The MD’s outlook

What significant developments for private markets could take place in 2026?

Asset classes within private markets are impacted by the same macro factors as their public-market counterparts, although the method and timing of those impacts may vary. Digitisation, demographics, and deglobalisation are significant mega-trends that will continue to shape private markets in 2026 and beyond.

At the industry level, we expect deal activity – which showed signs of life in H2 2025 on hopes of a normalisation of interest rates – will continue to gather positive momentum in 2026. With this increased deal activity, private asset classes are poised to deliver greater capital distributions to investors from older vintages. This should, in turn, fuel new allocations into private markets from here. When this happens, we believe investors will look to add specialist strategies, rather than generalist, diversified strategies.

The investor mix should also continue evolving to include more Wealth Management clients (likely through evergreen structures). According to Morningstar, in the US alone, these structures collectively managed US$250bn of client capital at the end of 2022 rising to US$450bn by mid-2025. Most industry commentators expect this allocation to only grow in the coming years.

Despite significant interest from governments for defined contribution (DC) pension schemes to increase allocations to private markets that invest in their countries, the industry is very much in the early stages of this becoming a reality at scale. Will 2026 be the year that this ultimately happens? While allocations will increase, we expect the year ahead will be dominated by discussion and, possibly, a decision to remove the final barriers to entry before allocations at scale are possible.

What’s your outlook for 2026?

After several years of rising interest rates, slowing growth and high inflation, coupled with an uncertain M&A pipeline, the market is settling into a more predictable environment. For managers and investors, this should present an attractive mix of increased deal flow, lower economic turbulence and yields that are attractive when compared with pre-Covid levels.

Clearly, there will still be challenges on the horizon. Deployment will remain competitive on the back of a cycle of strong fundraising which has led to a great deal of dry powder in the market. Some unitranche direct lenders, with higher returns targets, will seek to compete by providing aggressive loan terms to borrowers – which could mean we continue to see aggressive structures appearing in the market. But also, borrowers that have struggled to cope with a higher interest rate and a slower growth environment over the past few years may find it harder to meet covenant tests, which are now getting tighter as the loans come nearer to maturity. As a result, we expect default levels will increase over the next year.

How will interest rates affect the market?

By 2026, we expect interest rates in Europe to be lower than the highs of 2023, even if they don’t come back to the ultra-low levels of the previous decade. This will be the sweet spot for direct lending. Borrowers will get the benefit of lower interest costs, reducing the pressure on their cashflows, while investors will continue to make attractive risk-adjusted returns on their investment. The reduction in interest rates will also encourage private equity to restart investing, after a quiet period over the last couple of years.

One of the defining features of 2024/25 was the buildup of unsold private equity assets. Many sponsors held on to assets longer than usual, waiting for valuations to stabilise. This backlog will clear in 2026 and should lead to a firmer pipeline of transactions – buyouts, add-ons, and refinancings – which will feed directly into mid-market direct lending volumes.

How restrictive will lending be in 2026?

While some lenders will try to compete with more aggressive loan terms, lending discipline will continue to be of utmost importance, particularly as European economic growth is likely to remain modest. As a result, direct lenders should continue favouring non-cyclical sectors. Similarly, documentation will generally remain tighter than it was pre-Covid. However, with interest rates falling, we expect to see a return to complementary loan products in the market. Traditional senior secured loans and unitranche will remain the core products, but we are likely to see increased use of delayed draw facilities, second lien, and junior payment-in-kind (PIK) instruments to facilitate acquisition strategies. With the total cost of borrowing having come down, borrowers will be able to use these complementary loan instruments with much better effect. This will mean that strategies like credit opportunities will become much more popular with investors.

What regulatory changes could come into effect in the coming year?

The year ahead will see increased regulatory scrutiny for direct lenders. This will be centred on valuation practices, liquidity management of semi-liquid structures, and the levels of leverage offered in transactions. While we don’t expect any restrictive rules to be implemented in Europe, rising scrutiny could increase reporting requirements and slow down deal execution as managers deal with regulatory demands. Well-established managers with strong governance and transparent processes, and in-house reporting teams should benefit.

We expect 2026 to be an exciting year as the market slowly comes back to life. Managers who have stayed disciplined and adopted conservative lending strategies in the past will benefit in this new market and will be able to deploy loans to the many new lending opportunities that will be bought to market. Those who have been aggressive and reckless in the past will be busy dealing with issues in their existing portfolios.

What’s your outlook for 2026?

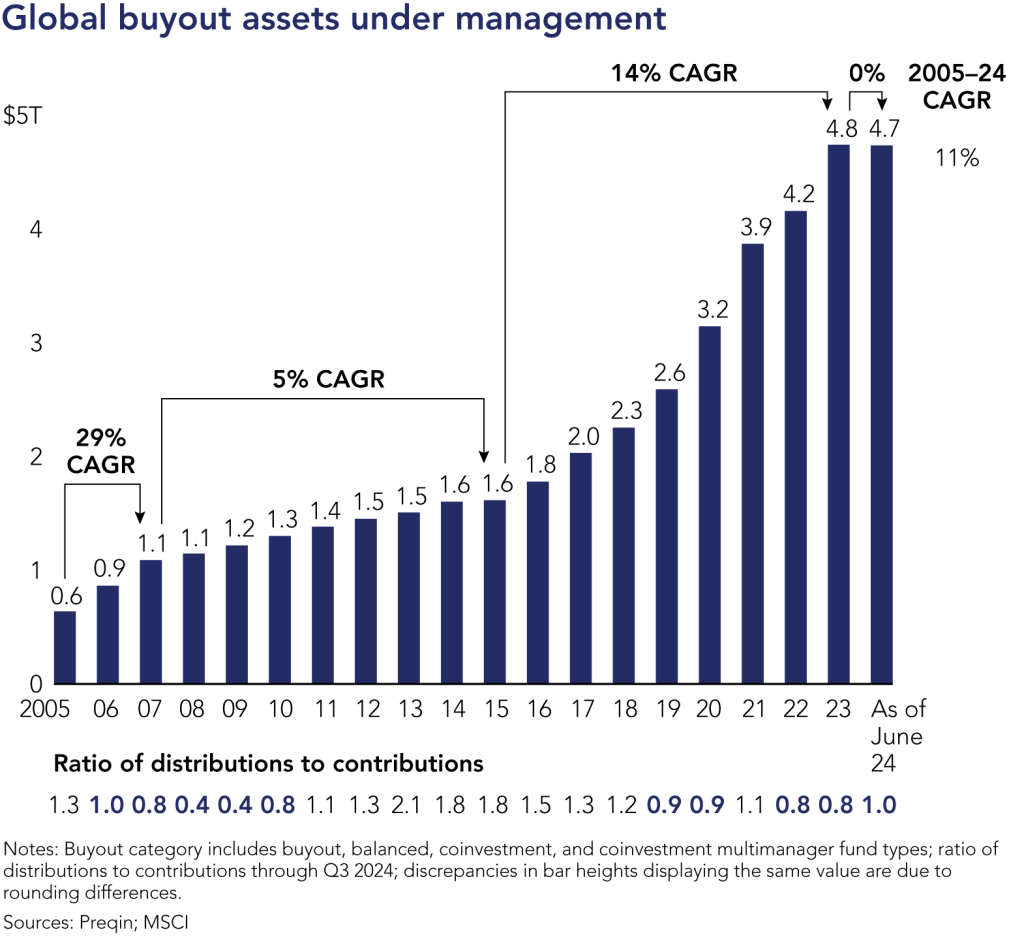

We believe 2026 will be another year of evolution as the industry goes through a period of historic upheaval. After a bumper decade and a half, private equity faces a challenging environment for exits and fundraising. Distributions paid to investors as a percent of industry net asset value are at their lowest point in history, two-thirds lower than industry norms that occurred up to and through the Covid pandemic.

The global buyout industry doubled between 2019 and 20241 – but it’s now flattening out as institutional investors become relatively fully allocated. From here, distributions are needed to allow investors to deploy more capital. The IPO window remains muted compared to the years before and during Covid. This challenging fundraising environment is particularly acute at the lower end of the market with its lack of scale and fundraising resources.

What structural changes could help the industry address these challenges?

Creative solutions are emerging across the industry to help General Partners (GPs) generate liquidity. The secondary market, and especially the GP-led segment, continues to be a bright spot, solving real problems for GPs and Limited Partners (LPs). Beyond secondary strategies, though, there’s also been a growth of creative financing solutions for GPs and LPs as the industry matures.

Fundraising has changed as well – with the majority of net new dollars coming from the private wealth channel and, potentially, soon the 401(k) market too. On this, our view is that private equity is an essential asset class and we believe it belongs in every balanced portfolio. Opening up the industry to investors who have not historically had access should be a good thing for all parties. A large proportion of the newly raised dollars will initially go to scaled firms with the infrastructure and resources to tap into the opportunity. Because of this, capital will continue to aggregate at the mid and upper end of the market.

What other changes are taking place?

The industry is rapidly evolving from a people point of view. The explosion of private equity AUM has coincided with an influx of professionals into the industry, giving rise to a vast ecosystem of highly talented deal-doers and investors. As the industry changes at the people level, the environment for talented professionals to change firms, start their own firms, or focus on deal-by-deal strategies has never been better.

Even in this tougher exit environment, the private equity opportunity remains as vast as it is compelling. Merely focusing on historical industry returns and obtaining private equity exposure is not enough. Products are changing, incentives are changing, and, in 2026, selection will be key.

What kinds of strategies could do well in 2026?

Investors will benefit from strategies with pathways into harder-to-access areas of the market where less capital is flowing (such as the lower mid-market). Strategies could also do well if they have a playbook for investing alongside talented deal-doers no matter where they reside (old firm, new firm, funded or unfunded, etc.). Strategies focused on creating clear exit pathways are another area of opportunity – particularly those focused on smaller companies, multiple value-creation levers, operational upside, or exposure to industries with long secular tailwinds. These are businesses that are attractive today and likely to be even more compelling to buyers in five years’ time.

1 Preqin, 2025

What’s your outlook for 2026?

Cyclical and structural changes in real estate are one area of risk and opportunity worth highlighting for the coming year. While capital values have undergone a sharp correction, occupier markets have remained surprisingly resilient. For property owners, the past few years have been challenging, but this was no crisis. It was a cyclical adjustment in asset pricing; not a black swan event. Changing market conditions drove illiquidity of real assets, with valuations eventually reflecting this. As transaction volumes begin to recover, it’s now tempting to declare the end of that difficult market. But it’s also crucial to recognise that cyclical and structural shifts can occur simultaneously.

Consider hybrid working as an example of the latter. It’s had a profound impact on office rents and, while prime offices are commanding record-high rents, there’s also significant weakness in the broader office sector. Obsolescence is a real risk for older buildings, and outside major cities, new office development has become largely unviable as rents fail to keep pace with construction costs. Hybrid work hasn’t changed what we do but it has changed where we do it. And for an immovable asset class like real estate, the ‘where’ matters deeply. Even if yields tighten, parts of the office sector will likely not see a recovery in occupier demand.

The AI revolution adds another layer of disruption. It’s driving huge energy demand and needs data centre infrastructure to support it. But the pace of technological change brings the risk of faster depreciation of older assets. In the wider economy, AI will reshape tenant activity, sometimes enhancing tenants’ ability to pay rent, sometimes undermining it. As business models evolve, so too will the appeal of certain locations, and with that, rental tones will shift.

So even if we do see a cyclical rebound, could we be simultaneously facing structural changes in the occupier market? Are tenant failures a concern? Certainly, a weakening economy could lead to rising tenant defaults, with limited prospects for replacing tenants. We believe both real estate owners and lenders must remain vigilant, closely monitoring tenant mix and sector exposure.

What makes real estate debt an attractive asset class in 2026?

One of the enduring strengths of real estate debt, particularly senior loans, is its potential to outperform even when the underlying asset underperforms its underwriting. Because of this, it continues to play a vital role for institutional investors seeking diversification within their real estate allocation. The uncorrelated return profile of the asset class compared to direct real estate strategies, makes for a powerful complement – and, although return targets for real estate debt are typically lower than for direct real estate, they’ve proven to be much more resilient in the face of previous market disruptions.

The yield question is also worth considering. For those seeking higher yields, real estate credit could be an interesting option, particularly at shorter hold-periods. Higher-yielding strategies investing in higher-leverage loans or subordinated loans are likely more correlated to real estate – but they do so with negligible or negative transaction costs. This means debt investors (unlike real estate owners) have the potential to begin earning positive returns from day one. In an uncertain world, that’s worth something.

Lending levels held up well during 2025, and rising real estate transaction volumes for the coming year are a positive development. Yet, while yield forecasts show some capital growth in certain submarkets, broader expectations are reasonably flat. We, therefore, remain cautious in our underwriting. We continue to seek out strong relative value and encourage diversified exposure to the occupier market.

What’s your outlook for 2026?

It doesn’t take a crystal ball to predict that geopolitics will continue to shape the global economy and, therefore, the outlook for all private markets including infrastructure, in 2026. Globalisation is in retreat, and what comes next will take time to emerge. Support for free trade, grounded on a rules-based economic order, has always depended on mutual self-interest – not shared values, shared political systems or shared religious beliefs. Keep your friends close and your enemies closer by creating mutual economic dependencies. Today, however, shifting geopolitical dynamics increasingly prioritise independence, not interdependence.

Consequently, most developed economies, including the UK, will double down on onshoring key sectors: energy, data and defence. Sovereignty – to mitigate vulnerabilities by minimising dependence on others – will trump free trade, the climate emergency and economic rationality. Technological sovereignty is already beyond most countries’ reach. Economies will become either US- or China-technology reliant. Over time, international trade and capital flows may increasingly trace military alliances.

Private investment will be significantly influenced by these trends. As an infrastructure investor, our focus will remain on the driving force that is electrification of the economy. Electrification, mainly powered by renewable energy, intersects with the key trends of energy security, data sovereignty and decarbonisation of the economy. This is where we will be seeking to allocate capital in 2026 and beyond.

UK Inflation and base interest rates are within historic ranges

What’s your outlook for the UK?

Despite the headlines, today’s macro-economic conditions in the UK are historically familiar – with current inflation, base interest rates and gilt yields all within ranges that have prevailed over the past 200 years.

Today’s base rate, for instance, may appear high compared to the extremely low levels experienced in the 12-year period following the 2008 financial crisis, but that period was unprecedented. Less typical is the weight of the UK’s national debt stack – approaching 95% of GDP. Levels at this rate have not been seen outside periods of major conflict.

All of this means that the outlook for inflation, and therefore the base rate, is nuanced. Absent sovereignty drivers, and the elevated levels of national debt straining public finances, we’d expect the twin megatrends of technological advancements and demographic shifts, such as lower birth rates and aging populations, to be powerful deflationary forces. In the UK, strategic onshoring of key sectors will come at a cost that, combined with the burden of servicing elevated levels of national debt, is likely to keep inflation and interest rates remaining close to 2025 levels, making the UK an outlier compared to the EU and possibly the US.

These factors are all relevant to the relative attractiveness of infrastructure as an asset class. It’s no coincidence that what may turn out to be the golden age of infrastructure investment coincided with the period of ultra-low rates and gilt yields. The hunt for yield with downside protection attracted unprecedented levels of capital. The challenge in 2026 and beyond is to continue to attract capital based on fundamentals while avoiding strategy drift and importing outsize risk to justify the higher returns investors are now seeking.

What’s your outlook for 2026?

As we look ahead to 2026, the UK real estate investment market remains cautious. But in times of global uncertainty, subdued investor sentiment, and transaction volumes that continue to lag historic norms, it is helpful to be reminded of the fundamental purpose of real estate: that being to facilitate economic and social activity. The built environment shapes how and where we live, work and play, how and where we educate and provide care, and how and where we store and distribute physical goods and digital data. The astute investor will identify occupational need borne from the structural drivers of demand – demographics, deglobalisation, digitisation, decarbonisation (and arguably now defence) – and will deliver relevant real estate responses. The reward will be resilient income streams.

Capital values are unlikely to stage a strong recovery in 2026. Against an expectation that gilt yields may fall in 2026 it is likely that the real estate risk premium will expand rather than yields will compress. And whilst some rental value growth might be seen in some segments (best offices for example), income will remain the dominant driver of total returns. This of course is as it has been over the long-term – more than 80% of returns have been derived from income since 1986 (MSCI) – and is fine.

We expect investor appetite to continue to favour specialist strategies, particularly in the “beds and sheds” sectors. Living assets – across their various formats – are expected to top allocation lists, supported by structural undersupply and emerging political tailwinds that are aimed at boosting delivery. Data centres remain a widely cited preference, though translating this into transactions may prove challenging given constraints on power availability and unknowns around the underwriting of exits. Development activity will remain viability-challenged, likely to be tolerated only where projects promise the delivery of strong income generators and, increasingly of interest for some, a return on purpose.

Ultimately, 2026 will reward disciplined investment strategies that align with non-discretionary demand, deliver relevant supply responses, and embrace operational excellence. Real estate remains a dynamic asset class – capable of adapting to societal needs and delivering attractive, risk-adjusted returns driven by durable income in an era of elevated interest rates.

Further themes that will matter next year: