- The BoE emergency gilt-buying programme is set to end this week although central bank reportedly open to extend programme in the event of further market volatility.

- Many investors anticipate a sharp increase in interest rates next month in response to the government’s fiscal plans.

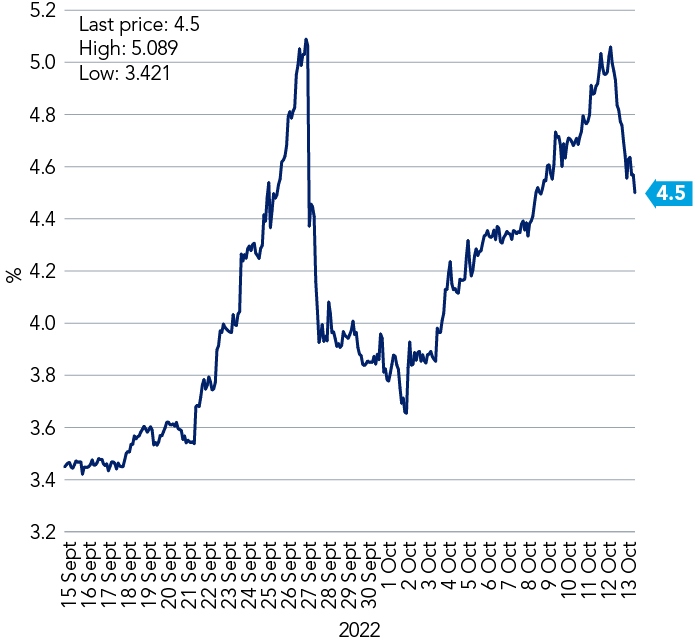

UK government bond yields endured further spikes this week after the Bank of England (BoE) stuck by its self-imposed deadline to stop its emergency £65m gilt-buying programme on Friday. The scheme was introduced to calm markets unnerved by the fiscal plans of new UK Prime Minister Liz Truss. The yield on the 30-year UK gilt had leapt to as high as 5.1% this week, before steadying to 4.5% at 16:30 GMT on Thursday 13 October amid the speculation the government may row back on some of its fiscal plans (See Figure 1). The yield on the 10-year gilt – which had risen to 4.6% this week – stood at 4%¹.

“Investors are anxious about the conflicting plans of the BoE and the government; the former trying to put the brake on growth to tame inflation while the latter is putting its foot on the growth accelerator, increasing inflationary pressures,” says James Rutherford, Head of European Equities, Federated Hermes Limited.

While the BoE stated it would end its scheme this week, officials reportedly briefed lenders in private that the BoE was prepared to extend the programme in the event of further market volatility². “It hasn’t helped that the BoE has provided confusing and flip-flopping messaging on its intentions, which might reflect internal debates around the dilemmas they are facing, involving inflation, growth and financial stability,” says Silvia Dall’Angelo, Senior Economist, Federated Hermes Limited.

“The BoE is aware that the current conflicting set of policies – tightening monetary policy with one hand and buying long-dates gilts with the other to stabilise financial markets – is unsustainable and is trying to move the focus back on high inflation, as the opportunity window to tackle it is about to close with growing recessionary signals. Whether developments in financial markets will allow them to do so is another story,” Dall’Angelo says.

Figure 1: 30-year UK gilt yields on a bumpy ride

Shifting focus

If as expected the BoE ends its emergency bond-buying programme on October 14, the market focus should firmly shift from the BoE to the government, says Orla Garvey, Senior Fixed Income Portfolio Manager, Federated Hermes Limited. “Gilts have been performing better in recent sessions and we think this is on the back of fiscal reversal or perhaps an entirely new government entering the distribution in the short-to-medium term. Sterling and short sterling in particular is trading well on this,” she says.

Investors have highlighted underlying concerns about the health of UK public finances, with the government under increasing pressure to show how it will get shore up its fiscal position. On Wednesday in Parliament, Ms Truss stated the government would not reduce expenditure — prompting questions about how it plans to finance its intended £43bn in tax cuts.

Despite concerns about how much central banks can hike borrowing costs this year in the face of slowing growth (the UK economy shrunk 0.3% in August), many investors anticipate a big increase in interest rates in November in response to the government’s fiscal plans. The BoE raised rates by 50bps on September 22 to 2.25%.

European stocks ended higher on Thursday. The pan-European Stoxx Europe 600 closed up down 0.9%; while London’s FTSE 100 was up 0.4% amid expectations the UK government may change course on tax rises. The US blue-chip S&P 500 ended Wednesday down 0.3% at a two-year low³.

With higher interest rates and a higher risk of future earnings disappointments, investors should focus on low-multiple stocks with strong balance sheets, says Geir Lode, Head of Global Equities, Federated Hermes Limited. “Higher interest rates alone also makes low multiple value stocks more attractive. Investors should focus less on high multiple stock darlings with limited US dollar sales and earnings,” Lode says.

For further insights into fixed income please see the latest Q3 2022 360° report.

1 Bloomberg as at 13 October

3 Bloomberg as at 13 October