Fast reading

- Spotlight: From disinflation to reflation to stagflation?

- Fundamentals: The outlook for credit in the context of a supply shock to the system

Typically, when we see elevated geopolitical risks, the flight to quality includes government bonds. As a result, front-end interest rates rally. This did not happen following the Israeli-US attacks on Iran.

So, what has happened… and what does it mean for credit markets?

First, the price of fossil fuels spiked… and then spiked again. Within hours of the attacks, inflation forecasts reversed entirely. The market pivoted from expectations of disinflation to fears of inflation as the price of oil rose more than 50% within days, continuing an upward trajectory that began before the onset of the latest conflict.

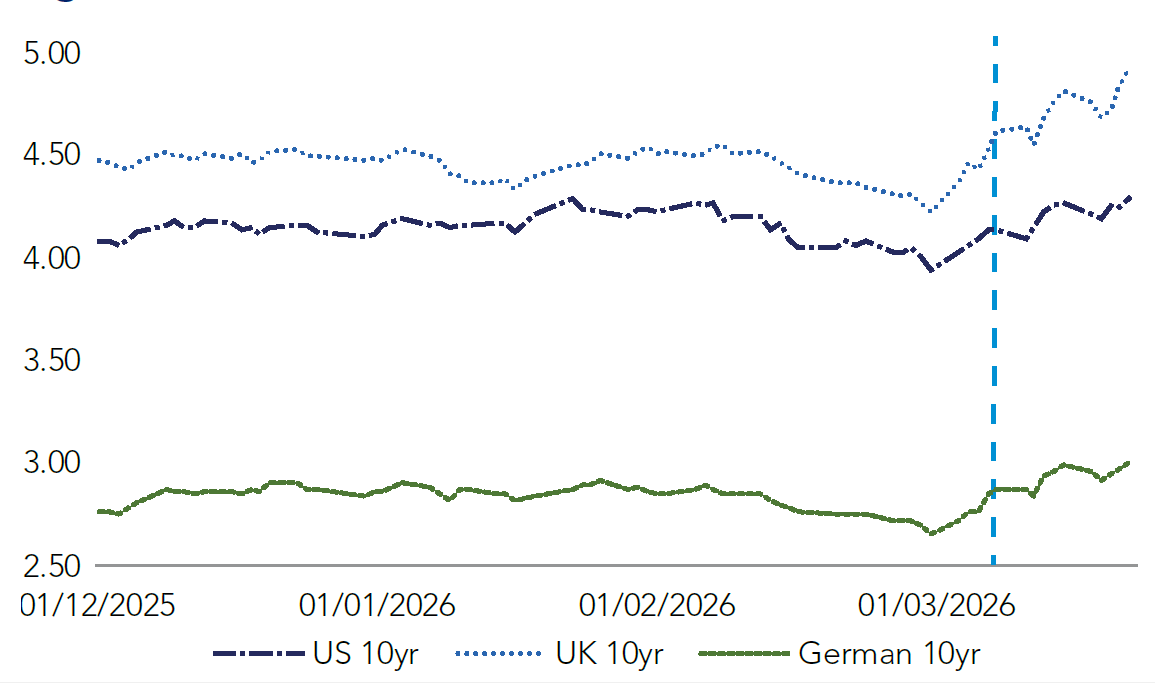

Figure 1: Dotted line demarcates the launch of the attacks on Iran

Source: Bloomberg, Federated Hermes, Ltd. March 19, 2026.

Second, the reversal in inflation expectations triggered a sell-off in rates, as the prospects of dovish central bank policy this year– predicated on ongoing disinflation– evaporated. The sharpest sell-off was in UK gilts, where a 90% market expectation of a spring rate cut by the Bank of England collapsed to zero1. Meanwhile, central bank activity during the week of 16 March pushed expectations even further in the same direction.

The sharpest sell-off was in UK gilts, where a 90% market expectation of a spring rate cut by the Bank of England collapsed to zero.

Markets are now expecting as many as three rate hikes from the Bank of England (BoE) and the European Central Bank (ECB). This is a remarkable turn of events in just a matter of weeks.

The sell-off in the front end of the curve has caused dramatic bear flattening, accelerating the twist in rates curves. In the space of just over a month, we have seen more than 85 basis points (bps) of flattening in the two-year/30-year gilt curve from peak to trough, and dramatic flattening in others as well (Figure 2).

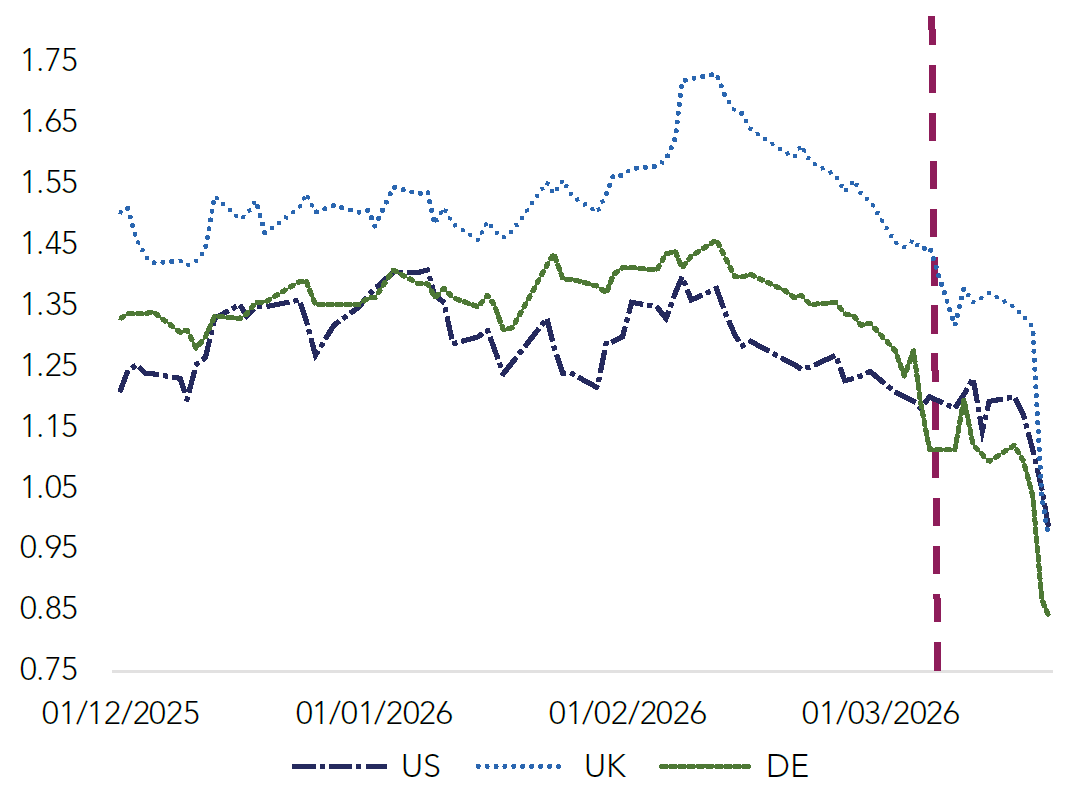

Figure 2: Rate curves do the twist

Source: Bloomberg, Federated Hermes, Ltd. March 19, 2026.

Concerns about inflation and, as a consequence, central bank rate activity, appear to have eclipsed worries about the effects of rising geopolitical risks on the back of the US military’s “little excursion” into Iran2. This speaks volumes about the market’s belief that the current conflict can be contained. Elevated oil prices in the near term appear likely.

The extent to which the price of oil can be contained remains an open question. What is clear is that rates markets have made a rapid U-turn from the dovish consensus-led rally this year (until 2 March). This suggests that markets now see central banks lifting rates to tame inflation, which, in turn, has caused the pronounced moves in credit markets.

FHL 360 H1 2026 report

1 World Interest Rate Probabilities (WIRP), Bloomberg.

2 Trump calls U.S. operations in Iran ‘a little excursion’. March 11, 2026.

BD017448