What is LIBOR?

LIBOR is a measure of the average rate at which banks are able to borrow wholesale unsecured funds. It is administered by the ICE Benchmark Administration and is calculated using submissions from a panel of global banks. Banks submit an estimate of what they would pay other banks to borrow for a specific period of time if they borrowed money on the day the rate is being set. Depending on how many banks submit estimates, roughly the top and bottom quartile of submissions are discarded, before an average is set.

Published in five currencies (US dollar, sterling, euro, Swiss franc and Japanese yen) and a range of tenors (from overnight up to 12 months), LIBOR is used as a reference rate in financial contracts that include derivatives, bonds and loans. Overall, it underpins about $300trn-worth of deals.

Why is it being replaced?

The rates that are submitted are estimates and not based on actual transactions, which has resulted in some high-profile cases of LIBOR manipulation. Coupled with a decline in interbank lending, this prompted Andrew Bailey, then-CEO of the Financial Conduct Authority (FCA) and current governor of the Bank of England, to call for an end to the use of LIBOR and a “transition to alternative reference rates that are based firmly on transactions.”1

At that time, Bailey said that the FCA would not compel banks to make LIBOR submissions beyond 2021. Similarly, the Bank of England’s Financial Policy Committee stated in its Financial Stability Report that “the continued reliance of global financial markets on LIBOR poses a risk to financial stability that can only be reduced through a transition to alternative risk-free rates (RFRs) by end 2021.”2

As such, the FCA secured panel-bank support to continue submitting to LIBOR, but only until 2021. Beyond this date, the future of LIBOR is not guaranteed.

What is it being replaced with?

The replacements for LIBOR and IBORs have not all been agreed. Some have been confirmed: for example, the Sterling Overnight Index Average (SONIA) will replace sterling LIBOR, while the Secured Overnight Financing Rate (SOFR) will replace US dollar LIBOR. As table 1 illustrates, these risk-free rates (RFRs) are not direct replacements, with differences in calculation methodologies as well as collateralisation levels. There remains a significant degree of uncertainty: although the alternative rates have been selected, it is not yet clear how they will be adopted in certain markets.

Figure 1. Alternatives to LIBOR

Jurisdiction | Working group | Alternative reference rate name | Administrator | Collateralisations | Description |

|---|---|---|---|---|---|

US | Alternative Reference Rates Committee

| Secured Overnight Financing Rate (SOFR) | Federal Reserve Bank of New York | Secured | Secured rate that covers multiple overnight repo market segments |

UK | Working Group on Sterling Risk-Free Reference Rates | Sterling Overnight Index Average (SONIA) | Bank of England | Unsecured | Unsecured rate that covers overnight wholesale deposit transactions |

Switzerland | The National Working Group on CHF Reference Rates | Swiss Average Rate Overnight (SARON) | SIX Exchange | Secured | Secured rate that reflects interest paid on interbank overnight repo rate |

Japan | Study Group on Risk-Free Reference Rates | Tokyo Overnight Average Rate (TONAR) | Bank of Japan | Unsecured | Unsecured rate that captures overnight call rate market |

Euro area | Working Group on Risk-Free Reference Rates for the Euro Area | Euro short-term rate (€STR) | European Central Bank | Unsecured | Unsecured rate that captures overnight wholesale deposit transactions |

Source: Financial Conduct Authority, as at September 2019.

In order to remain fair to all parties, these replacement rates will need to be adjusted. For example, there will need to be agreed methodologies to compound and calculate the daily rate to create one that matches the maturity of the agreed term. Because some of these RFRs are backwards looking, a timing challenge arises when calculating coupons. As a result, lag mechanisms will have to be put in place.

IBOR rates reflect the terms at which banks would lend to each other at the unsecured level. Conversely, some of the new RFRs being considered reflect secured lending terms. This results in a lower credit risk and most likely a lower quoted rate.

How are we managing the transition?

At the international business of Federated Hermes, we understand that the transition to RFRs will have different implications for our clients. We are committed to working with them to understand the impact across asset classes and portfolios and have set up a dedicated programme and project resource to manage the transition.

We have an assigned working group and project manager who is responsible for ensuring we are equipped and ready to move away from LIBOR and other IBORs at the end of 2021. They are responsible for leading project governance and frequently updating senior members of the company (including our CIO, the project sponsor) about our exposure, the development of suitable alternative reference rates and next steps for our transition.

Through our impact assessment, we have found that the key areas likely to be affected are:

- Operations: we are working to ensure that our systems and processes can handle the new alternative reference rates and perform accrued interest calculations.

- Performance and benchmarking: we are making sure that our benchmarks and performance analytics are re-baselined (where applicable) to the new RFRs.

- Legal contracts: a range of procurement, counterparty and client contracts reference LIBOR and other IBORs. As a result, we are working to assess the materiality of the impact of the LIBOR transition and will revise our contracts where appropriate.

In addition, we have installed a client communications committee and will be providing regular updates on how we are managing the transition. If you have any questions on our move away from LIBOR, please contact your sales representative.

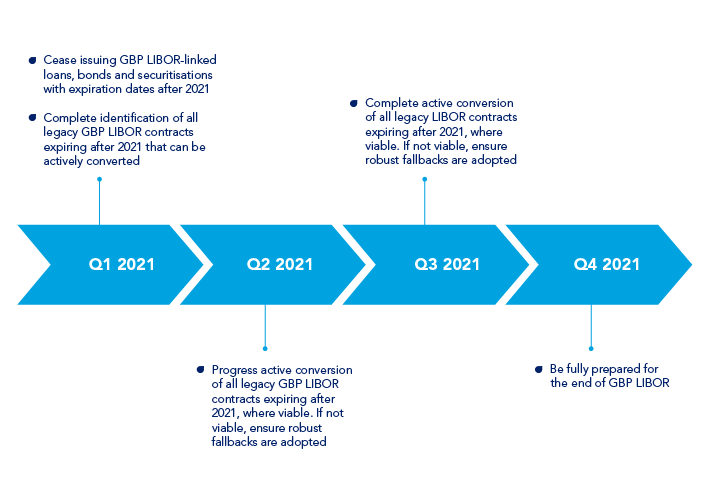

What are the priorities and milestones for the GBP LIBOR transition in 2021?

The international business of Federated Hermes has identified all GBP LIBOR exposure through an impact assessment conducted in 2020. This has been independently verified by a third-party auditor.

Figure 2. Expected timeline for GBP LIBOR transition

Source: Federated Hermes, as at March 2021.

What is the ISDA Protocol?

On 23 October 2020, the International Swaps and Derivatives Association, Org (ISDA) launched the IBOR Fallbacks Supplement to the 2006 ISDA Definitions (the “Supplement”), and the ISDA 2020 IBOR Fallbacks Protocol (the “Protocol”). 3Both have an effective date of 25 January 2021. From this date, all new contracts that incorporate the 2006 ISDA Definitions ─ and reference one of the covered IBORs set out in the Supplement ─ will contain the new fallbacks.

This means that on final cessation of the applicable IBOR, the relevant replacement rate will apply. The new calculation methodology and a standardised spread adjustment will be used, unless the counterparties involved have agreed on an adjustment spread bilaterally before the cessation occurs.

While adherence is voluntary, as with all ISDA protocols, we have signed up.

What happens to USD LIBOR?

In November 2020, ICE Benchmark Administration (IBA) announced that it would be consulting on its intention to cease USD LIBOR, a move the Financial Conduct Authority (FCA) welcomed and supported.4 Subject to confirmation following consultation, the IBA said it intended to cease publication of one week and two month USD LIBOR after 2021. It also said it would cease publication of overnight, one, three, six, and 12-month USD LIBOR after 30 June 2023.

Although we continue to monitor all USD LIBOR exposures, the international arm of Federated Hermes has no exposure to one- or two-month USD LIBOR.

3 See: ISDA

4 See: Financial Conduct Authority