime US consumer debt is withstanding rising unemployment

ALLY: annualised NCO relative to national unemployment

OneMain Financial: annualised NCO relative to national unemployment

Source: ALLY and OneMain Financial data, Federated Hermes at November 2020.

The next innings: is consumer debt on a sticky wicket?

As the pandemic shut down large parts of the US economy earlier this year, consumer lenders adopted large-scale debt forbearance policies for people suffering financial stress. But now, almost nine months on from the first innings of the coronavirus crisis, lenders have started to tighten the criteria for granting debt relief. For example, some require more details from consumers on their financial situation before extending forbearance periods.

Over the coming months and quarters, we will be keeping a close eye on the following three key US data points as they pitch up on what looks like a turning wicket:

- changes in unemployment rate and composition;

- the conversion rate of forbearance into delinquencies; and,

- whether more delinquencies transition into NCOs.

English cricketing legend, Geoff Boycott, who scored more than 20 centuries during his international career, was asked on turning 80 years old this October which of his batting performances he was most proud of.

Wisely, Boycott replied that there is plenty of satisfaction in making lower scores on a difficult pitch.

Richard Feynman, US physicist

References

FICO® scores | Detail and region |

|---|---|

740 to 799. | Very good |

670 to 739. | Good |

580 to 669. | Fair |

300 to 579 | Very poor |

Source: Experian as at November 2020

Regression analyses

Ally Regression statistics | |

|---|---|

Multiple R | 0.292437663 |

R Square | 0.085519786 |

Adjusted R Square | 0.064736145 |

Standard Error | 0.026965671 |

Observations | 46 |

Analysis of variance | |||||

|---|---|---|---|---|---|

df | SS | MS | F | Significance

F | |

Regression | 1 | 2.36392E-06 | 2.3639E-06 | 2.75335 | 0.117807731 |

Residual | 15 | 1.28784E-05 | 8.5856E-07 | ||

Total | 16 | 1.52424E-05 |

OneMain Financial

Regression statistics | |

|---|---|

Multiple R | 0.609808521 |

R Square | 0.371866432 |

Adjusted R Square | 0.352237258 |

Standard Error | 0.014544522 |

Observations | 34 |

Analysis of variance | |||||

|---|---|---|---|---|---|

df | SS | MS | F | Significance

F | |

Regression | 1 | 0.004007595 | 0.004007595 | 18.94457871 | 0.000128859 |

Residual | 32 | 0.00676938 | 0.000211543 | ||

Total | 33 | 0.010776976 |

1 “History of cricket in USA,” published by US Cricket at https://www.usacricket.org/history/. Accessed in November 2020.

2 Sources: ALLY, OneMain Financial and Navient reports at 30 September 2020.