- Lack of clear fiscal rules for UK government mini-budget and absence of Office for Budget Responsibility oversight sparked panic in markets.

- In response, the central bank launched a £65bn emergency bond-buying programme following sharp spikes in UK gilt yields and collapse in value of sterling.

Bond market turmoil eased this week after the Bank of England (BoE) launched a £65bn emergency bond-buying programme on Wednesday to stabilise financial markets following UK Chancellor Kwasi Kwarteng’s mini-budget which announced sweeping tax cuts. The Chancellor published the mini-budget in the absence of oversight from the UK’s Office for Budget Responsibility, leading to a spike in UK gilt yields and a collapse in the value of sterling.

The 30-year gilt yield stood at 3.95% at 16:30 on 29 September, after hitting a two-decade high of more than 5% on Wednesday. Yields on 10-year UK government debt stood at 4.13% – after hitting 4.50% earlier in the week – while the pound was trading at 1.10 to the dollar on Thursday afternoon after falling to near parity1.

While the selloff in long-dated gilts and particularly inflation-linked gilts [prior to the BoE’s intervention] was extreme, the action from the central bank does beg the question: ‘What was happening behind the scenes that warranted this move?’” says Orla Garvey, Senior Fixed Income Portfolio Manager, Federated Hermes Limited.

The central bank’s intervention should reduce the tail risk of endless stop outs causing real yields to continue spiralling higher, she explains. “But it will cause confusion around tightening rates, starting quantitative tightening while still doing quantitative easing – and also doesn’t change the fact that there’s a huge amount of issuance in the years to come and the BoE won’t be here to buy it.”

“The concern would be that the market sees this as something to be tested and I don’t believe the bank will want to set this precedent. This continues to leave long-dated gilts vulnerable,” she adds.

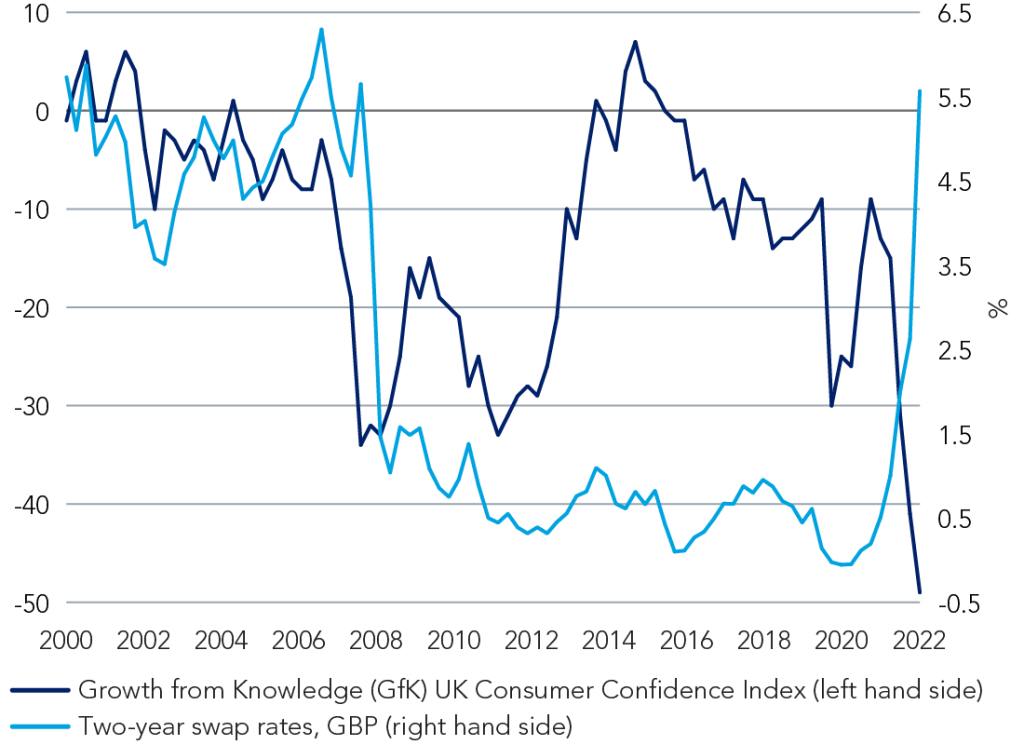

Two-year swap rates have continued to reprice to such an extent that they have almost entirely unwound the post 2008-09 global financial crisis moves, Garvey points out (See Figure 1).

Figure 1: UK consumer confidence vs. two-year swap rates

A weakening outlook

The BoE raised rates by 50bps on September 22 to 2.25%2. and another rise is expected at its meeting in November. The US Federal Reserve increased its policy rate by 75bps for the third consecutive time last week3 and other central banks have adopted similarly aggressive policy tightening as they seek to bring inflation under control.

“Gas prices also soared this week as the supply outlook worsened, exacerbated further by the damage to Nord Stream pipelines and the potential threat from Russia to curtail supply through Ukraine. Shipping rates are the beneficiary as they near record levels,” says Lewis Grant, Senior Portfolio Manager – Global Equities, Federated Hermes Limited.

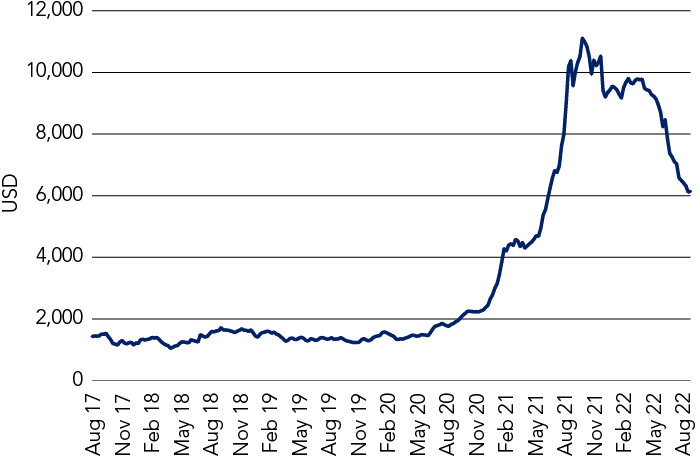

The Baltic Dry index, a benchmark for the cost of bulk shipping, is viewed as a useful indicator of global economic activity (see Figure 2).

After rising sharply following Russia’s invasion of Ukraine it has been falling fairly steadily since late May, indicating global shipping delays are easing as trade declines.

Figure 2: Baltic Dry Index (2012-2022)

European stocks and government bond prices ended lower on Thursday. The pan-European Stoxx Europe 600 closed down 1.81% while London’s FTSE 100 was down 1.77%. The US blue-chip S&P 500 ended Wednesday up almost 2% following a six-session losing streak4.

“Equity investors are being buffeted by waves of geopolitical risks, with little sign of respite. The impending earnings season will provide a stock-specific view on these geopolitical events and has the potential to be brutal: expectations have held up surprisingly well despite the macro stresses and with such negative investor sentiment there will be no quarter given for companies who fail to deliver. A well-diversified portfolio is key to smooth the whipsaw of these markets,” Grant adds.

1 Bloomberg as at 29 September

2 Bank of England lifts interest rates by 0.5 percentage points | Financial Times

3 Jay Powell refuses to rule out US recession after third 0.75 percentage point rate rise | Financial Times

4 Bloomberg as at 29 September