Safety first

In 2019, much of the news flow was dominated by the stock markets’ longest – and best ever – bull market in history. But arguably, bonds have been on a general upward trend for much longer (the global bond bull market began in 19851). Despite a few significant setbacks, bond prices have risen, and yields have declined for the best part of four decades.

During this time, low interest rates (major central banks reversed course last year and are once again in easing mode), subdued inflation and muted global growth have prompted investors, searching for ways to generate income in the low-yield environment, to buy longer, riskier durations and rely on diversification for protection. And although this backdrop is unlikely to change just yet, vigilance is necessary. That’s because if the market enters periods of tumult in the future multiple lines of defence – not just rates and duration – will be needed to navigate it successfully.

Positively negative

Over the past century, there have been many stock-bond correlation regimes: the rolling three-year correlation was positive from the mid-1960s to 1998, but it has been almost entirely negative since the late 1990s (see figure 1a).

This regime change has been driven by a subdued inflation environment over the past 25 years. Indeed, this can be demonstrated by comparing the correlation of bonds and equities and inflation-linked bonds (real rates) and equities (see Figure 1b). Owing to an environment of low interest rates and disinflation, investors wishing to hedge their credit exposure have used rates, accepting much longer, riskier durations in exchange for yield.

Even though longstanding predictions of the end of the bull market (which started after former Federal Reserve Chair Paul Volcker quashed inflation in the 1980s) have not materialised, it can’t last forever. As such, actively managing duration is therefore important, but investors should not rely on the relationship between interest rates and risk assets to provide protection. This would be a threat to capital in a rising-rating environment.

Figure 1: The yin and yang of financial markets

Source: Bloomberg as at 31 July 2019.

From defence to offence: building a multi-faceted strategy

Diversification: still on the menu?

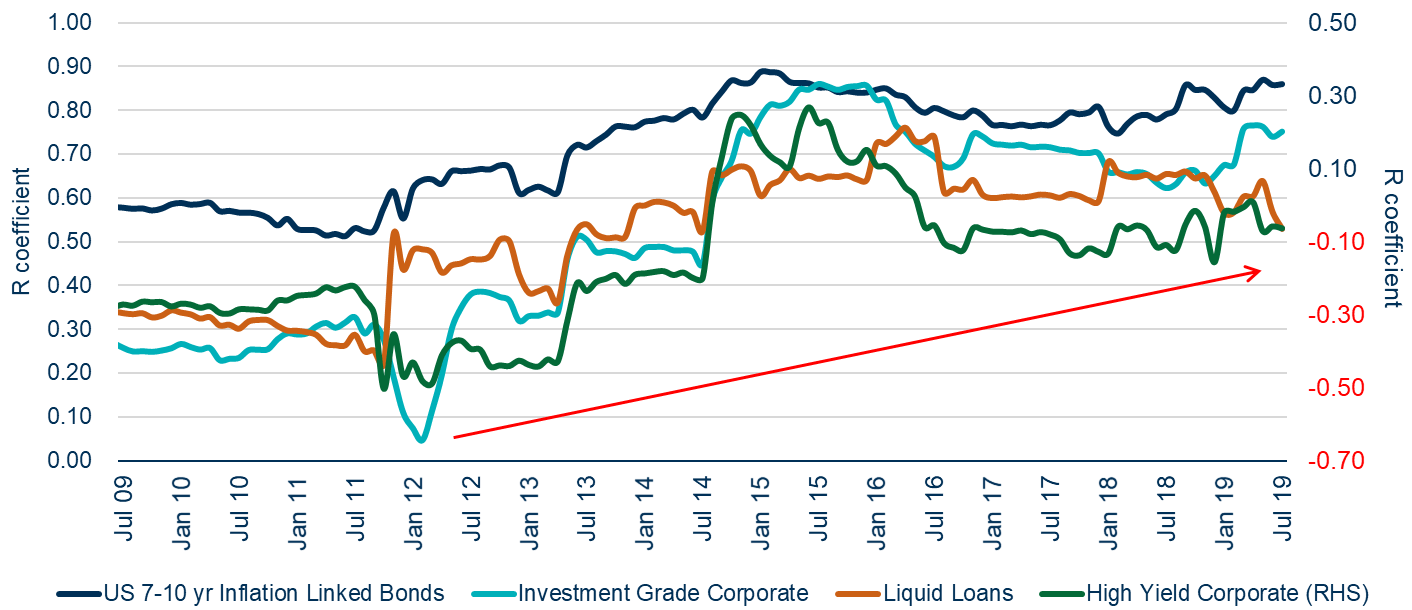

Harry Markowitz, the Nobel Prize winning economist and godfather of modern portfolio theory, famously remarked that diversification is “the only free lunch in investing” – and although multi-asset credit benefits from decorrelation across sub-asset classes, the rise in correlations2 have eroded the impact of diversification in recent years (see figure 2). For example, during the 2013 taper tantrum, risk assets and bonds declined together, reflecting a higher correlation (we will return to the impact of the taper tantrum later in the piece).

Figure 2. Don’t depend on diversification

Fixed income asset class correlation (36m rolling v US government bond)

Source: Federated Hermes, Bloomberg and Bank of America Merrill Lynch as at 31 July 2019. Note: the R coefficient is a numerical output used as a correlation measure tool between two variables.

Of course, there is value in adding diversifying sources of return by investing across different sub-asset classes but, given rising correlations, diversification alone should not be considered an adequate source of downside protection.

Dynamism is vital

The defence approach of rates and duration alone is unlikely to offer investors the protection they will need in the event of a market shock. To successfully manage downside risk, we believe dynamism is vital. We understand that a long-only exposure to bonds cannot continue to deliver the strong returns of recent years. Dynamic and flexible allocation allows us to respond to market changes with greater flexibility and security – that is, adjusting our portfolios to seek optimal sources of value throughout the cycle (see figure 3).

Figure 3. Dynamic and flexible allocation through the cycle

For illustrative purposes only. To be measured over the market cycle.

Another way in which we aim to preserve capital is through our ability to access a broad spectrum of liquid credit. This allows us to leverage our credit view across all debt instruments, gives us the ability to diversify our sources of alpha generation, and respond to changes in the market. We exploit relative value through high-conviction name- and security-selection. We also believe in active management predicated upon bottom-up, fundamental stock picking within a top-down framework. The discipline of assessing and pricing credit, ESG and liquidity risks is deeply ingrained in our investment process. ESG integration is a valuable tool for both downside protection and alpha generation through engagement on key issues that can impact the enterprise value and cash flows.

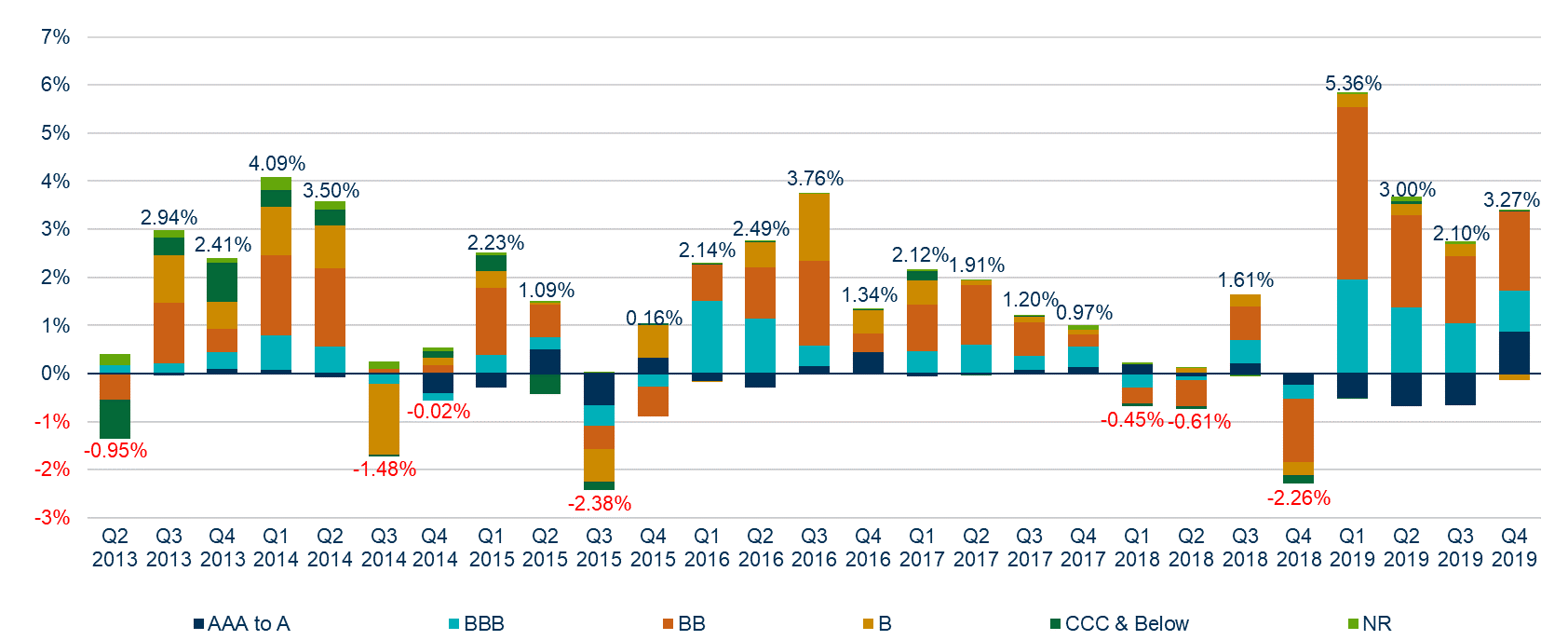

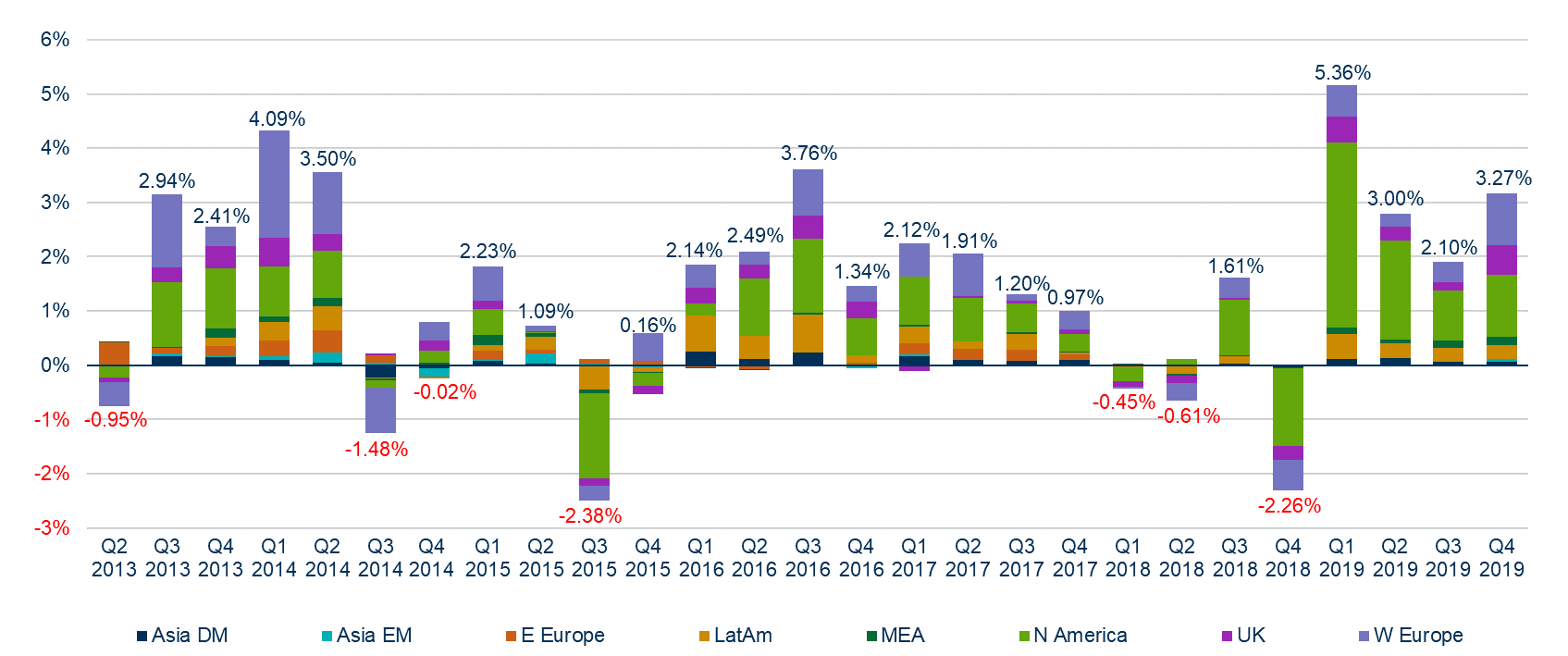

For example, one of our flexible strategies, Multi-Strategy Credit, aims to deliver positive performance based on superior security selection, sector and geographical allocation (see Figure 4), and by searching for the most attractive debt instruments – bonds, CDS or floating-rate notes – across the capital structures of issuers worldwide that offer the best pay-off profile. In doing so, we strive to provide investors with exposure to our best long-only credit investments, combined with defensive trades – a range of bearish strategies that seek to defend against market volatility and protect our ability to take risk when the opportunities are the greatest.

Figure 4. Multi-Strategy Credit: relative strategy performance since inception

4a. Performance analysis by ratings

Past performance is not a reliable indicator of future returns. Inception date: 31 May 2013. Performance as at 31 December 2019 in USD, gross of fees. Source: Federated Hermes Credit Team. The figure at the top of the columns is the sum of the positive and negative contributions.

Figure 4b. Performance analysis by geography

Broadening the toolbox

We aim to protect capital and enhance convexity by using an expanded set of tools: these include single-name CDSs, index CDSs and options on the index.

Indeed, within our credit team, we express a myriad of different views, and our views of the market will inform whether we use just one or a combination of these products to both preserve capital during broad, adverse market moves and exploit opportunities when they arise (see figure 5).

Figure 5. Managing downside risk: our investment decision-making process

Single-name CDS | Index CDS | Option on index | |

|---|---|---|---|

Investment view | Bottom-up | Top-down | Top-down |

Geographical view | N/A | Yes | Yes |

Ratings view | N/A | Yes | Yes |

Express an idiosyncratic view | Yes | N/A | N/A |

Liquidity | Moderate to very liquid | Highly liquid | Highly liquid |

PnL profile | Linear | Linear | Convexity |

A single-name CDS allows us to express a bottom-up view. Given its linear profit and loss (PnL) profile, should a small market correct occur, it will take effect immediately, providing a positive protection impact. However, its liquidity will vary from moderate to very liquid depending on the single-name in question.

Conversely, an index CDS and an option on an index have the same underlying. They express a top-down view on a geographical or ratings basis and are both extremely liquid. The main difference between these two products is their PnL profile: options add convexity, while index CDSs have the same linear profile as single-name CDSs.

Effective risk management is also an integral part of the investment process and so, using a centralised hub to manage portfolio risk is essential. Every day, we review our portfolio hedges using a proprietary dynamic duration-management tool that calculates the suggested hedge by currency and part of the curve based on current positioning, market environment, shape of the interest rates curve and correlations. We subsequently review the results and adjust the hedge as appropriate.

Indeed, adopting such a flexible approach enables us to mitigate risk more effectively than solely relying on rates and diversification.

Preparing for tomorrow

Dampening the downside: the 2013 taper tantrum

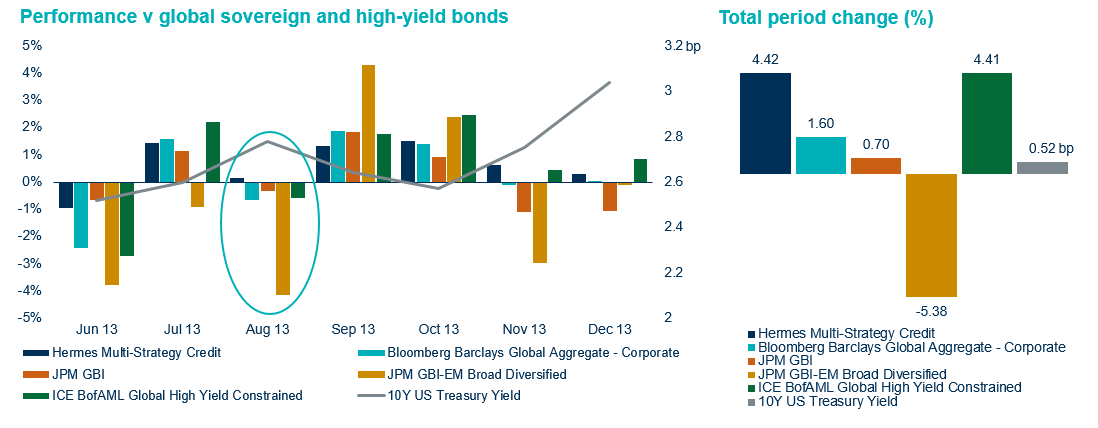

In Q2 2013, the US Federal Reserve indicated for the first time that it would reduce quantitative easing after almost five years of running the bond-buying programme. The market’s acute sensitivity to changes in US interest rates became clear: fear of a rate hike had already caused overcrowding in short-duration bonds, and this strong demand allowed issuers to introduce looser covenants and shorter non-call periods. Unwilling to accept the consequent risks (high valuations, weaker investor protections and diminished upside), we invested in credit default swaps of companies instead to gain a similar short-duration exposure. By leaning on some of the defensive trades in our Multi-Strategy Credit portfolio, we were also to protect against rising interest rate volatility, thereby preserving capital throughout the taper tantrum.

Figure 6. Preserving capital throughout the 2013 taper tantrum

Fighting risk with risk: a simulation study

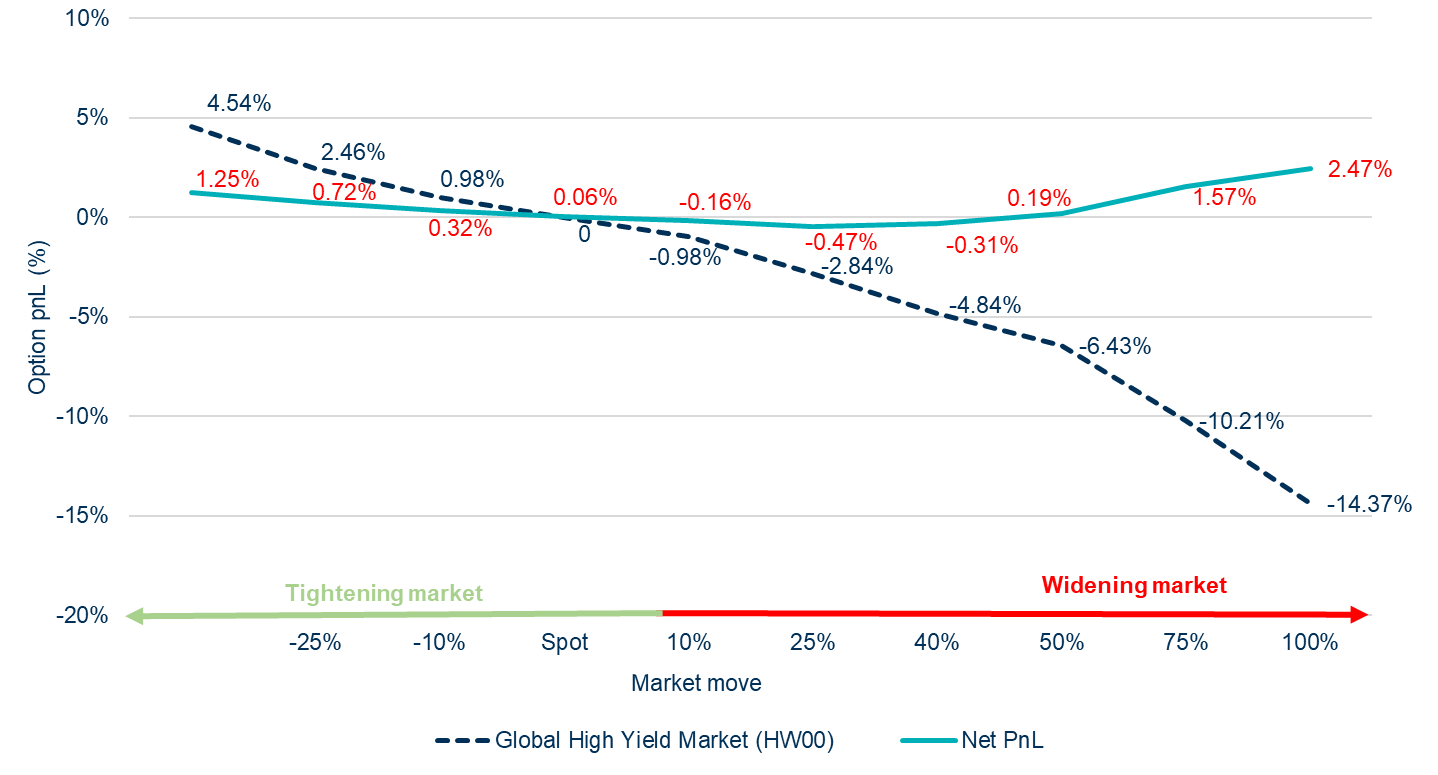

The long-running bond bull market can’t last forever – and so investors must use defensive strategies that have the potential to protect them in the event of a future shock. Should credit spreads widen, naturally investors will want to protect themselves from any extreme scenarios. By simulating the performance of the global high yield market (which is long-only by definition) compared to a global high-yield portfolio that uses options and index shorts as a hedge, it is evident that the latter will outperform the benchmark if spreads widen in the wake of a market correction thanks to the convexity provided by options (see figure 7). Such a simulation demonstrates the benefit of embedding options- and index-based strategies into our portfolios.

Figure 7. Scenario analysis: the appeal of downside protection

Source: Federated Hermes as at January 2020. For illustrative purposes only.

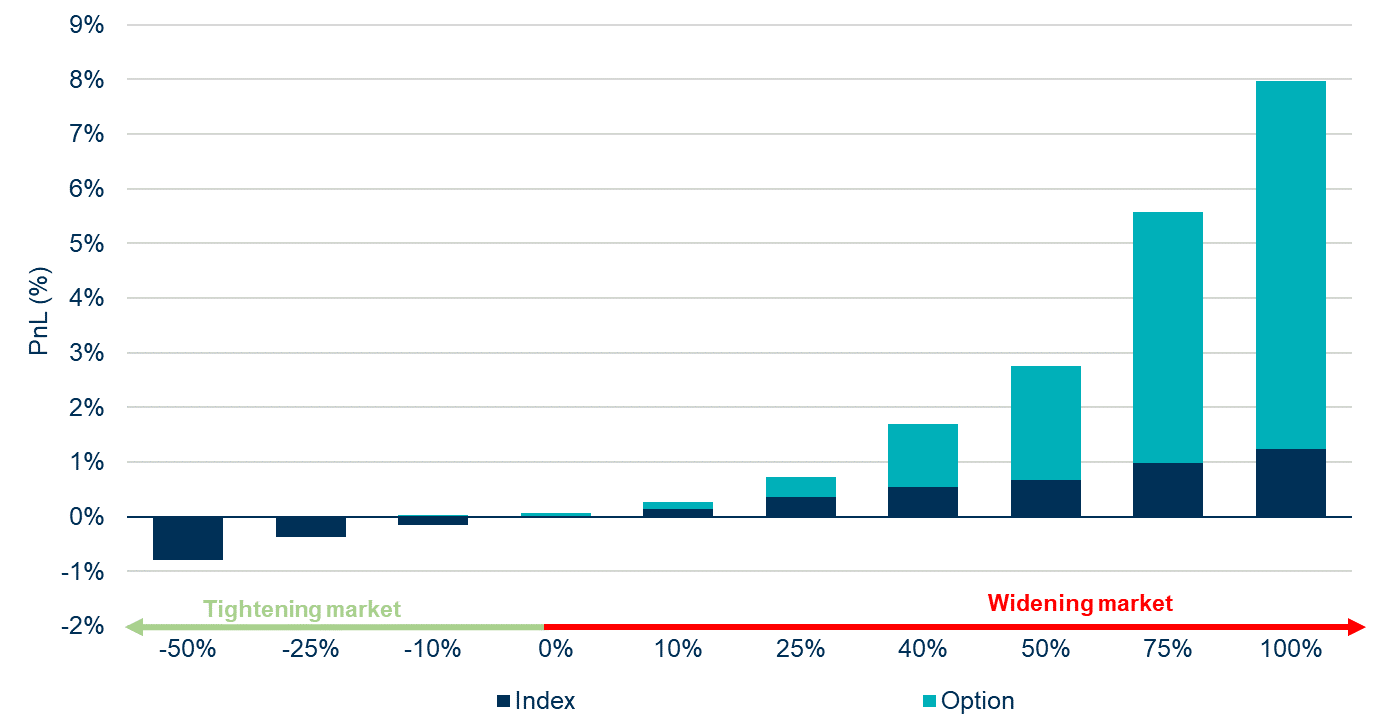

As already mentioned, we used index and options-based strategies to manage downside protection. By simulating a number of market-move scenarios, the impact of each strategy on the PnL is evident (see figure 8). For smaller market moves, index-based strategies take effect immediately. Conversely, the benefit of options only materialise when the market experiences wider moves – that is, the positive contribution of options to performance grows as the market underperformance deepens. Should a major correction occur, it is therefore possible to preserve capital by using out-of-the-money payers (puts). However, should the market tighten, the downside of employing an options-based strategy is limited to the premium paid. This example serves to demonstrate the power of combining both index- and options-based strategies during a market downturn.

Figure 8. How downside protection tools are expected to contribute to PnL in possible market scenarios

Ready to act: applying multiple lines of defence

As we have discussed already, the preceding decades have stacked up well for bond markets. But from here, investors must work harder – and to do so, multiple lines of defence – not just rates and diversification – will be needed to navigate any changing market conditions. Employing such strategies can not only help to reduce downside risk, but they may also enhance upside growth too.

Net rolling year performance (%) | |||||

|---|---|---|---|---|---|

31/12/18 to 31/12/19 | 31/12/17 to 31/12/18 | 31/12/16 to 31/12/17 | 31/12/15 to 31/12/16 | 31/12/14 to 31/12/15 | |

Multi-Strategy Credit | 13.68 | -2.37 | 5.64 | 9.36 | 0.39 |

Share:

Risk profile

- The value of investments and income from them may go down as well as up, and you may not get back the original amount invested.

- Targets cannot be guaranteed.

- It should be noted that any investments overseas may be affected by currency exchange rates.

- This information does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.

- Where the strategy invests in debt instruments (such as bonds) there is a risk that the entity who issues the contract will not be able to repay the debt or to pay the interest on the debt. If this happens then the value of the strategy may vary sharply and may result in loss. The strategy makes extensive use of Financial Derivative Instruments (FDIs), the value of which depends on the performance of an underlying asset. Small changes in the price of that asset may cause larger changes in the value of the FDIs, increasing either potential gain or loss.

1 Global bond bull run has reached historic levels,” published by The Financial Times in September 2019.

2 A rise in correlations limit the ability of fixed-income instruments to preserve capital in periods of volatility.