Scientists have forever battled against fear, uncertainty and doubt – or ‘FUD’ as the cryptocurrency crowd likes to phrase it – to advance the cause of greater knowledge.

FUD-fighting, however, can come at a terrible price for those at the vanguard of scientific progress like Austrian physicist, Ludwig Boltzmann, who in 1877 defined ‘entropy’ as an inescapable, statistically quantifiable fact inexorably leading the universe into a disordered state.1

Boltzmann was not the first scientist to propose entropy with his genre-bending formula coming almost 30 years after German physicist, Rudolf Clausius, coined the term and laid the basis for the field of thermodynamics.

However, the Austrian made the explicit and measurable link between the action of tiny particles and macroscopic thermodynamic behaviours.

In popular culture ‘entropy’, perhaps, is a synonym for chaos, but the term has a more precise technical meaning, which the Encyclopedia Britannica defines as: “… the measure of a system’s thermal energy per unit temperature that is unavailable for doing useful work. Because work is obtained from ordered molecular motion, the amount of entropy is also a measure of the molecular disorder, or randomness, of a system.”

If left undisturbed, the entropy, or ‘e’, of any isolated system always increases to the point of thermal equilibrium, leaving all particles at the same temperature with no prospects of useful work. Entropy offers deep insight into the nature of spontaneous changes witnessed in everyday phenomena, as well as a gloomy prognosis for the future of the universe.

But we exist in a lucky low entropic zone in the universe that enables highly ordered entities, such as ourselves, to live in a state that could be sustained for billions of years yet, if we look after it.

Unfortunately, as the mounting evidence of human-derived environmental degradation and climate change data suggests, we have not been great custodians of our low-entropy paradise.

Financial sector zeroes in on climate

As discussed in the July Fiorino, climate change, in particular, has added to the financial sector’s other well-publicised existential challenges such as super low interest rates, digitalisation, high fixed costs and weighty compliance obligations.

Like ‘e’ in pre-Boltzmann times, though, climate change (‘c’ anybody?) remained a broad concept, rather than an actionable quantity on the books of banks, insurers and other financial institutions.

Now, supervisors, investors and governments around the world are demanding financial institutions and corporates supply greater clarity and detail on climate change risks. Specifically, through a range of initiatives including the Taskforce on Climate-related Financial Disclosures (TCFD), authorities are working with institutions and investors to develop a more precise picture of the resilience of financial firms across a range of plausible climate change scenarios.

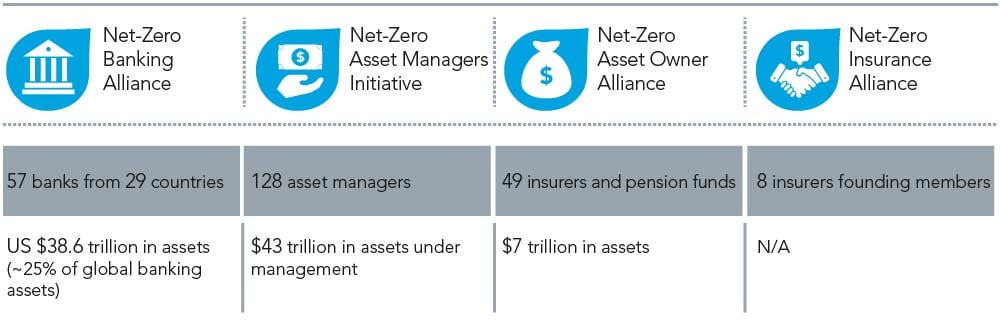

Galvanised into action, and well-aware of the stakes at play, many financial institutions have organised groups to develop a collective response to the climate change challenge.

Figure 1. Overview of net-zero financial institutions

Source: United Nations, 2021

For example, banks and insurers are learning to manage new dangers as climate change disrupts the economy, erodes corporate revenues and threatens traditional risk management tools, such as ratings assumptions or default probabilities.

Forward-thinking risk management and commercial strategy must apply climate criteria across lending and investment books to both limit losses and profit from emerging opportunities.

Without a doubt, those institutions slow to incorporate climate change risks face financial and reputational consequences that will erode their credit strength. Institutions financing coal-miners, for instance, could see less demand for their debt or equities securities, as investors judge long-term climate risks to outweigh any short-term profits. And given coal firms typically represent only a small proportion of lending books, this could be a case of ‘picking up pennies in front of a steamroller’ for those continuing the practice.

ECB stresses in, as test date set

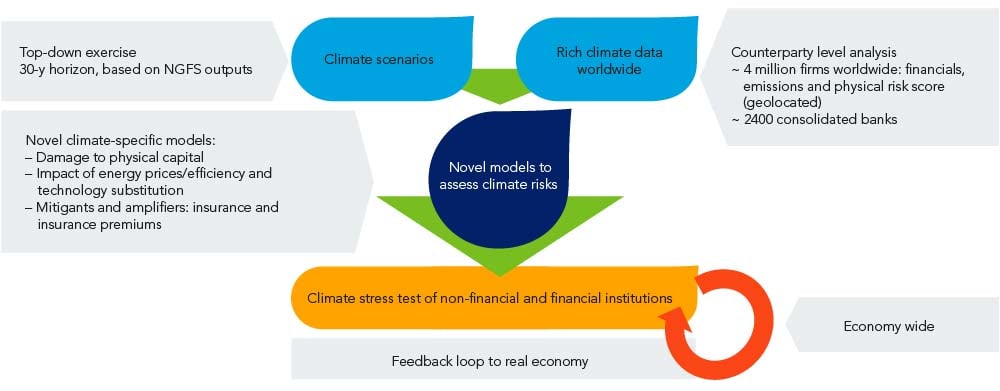

While institutions and investors will continue to develop their own nuanced understanding of climate risks, regulators are also adding their heft to the effort. Most recently, the European Central Bank (ECB) unveiled a Climate Stress Test (CST) to identify vulnerabilities and industry best-practices among the financial institution under its watch.

In addition to flagging challenges, the CST was designed to improve the quality and availability of climate data as well as providing regulators with deeper insight into how banks assess the emerging risks.

Figure 2. Main elements of the ECB economy-wide climate stress test

Source: European Central Bank (ECB), 2021

In guidelines for the 2022 CST – released on 18th October – the ECB began their push, with an emphasis on enhancing bank climate risk disclosure and peer comparisons. The CST results will not directly affect bank capital obligations (although, this will happen in the medium term); instead, the information will feed into the Supervisory Review and Evaluation Process (SREP) as a qualitative factor, potentially influencing bank Pillar 2 capital requirements.

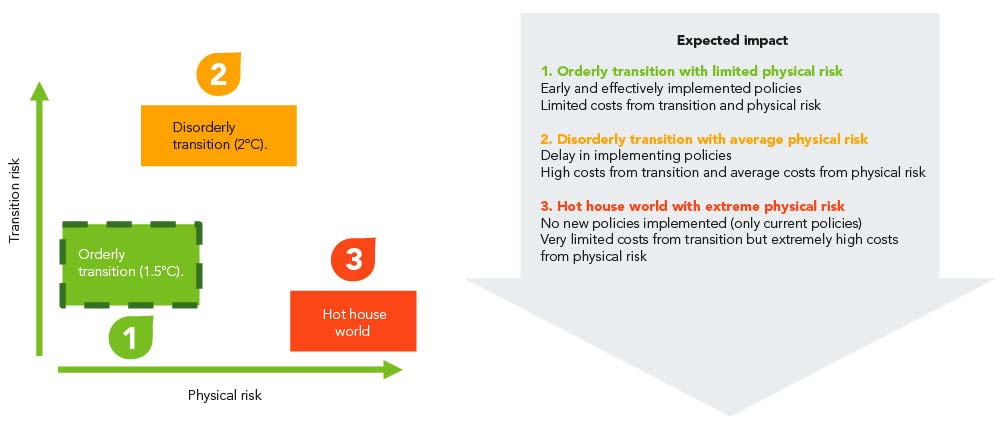

Figure 3. ECB’s three scenario for physical & transition-risk

Source: European Central Bank (ECB), 2021

Note: The scenarios are organised in the graph based on the combination of transition and physical risks.

Under the plan, the ECB will roll-out the climate risk stress-test to banks from March to July of next year in two main phases: data-collection mode, followed by a quality assurance exercise.

In practice, the CST has been structured as three modules, comprising:

- Module 1 – a questionnaire to assess how banks are building their climate stress test capabilities;

- Module 2 – a peer benchmark analysis across climate risk metrics including banks’ reliance on income from carbon-intensive industries and volume of greenhouse gas emissions they finance. The study should enhance the comparability of bank exposure and indirect emissions, via loan books. Currently, only a few banks in Europe provide this data (mostly French and Dutch lenders); and,

- Module 3 – bottom-up stress-test on transition and physical risks including scenarios examining the impact of extreme weather events over the next year, a sharp increase in the price of carbon emissions over the next three years, and transition scenarios over the next 30 years. Banks will provide starting points and their own projections under a common scenario and methodology prepared by the ECB. The scenarios will be based on those developed in the ECB 2021 economy-wide climate stress-test.

Weathering doubts

Overall, the CST will provide a comprehensive first-take on climate risks in the European banking sector with three core outcomes: a qualitative assessment of the institutions’ internal stress-testing capabilities; a comparable quantitative assessment of institutions’ reliance on greenhouse gas intensive industries (both in terms of revenues and volumes financed); and a bottom-up stress-test on transition and physical risks.

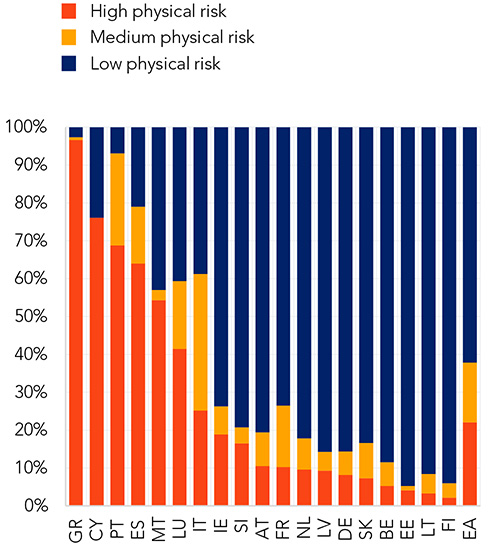

For investors, the bottom-up stress-test should provide the best view yet of climate change liabilities across issuers. Greater physical risks in southern Europe – for example, the increased frequency and severity of natural disasters, as per the graph below – could compound the divergence between core and peripheral countries, something already evidenced in recent ECB top-down testing. Caveat here: estimating climate risk scenario with any degree of precision needs be taken with a pinch of salt.

Figure 4. The share of bank loans exposed to physical risk

Source: European Central Bank (ECB), 2021

It would be a cruel irony if the ECB – renowned for saving the single currency during the Global Financial Crisis – drives the Eurozone further apart with a tool designed to shed light on the entropic climate effects of previously opaque financial components.

In a sad coda to a briliant career, Boltzmann – just 62 at the time – took his own life while on a family holiday in Duino, near Trieste, Italy, in 1906. He did not leave a note, but his insights on entropy live on.

We must fight the FUD.

Ludwig Boltzmann (1895)

1Boltzman’s formula for entropy, as carved on his gravestone, is S=KB log W