Q: Will the government also have to bail out banks again? How stable will the financial sector be if more and more loans start to default?

A: Unlike in the financial crisis, banks are currently playing a stabilising role. They have significantly expanded their lending to enterprises – partly thanks to government loan guarantees. But the same warning applies here – the longer the crisis lasts, the greater the risks to bank balance sheets.

–Jens Weidmann, President of the Deutsche Bundesbank, quoted in Frankfurter Allgemeine Sonntagszeitung on 21 June1

Waste not, want not

Weidmann is right: this time is not different. And as in other economic dislocations, clichés are guiding the collective thinking on disaster management.

‘Never let a good crisis go to waste’ has been the chief rerun of the pandemic, reaching a large audience as lockdowns worldwide have upended social, economic and financial certainties. In response, banks across the globe are reverting to their traditional, if long-neglected, role in society.

Most have realised that their franchise value hinges on supporting personal and business clients through this challenge: it’s about forbearance, not foreclosure.

After years of bad press and regulatory attention, banks could emerge as the good guys and even discover a new purpose.

We will see. In the interim, however, they have dramatically revised their capital-management plans to bolster balance sheet buffers. To some extent, bank shareholders and management teams are bearing the brunt of this crisis as financial institutions shoulder these social duties.

And once the global economy reopens more fully, there is a risk of a persistent shortfall in demand, weak earnings and a souring credit cycle – which will erode banks’ capital.

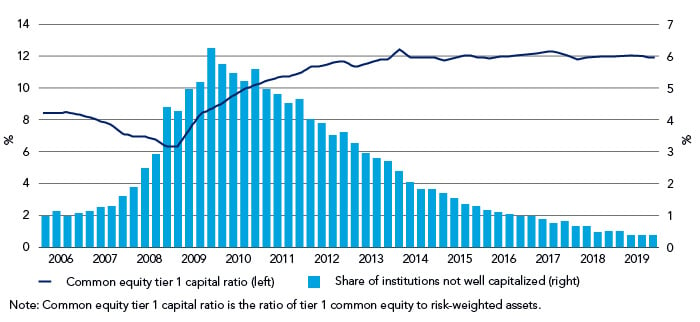

The institutions are already taking precautions. All of the US ‘money center’ banks, for example, have suspended major share buyback plans and the capitalisation of the system seems sound. In advance of the Comprehensive Capital Analysis and Review stress test for June 2020, the Federal Reserve stated: “The aggregate bank common equity tier 1 capital ratio ended 2019 at a high level, close to 12%. As of year-end 2019, less than one-half of 1% of institutions were not well capitalized”2.

Figure 1. Buffers ready: US institutions are now more strongly capitalised

Source: Federal Reserve at June 2020.

In Europe, banks have freed up an extra €30bn of balance-sheet firepower following 2019 dividend freezes on top of the €130bn released under capital regulatory relief measures3. Andrea Enria, Chair of the Supervisory Board of the European Central Bank, said recently: “Our estimates are that those decisions, together with the decisions by national authorities to release some of the macroprudential buffers, made available around €160bn of extra CET1 capital in order to absorb losses and extend credit before prudential minimum requirements are breached”.

UK banks could have access to between 1.6%-2% of more capital due to the combination of relaxed regulation and dividend suspensions.

Stress less? Now’s not the time

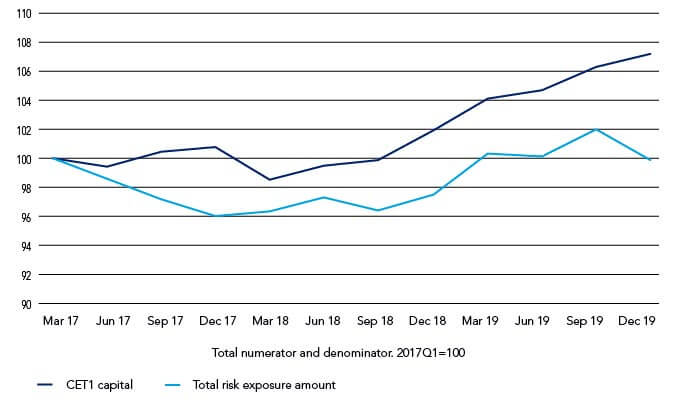

What should be the worst-case scenario that we pencil in? On 25 May, the European Banking Authority released a sensitivity analysis of credit losses linked to the coronavirus, using the 2018 stress test as a starting point (updated for 4Q19 loan portfolios). This indicated the potential impact on common equity tier 1 (CET1) and serves as a useful illustration of how bad things could get.

Figure 2. Up to the test? European banks’ capital buffers

Source: European Banking Authority at June 2020.

In aggregate, this showed defaults resulting in losses ranging from between 230-380bps of CET1, but importantly this analysis did not consider the potentially beneficial impact of loan moratoria or state guarantees4. This is key, as the impact of both on the cost of risk in 2020 will be significant. Still, the EBA exercise indicated losses comparing to average capital headroom of about 500bps, shows the resilience of the banking sector on average.

By carefully managing capital and tuning in to the coronavirus zeitgeist, banks could well rebuild their reputations as socially important entities.

This time could be different, after all.

1 “The trough is likely to be behind us now”. An interview with Jens Weidmann in the Frankfurter Allgemeine Sonntagszeitung, published on the Deutsche Bundesbank website.

2 “Supervisions and Regulation Report: May 2020”, published by the Board of Governors of the Federal Reserve System.

3 “Introductory statement”, a speech by Andrea Enria, Chair of the Supervisory Board of the ECB, at the virtual meeting of the European CFO Network organised by UniCredit Group, on 12 June 2020.

4 It is important to note that the EBA analysis stressed the probability of default, while loss given defaults and exposures at default were held constant.