Inflation and supply chain disruptions, along with the moderating pace of the post-pandemic earnings recovery, have made us more cautious on corporate fundamentals as we enter Q3 reporting season. While we do not expect a material deterioration in credit profile on the back of these factors, the more challenging operating environment does require caution from credit investors.

In this summary, our Credit analysts offer their view on the impact of inflation and supply chain disruptions on the sectors they cover:

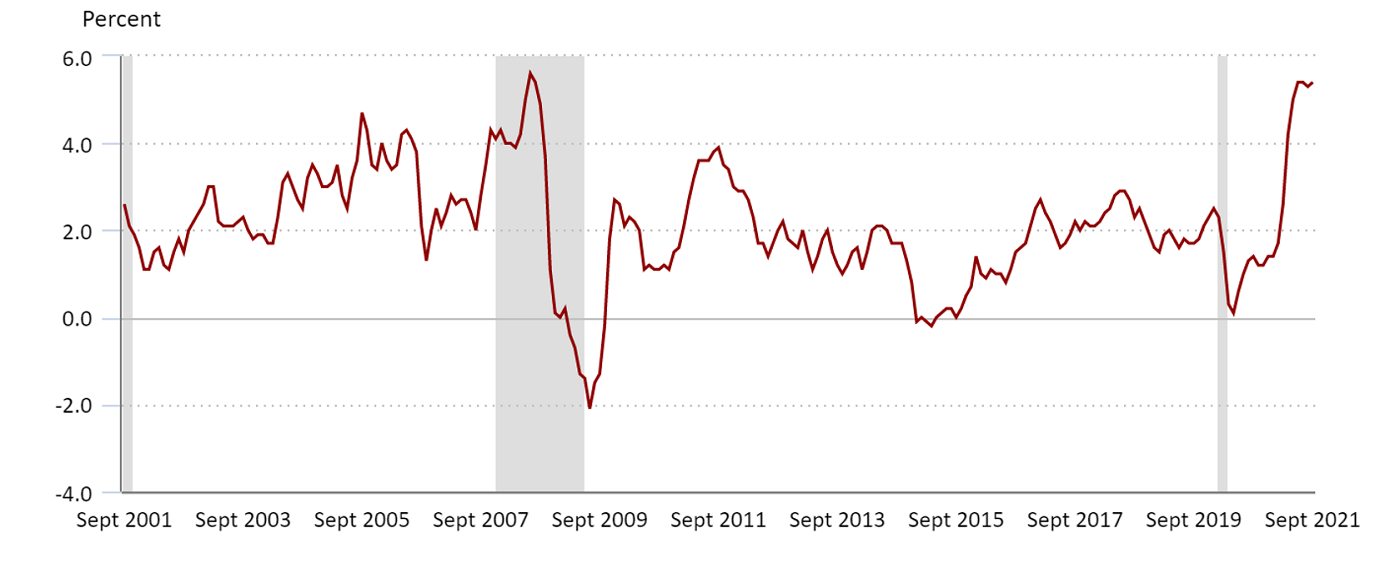

Figure 1: Consumer Price Index (US) - 12-month % change

Retail: Profit margins pressured by supply chain constraints

Retailers continue to benefit from pent-up demand driven by significant savings accumulated during the Covid-19 lockdowns. However, supply chain constraints, higher shipping costs, slower deliveries, and higher labour and raw material costs are limiting supply and putting pressure on profit margins. The impact of this varies across the sector as more resilient retailers – with a diversified supply chain and strong branding – are able to pass on costs to consumers through higher prices and fewer promotions.

As peak season approaches, the question is whether retailers will have sufficient inventory levels to meet demand, and thus sales expectations. Prioritising orders for the holiday season and chartering own cargo ships are some of the proactive supply chain management measures that retailers are taking. Some of these measures (such as the chartering of ships) are, however, not financially feasible for most retailers.

Steel: Supply constraints buffer against demand pressure

Steel prices recently hit new highs as demand rebounded strongly from the pandemic-induced slowdown. As a result, we expect Q3 2021 earnings to be very strong, driven by prices. Looking forward, on the demand side, the global semi-conductor shortage has hindered automakers’ volumes and is expected to continue to do so, but demand from other end markets has so far been supportive. The supply chain crisis and power constraints have the potential to impact industrial production, while the Chinese property crisis is also expected to lower demand.

On the supply side, increasing global power prices is pushing up the cost of production, and we have seen European steel producers adding surcharges to long steel prices to reflect this. Chinese steel output curbs are expected to constrain production in H2 2021, which should be supportive of global steel prices and may act as a counterbalance to potential softening demand. Combined with lower iron ore prices, this should limit the margin squeeze in the short term.

Automotive: semiconductor shortage impacting volumes, positive on pricing

Input cost and supply-chain linked inflationary pressures are impacting the auto sector with the semiconductor shortage, in particular, affecting both volumes and pricing. Original equipment manufacturers (OEMs) are enjoying all-time high margins (owing to strong pricing power, lower discounts and product mix), however, prolonged supply-chain disruption could negatively impact those margins.

Wage inflation is less relevant for the sector as the electrification revolution is matched by a manufacturing revolution that has seen automation and digitalisation improve productivity. Auto Parts have generally lower pricing power and are, therefore, more exposed to cost inflation; but are able to pass through some of it to Auto OEMs.

Utilities: Commodity-linked inflation provides a tailwind but increases regulatory risk

European electricity prices are set according to a marginal pricing model. This means that the marginal cost of the final plant needed to balance supply and demand sets power prices. In most European regions and for most of the year, the marginal plant is a gas plant which means power prices have been a function of both (i) gas prices (+201% year on year to €51.38/megawatt hour(MWh) and (ii) CO2 emission certificate prices (+82% year to date, to €59.59/million tonnes (mt).

Given strong one-year forward hedges from merchant-exposed utilities, we care more about the leakage of high spot power prices into longer-term forward power prices. As the two-year forward is up approximately 60% year to date in both France and Germany, commodity-linked inflation provides a strong tailwind to these merchant-exposed electric utilities, reducing future cash flow and earnings risks and, in turn, improving credit quality. For network utilities (remunerated on a regulated-asset basis), capex inflation also provides a positive tailwind as it ultimately translates into a higher regulated asset base (recorded at cost on balance sheet).

US homebuilders: Positive pricing power offsets supply chain disruptions

US homebuilders have enjoyed stellar demand coming out of Covid-19 lockdown driven by low interest rates, growth in personal savings, and other factors including the urban flight and changing consumer priorities. Strong demand was supported by tight supply after 10 years of low housebuilding rates.

Recently builders have been impacted by supply-chain issues which are constraining volumes, but strong pricing power has so far shielded earnings from the negative supply-chain effects, and margins have been strong. The bigger risk to homebuilders pertains to the potential impact of rates: if rising inflation prompts rate increases, this may stretch house price affordability, dampening demand. However, homebuilders have counter cyclical cash flows with the ability to conserve cash by reducing land purchases; this makes credit profiles relatively defensive.

Oil and gas: Higher prices are positive for producers

Since the end of the second quarter, oil prices have risen by 6% and WTI is currently trading at $80/barrel. In the same period, US natural gas prices have risen by 47% with spot Henry Hub currently trading at $5.38/thousand cubic feet (mcf). Both commodities are trading at the highest levels since 2014, in stark contrast to the low, and in some cases negative, prices of 2020.

For oil and gas producers, these upward pricing movements are positive given high operating leverage in their business. Any cost and wage inflation is probably having little overall impact on profitability in light of elevated commodity prices. Companies more exposed to natural gas production might benefit more given greater moves in pricing. That said, some companies, especially natural gas producers, have entered material hedges for the rest of 2021 and 2022, which are below current pricing levels and thus the positive impact from higher prices will be capped.

TMT: Most impact in tech

The recent rise in rates is having a varied impact across the telecommunications, media and technology (TMT) sectors. Typically, telecoms and media are less impacted by rising rates on account of their low exposure to raw materials and more stable workforces (e.g. engineers) reducing the impact of wage inflation. To date, these sectors have experienced limited restrictions in equipment procurement with telecom operators highlighting minimal delays to network deployment and continued access to digital billboards in media.

The indirect impact of inflation presents a risk to advertising (key revenue in media) as advertising demand softens for companies experiencing a more material impact on demand. Within technology, particularly manufacturing, there is greater exposure to raw materials as well as freight and delivery costs. So far, issuers have navigated higher costs with strategic increases in raw material inventory and although inflation has yet to have a material impact on our coverage, a number of companies have indicated that should raw material price levels persist, it could prompt cost negotiations with both suppliers and customers.

Specialty chemicals: Margin pressure expected

Demand has been robust for specialty chemicals, but meeting that demand has been more challenging. Some companies have already been impacted by supply chain constraints in areas such as shipping and logistics, and this has begun to adversely impact earnings. Downstream chemicals companies are also sensitive to raw materials inflation.

Raw materials prices for some specialty chemicals companies have already been elevated in 2021, driven by supply constraints from the winter storm in Texas and recent hurricanes in the US Gulf Coast. High natural gas prices are expected to exacerbate this trend. The big question is whether companies will be able to pass through costs. We believe they will eventually as they typically operate in specialised markets with limited customer churn which allows costs to be passed through. However, a lag in price increases may pressure margins over the next few quarters.

Packaging: Significant impact on plastics

All substrates were not created equal in the face of inflation. Key to assessing inflation exposure in the packaging sector is understanding:

- cost structure

- contract structure and

- market structure.

Metal packagers generally have strong pass-through mechanisms embedded in contracts and, therefore, minimal exposure to input-cost inflation. Strong demand for beverage cans has shifted pricing power towards can-makers which operate in a consolidated market structure. Glass packagers produce glass (as opposed to metal packagers which only convert metal sheets into metal containers) and therefore have a different cost structure: raw material, labour, and energy each account for approximately 20-25% of total costs, and freight costs also account for close to 20%. The industry operates under multi-year contracts with monthly/quarterly pass-through of cost provisions including energy. This means labour and freight inflation are likely to be the main components impacting glassmakers’ margins in the near term.

On the contrary, the plastic packaging industry has lower pricing power. Cost pass-through mechanisms (where they exist) come with a 60 to 90-day lag, which means resin prices can have a substantial impact on margins. This could squeeze out highly-levered resin packagers. Weather-linked disruptions – by taking petrochemical capacity offline – have also impacted volumes.

Source of all market data quoted in this report: Bloomberg.

Additional reporting by Eugenia Lara Armas, Credit Analyst.