1. Macro recovery fuels rebound in commodity prices

In April 2020, oil futures prices collapsed into negative territory amid a coronavirus-induced supply glut. However, after a year of unprecedented volatility, oil prices have recouped their losses, returning to their pre-pandemic levels, and are currently lingering at $60 per barrel. This strong recovery has been driven by three factors:

- An economic recovery: global GDP is expected to grow by about 6% this year driven by vaccine rollouts and widespread stimulus packages;

- Market rebalancing: OPEC and its allies, known as OPEC+, have played an active role in balancing oil markets by making radical production cuts. Indeed, OPEC+ continues to take a cautious approach – and after accounting for the easing of production cuts due to begin in May, there will still be 6m barrels of oil per day that will remain off the market; and

- Oil demand recovery: the easing of lockdown restrictions and, in turn, the opening of economies should spur a recovery in oil demand.

Together, these factors are keeping the global oil market slightly undersupplied for now, with inventories being drawn every day and higher prices being supported.

2. A shift in behaviours can drive improvements in credit metrics beyond pre-crisis levels

Higher commodity prices are helping oil and gas producers. But for most producers, things are different this time. Despite the improving pricing environment, they are not increasing capital expenditures this year following substantial cuts in 2020. In the past, producers would generally respond to a rising pricing environment by increasing their capital expenditure. In our view, such a shift in behaviour is being driven by the industry’s need to demonstrate its ability to generate free cash flows on a recurring basis – something that has been missing in the past and has resulted in substantial equity underperformance relative to market indices over the last 10 years. We are also observing a change in management compensation initiatives: they are now focusing on free cash flow generation, shifting away from absolute production growth.

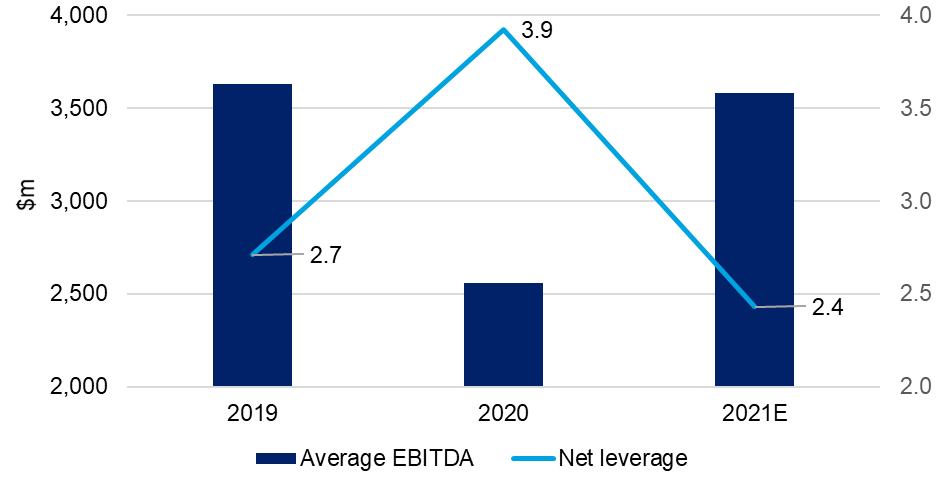

Looking at a sample of our exploration and production holdings within our credit portfolios, it is expected that this shift in behaviours coupled with an improved operating environment and the implementation of self-help measures in 2020 (that is, cost reduction efforts, the elimination of dividends, in some cases, and a focus on preserving balance sheet strength) will translate into 50% EBITDA growth year-on-year. Leverage is also expected to decline from 4x as of year-end 2020 to 2.4x by the end of 2021. This compares to leverage of 2.7x as at 31 December 2019 (see figure 1).

Figure 1. E&P earnings and metrics are set to recover this year

Source: Company Financials, Bloomberg, as at April 2021.

3. An expected improvement in fundamentals bodes well for valuations

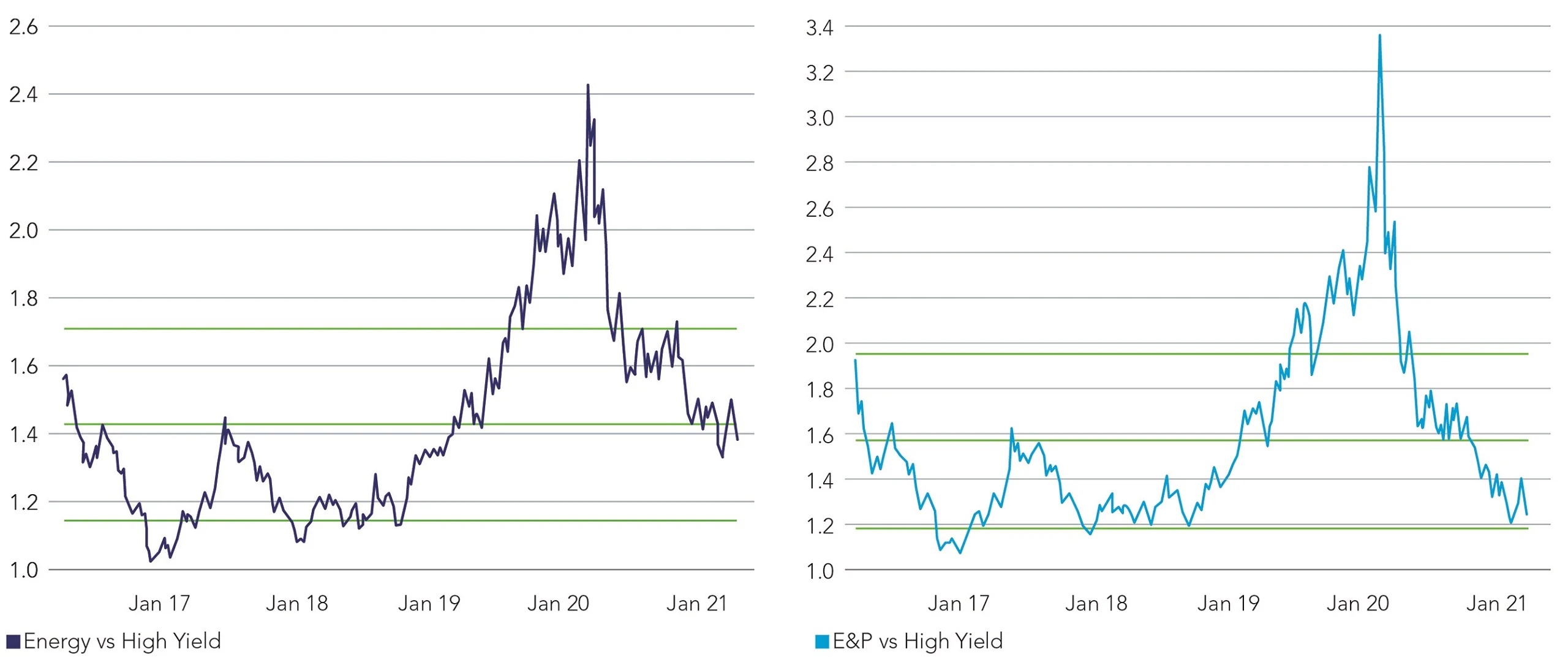

In the last six months, corporate credit spreads for firms in the energy sector have come in from the wides reached in 2020 and are currently trading in line with their five-year historical average relative to the index, thereby offering limited upside going forward. Figure 2 indicates that producers – excluding mid-stream and oil field services companies – are trading rich to the index. This can be explained by the addition of fallen angels – that is, credits downgraded from investment-grade status – to the high-yield index, which are trading at relatively tighter levels.

In response to this strong performance, we have been reducing some of our energy exposure. However, we also recognise that some high-conviction ideas offering further upside remain. Most of these ideas relate to fallen angels that have the potential to return to investment-grade status and benefit from scale, a high-quality asset base, M&A transactions as well as the potential for substantial deleveraging owing to the improved operating environment.

Figure 2. Energy valuations have come in from the wides of 2020

Source: Barclays Live. For illustrative purposes only.

4. Rising regulatory risks: manageable in the near term, adverse longer-term implications

As we have mentioned already, we have been reducing our exposure owing to valuations. At the same time, we have become increasingly concerned about the increased regulatory burden following the inauguration of the new administration, led by President Joe Biden, in the US. So far, we have focused on:

- The imposition of a one-year pause on leases on feral lands – both onshore and offshore;

- The re-establishment of an interagency working group to study the social cost of greenhouse gasses (GHG) in the US which suggests it will become increasingly important for investors to understand and quantify the exposures of companies to carbon emissions going forward; and

- The proposal to eliminate $35bn of fossil fuel subsidies over the coming decade, as outlined in Biden’s proposed infrastructure plan.

Overall, we view these developments as net negative, but manageable in the near term as companies have been preparing for some of these regulatory changes. However, it is likely that further regulatory restrictions will be imposed on the industry as efforts to combat climate change intensify – and we believe they will act as a headwind in the long term.

5. The energy transition: initiatives accelerate

In response to rising regulatory risks, oil and gas producers have been proactively addressing the energy transition by establishing a myriad of initiatives. For example, a number of producers have announced more ambitious GHG reduction targets. Meanwhile, some natural gas producers are shifting to responsibly sourced natural gas production – or simply put, production certified by third parties to meet stringent environmental and social requirements – and US majors are discussing ideas about public-private enterprises to develop carbon capture mechanisms.