Nurturing the green recovery through unparalleled spending

In December 2020, the European Parliament and members of the European Council reached an agreement on the next long-term budget called the Multiannual Financial Framework (MFF). The budget calls for spending of €1.1tn for the period covering 2021-2027. The two governing bodies also approved an additional €750bn of spending, called NextGenerationEU (NGEU), dedicated to finance the European recovery from economic dislocation following the Covid-19 pandemic.

This is an historic budget not only for its size – the largest ever at a combined €1.8tn – but also for its dedication to financing a green recovery. In moving to fulfil its obligations as per the ambitious European Green Deal, and as signatories of the Paris Agreement, the EU has said that “30% of the EU budget, under both MFF and NGEU, will be spent to fight climate change, the highest share ever of the largest European budget ever.”1

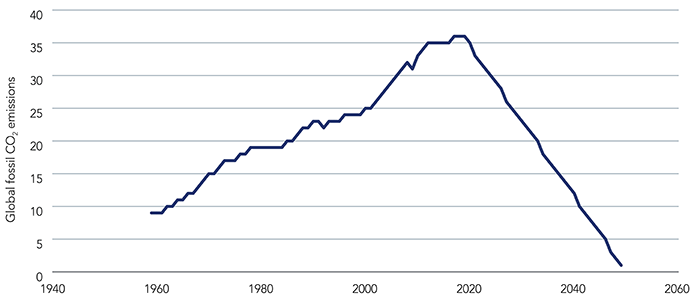

Figure 1. The drop in CO2 necessary to reach net-zero by 2050

Source: Data from the Carbon Disclosure Project (Global Carbon Budget, 2020).

The significance of nearly €550bn in climate-crisis spending over the next seven years cannot be underestimated. First, as we discuss below, the scale of this dedicated “green” spending is unlike anything we have seen before. Secondly, such spending addresses the challenge of having to respond simultaneously to the climate crisis, whilst also supporting economic growth, protecting jobs and backing technological and industrial innovation. Certain industries — such as real estate redevelopment, green mortgages, automobiles, power generation, hydrogen and renewable energy and transportation — will directly benefit from this kind of spending. Thirdly, given the EU Commission’s reliance on the bond market for financing the NGEU, it assures the permanence of the green bond market with the forthcoming of some €225bn in green bonds and sustainability-themed finance in general.

Finally, and perhaps most importantly, the above provides a catalyst for companies to decarbonise their production processes, as well as their product and services offerings. As stated by the European Commission, “the European recovery will need massive public and private investment”2. The path to net-zero, and the solution to the climate crisis, can only come from this kind of public-private partnership; there simply is no other solution. Setting aside rising “green” investor sentiment for the moment, with regulation and government spending of this kind, there is clearly no going back to “brown” once we have gone to “green”.

So just how green is the budget?

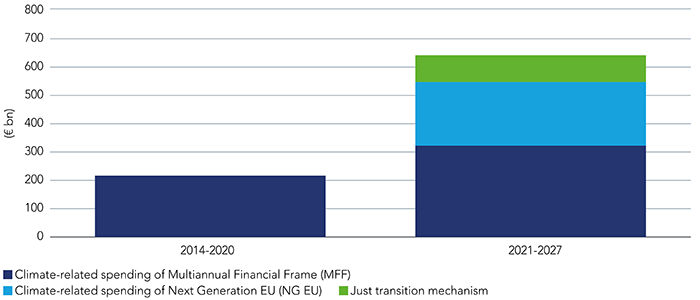

Some will say that the budget allocated to address the climate crisis and the European Green Deal does not go far enough, but let’s look at the “greenness” of the proposed spending. For the previous seven-year budget, which ran to the end of 2020, we estimate that around €215bn was allocated to support climate initiatives3. With the MFF and NGEU budget, that number jumps to an estimated €550bn, a rise of more than 150%.

Of course, much of that spend comes from the NGEU, for which the spending is front-loaded to cover the period from 2021-2024. If we also include spending for the Just Transition Mechanism – a €150bn initiative partially funded by grants from the NGEU and MFF which is designed to alleviate the social and economic challenges of those negatively affected by the green transition – total spending over that same period jumps to nearly €650bn. This represents a rise of just under 200%.

Figure 2. Comparison of EU climate-related spending for years 2014-2020 and 2021-2027 (€bn)

EU confidence creates conditions for green bond market to flourish

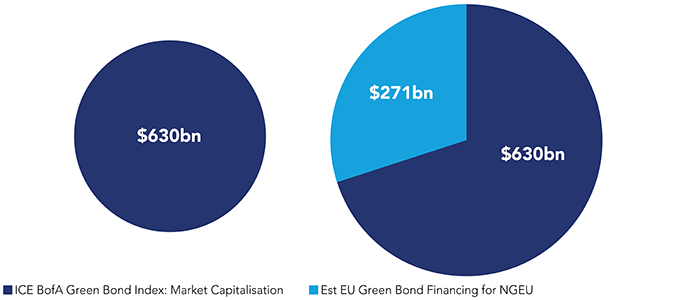

Having established the meteoric scale of the spending, let’s look at how the EU plans to raise capital. With insufficient funding from EU member states, the EU will rely heavily on bond markets to finance the ambitious plans of the MFF and the NGEU. More specifically, the President of the European Commission, Ursula von der Leyen, said in her State of the Union address on 16 September 2020 that, “30% of the €750bn NextGenerationEU budget will be raised through green bonds”4.

Thirty percent is a very sizeable issuance, amounting to €225bn over the four-year life of the NGEU. For context, the current market capitalisation of the ICE BofA Green Bond Index is approximately €525bn today (having been less than €100bn just five years ago). With its issuance of €225bn, the EU will easily become the world’s largest issuer of green bonds, eclipsing current leader – the European Investment Bank (EIB) – by a wide margin (the EIB today has just €45bn in outstanding green bonds).

Put simply, if the EU’s green bonds were issued today, the market would grow some 40%.

Figure 3. Pro forma impact of EU green bonds on the wider green bond market

Source: Bloomberg, ICE BofA Indices, as at December 2020.

A sure thing? Questions answered by the SURE bond issuance

We are unlikely to see any green bond issuance from the EU until H2 2021. That’s because the European Commission has set up a Technical Expert Group to assist in developing a suite of EU regulation, and this group has not yet codified a set of Green Bond Standards. How the EU might issue green bonds without finalising its own regulation for such instruments, in the first instance, is unclear.

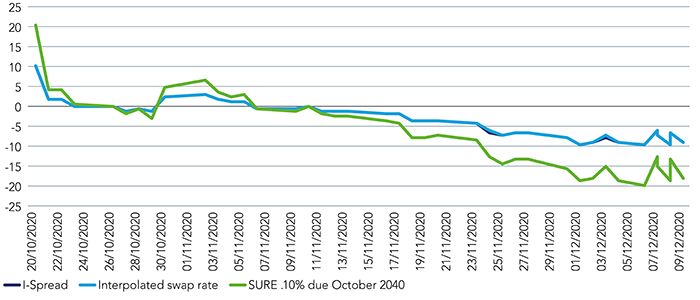

There are also questions around the demand for such a sizeable issuance, particularly when yields are well below 50bps, if they are even positive-yielding at all. In answering this latter question, it is useful to consider the EU’s recent €17bn, dual-tranche social bond issuance under the Support to mitigate Unemployment Risk in an Emergency (SURE) framework. Priced in October 2020, the deal was for an order book of an unimaginable €233bn, or a jaw-dropping 13.7x. The 2040 tranche of the SURE deal was issued at a yield of 10bps, or at a premium to the EU curve of 10bps.

Since issue, SURE has performed very well, and now trades well inside the same curve. Suffice it to say, if the EU’s treasury department is looking at demand for the SURE issuance, they should feel confident about the issue of €225bn in green bonds over a four-year period.

Figure 4. positive performance of SURE bond issuance

Source: Bloomberg, as at December 2020.

Lay of the land: the EU Budget stands to lower the cost of capital by raising the profile of green innovation

The fiscal stimulus plan outlined above certainly takes the climate crisis seriously. When you combine the EU’s commitment of €550bn over the next seven years with the principles of the European Green Deal and the regulatory proposals of the EU Taxonomy, it is clear that there is no going back on the green transition. The prospects of investing in a secular trend that is underwritten—at least in part—by government provides confidence that the green bond market will continue to grow, likely at an accelerated rate. We anticipate that, overtime, the EU budget will trigger a greater supply of sustainability-themed debt issuance, which will in turn deliver even more growth and depth to the sustainable-themed debt capital markets.

Moreover, as government loans and grants flow into certain industries — as shown in figure 5 —we would expect the cost of green capital to drop. Such support again provides assurance of the EU’s long-term commitment to emerging decarbonisation technologies, which reduces the risks associated with investing and in turn lowers hurdle rates, thus driving down the cost of capital. As such, we believe that the “greenness” of the EU’s budget will unlock further opportunities in green financing, including the issuance of more green bonds, loans, asset-backed securities (ABS) and sustainability-linked debt. Combined with equity, these opportunities complete the capital stack in support of green economic activities. As such, the probability of simultaneously financing positive environmental change, whilst also creating economic value, is increasingly likely with the greening of the EU budget.

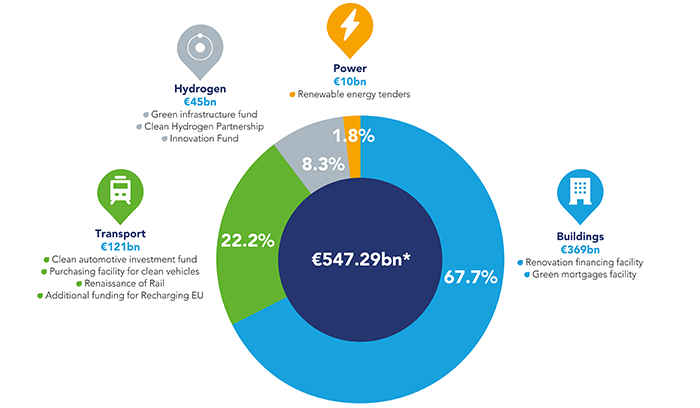

Figure 5. Breakdown of climate-related spending in the EU (2021-2027)

Source: EU Budget 2021 approved: supporting the recovery | News | European Parliament (europa.eu)

*The EU Commission has pledged to spend 30% of overall spending (€1,824.3bn) on climate related causes

The greenness of the EU budget: implications for fixed income and industry

1 See https://ec.europa.eu/commission/presscorner/detail/en/QANDA_20_2088 for more information.

2 See statement on #NextGenerationEU, 18 September 2020.

3 Source: see footnote to figure 2. See also Next Generation EU (europa.eu) for more information.