The scale of the pandemic and the response elicited has shone the light firmly on the ‘S’ of Environmental, Social & Governance (ESG) factors, but all three issues have come to the fore as the crisis has developed. Eoin Murray, Head of Investment, at the international business of Federated Hermes, takes a closer look at ESG performance and the importance of addressing these factors over the long-term.

Coronavirus has disrupted economies and financial markets in unprecedented ways, exposing the global economy’s lack of preparedness and resilience and radically reconfigured perceptions of sustainability.

Social factors once deemed to be non-financial or extra-financial concerns, have very clearly demonstrated that they are in fact financial matters indeed. We contend that their importance will only grow stronger through the global recovery and into the post-crisis world. The experience of what worked and what didn’t through the recent period must provide a framework for sustainable investment approaches going forwards.

Performance

Our proprietary research demonstrates that investment strategies which integrate ESG factors have historically outperformed those that do not. This observation, supported by academic evidence, holds across all asset classes. While we remain focused on sustainable value creation over long-term time horizons, YTD comparisons evidence the relative resilience of ‘social outperformers’ across equities, and of ESG factors more broadly in credit, through the recent market turmoil.

Equity

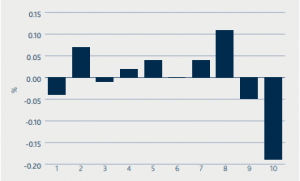

Research from our Global Equities team reveals that companies with poor or worsening social practices consistently underperformed their peers by 15bps each month since the beginning of 2009.

Figure 4. Companies with the lowest ranked social scores tend to underperform

Source: Hermes Investment Management as at 30 June 2018.

Credit

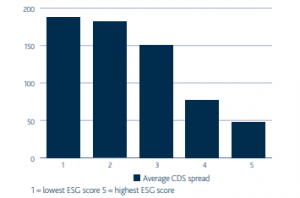

A study from Beyond Ratings and our Credit and Responsibily teams indicates that countries with the highest ESG scores (quintile five) have the lowest average CDS spreads, while those with the lowest ESG scores (quintile one) have the highest average CDS spreads. The difference in average spreads between these quintiles in terms of basis points is 140bps.

Figure 5. Average sovereign CDS spreads by ESG quintile, 2009-18

Source: Hermes and Beyond Ratings. Data as at August 2019

Resilience through a crisis: ESG outperformance

Source: S&P Global, MSCI, Federated Hermes

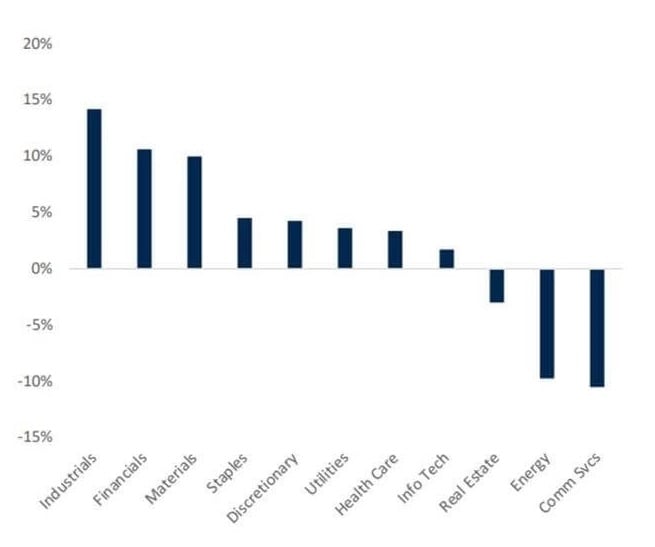

Importantly, this is not a sector specific phenomenon, with broad representation of ESG leaders outperforming in 8 out of 11 GICS sectors according to Sustainalytics:

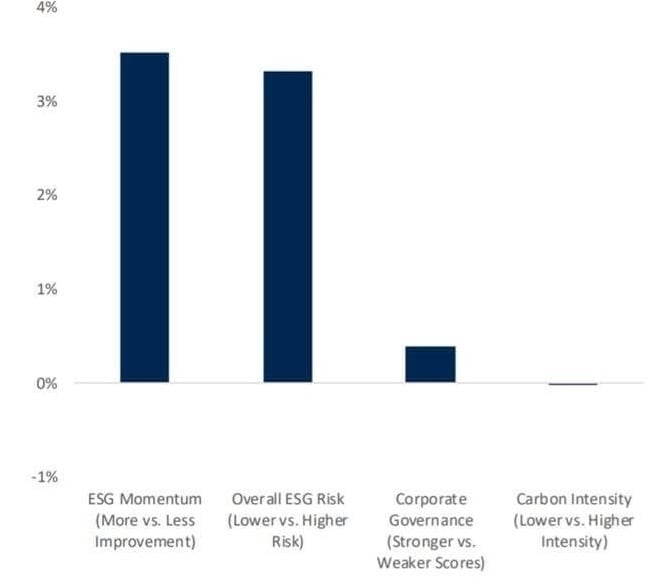

S&P 500 ESG Factor Perf Since Teh Feb 19th Market Peak Sector Neutral

S&P 500 Relative Returns Since Feb 19th Market Peak: Overall ESG Risk Scores (Lower vs. Higher Risk)

Source: RBC, S&P Global, Sustainaytics, Trucost, Federated Hermes

Constituents are equal weighted, baser on total returns; sector neutral analysis is capturing the top quintile vs. bottom quintile within each sector

The S factor?

The question remains as to why exactly these stocks have outperformed. Over the longer term, we can point to the creation of value for all stakeholders, including employees, customers, shareholders, bondholders, suppliers, the environment and wider society. Through a pandemic crisis, set to catalyse or accelerate potentially long-lasting implications for social and environmental issues, perhaps investors ascribe even greater weighting to the importance of these factors?

On the social side, major societal challenges – of healthcare resilience, the welfare of service and gig-economy workers, and the misery caused by social inequality – have gained new prominence in the international consciousness.

From an investment perspective, people have postulated that ESG factors are merely proxies for elements of quality and momentum. While healthy cash flows, a robust balance sheet and strong earnings would all feature alongside sound corporate leadership and strategy, this crisis has demonstrated the importance of social responsibility in the context of companies’ ability to survive – and thrive over the long-term.