Fast reading

- Credit spreads have tightened significantly following geopolitical de-escalation, reducing the scope for further capital appreciation.

- Macro conditions and corporate fundamentals continue to underpin credit, but uncertainty raises concerns about market complacency.

- Investors are increasingly focusing on income opportunities, favouring selective high-yield credits, CLOs and subordinated bank debt.

Credit spreads have tightened in response to de-escalation efforts between Iran and the US. While credit fundamentals remain supportive, stretched valuations and lingering uncertainty suggest a more measured approach to risk-taking in the months ahead.

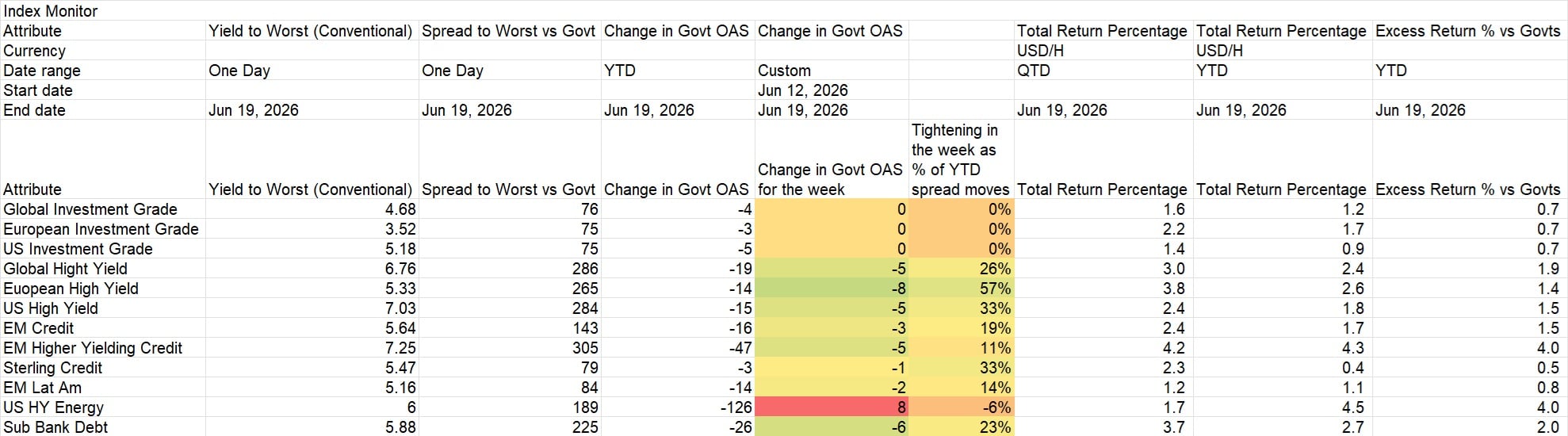

Risk premia have steadily compressed in recent months as the US attempts to draw a line under the conflict in the Middle East. The Memorandum of Understanding (MoU)1 signalled the final leg of the rally since the wides observed in March. The tightening was particularly evident in Europe, reflecting the region’s vulnerability to energy supply disruptions. Higher beta segments, especially high yield, led the tightening in spreads (Figure 1). Investment grade spreads, by contrast, remained stable.

Energy sector reverses outperformance

The most notable divergence has been in the energy sector. High yield energy bonds, which had previously delivered excess returns amid elevated oil prices, moved wider (Figure 1). This marked a reversal of year-to-date spread tightening in the sector, positioning it as a clear outlier. The shift may provide some relief to sustainability funds with limited energy exposure.

Figure 1: Spreads tighten but not within energy

Source: ICE BofA, Bloomberg, Federated Hermes, as at 19 June 2026.

Despite geopolitical uncertainty, the broader macroeconomic environment continues to provide underlying support for credit markets, according to our credit strategy committee’s assessment. While stagflation risks persist – particularly in Europe – the US and many emerging market (EM) economies remain on relatively solid footing, underpinned by post-global financial crisis reforms and stronger policy discipline.

Corporate fundamentals are similarly supportive. However, we have modest upward revisions to both macroeconomic and fundamental outlook scores, reflecting expectations that reduced geopolitical uncertainty could encourage renewed corporate investment and growth initiatives.

Markets now appear to have begun to refocus on domestic fiscal and monetary policy considerations. Gilts rallied in late May in response to the falling oil price, but performance appears to have decoupled from the energy shock in recent weeks. A falling oil price was not enough to prevent a sell-off in gilts following the news that a new prime minister is set to take office in the UK.

Markets now appear to have begun to refocus on domestic fiscal and monetary policy considerations.

In the US, a more hawkish policy stance has further complicated the outlook. Recent Federal Reserve messaging – characterised by reduced forward guidance and limited reassurance for dovish expectations – triggered a sell-off at the front end of the yield curve and pronounced flattening. Persistent inflation and resilient labour markets have led investors to price in the possibility of further rate hikes, reversing earlier expectations of easing.

This shift has also driven a notable appreciation in the US dollar, which has strengthened significantly since its trough earlier in the year (Figure 2). A stronger US dollar is expected to continue supporting EM corporates in commodity sectors, particularly those generating revenues in hard currency terms.

Figure 2: US dollar regains strength

Are markets complacent?

Technical conditions – the supply-and-demand dynamics in credit markets – have improved in recent weeks, which has prompted us to upgrade our assessment.

However, sentiment remains a key point of contention. It is our concern that markets may be displaying a degree of complacency. Despite the apparent diplomatic breakthrough, the MoU offers limited concrete assurances of long-term stability, and uncertainties remain regarding the duration and extent of inflationary pressures stemming from earlier supply disruptions.

With spreads now trading through pre-conflict tights and approaching long-term compression levels, questions remain over the scope for further capital appreciation.

Limited upside shifts focus to carry

Any reduction in uncertainty appears largely reflected in current spread levels, suggesting limited further upside from capital gains. As a result, investment focus is shifting towards income generation. Select opportunities were identified in single-B rated credit, particularly those less exposed to consumer demand trends, where relative value remains versus higher-rated BB issuers.

Highly rated tranches of collateralised loan obligations (CLOs) were also highlighted for their attractive carry profiles, aligning with a broader preference for quality at this stage of the credit cycle. In addition, subordinated bank debt continues to appeal, supported by significant deleveraging in recent years and strong underlying fundamentals.

Finally, the strength of the US dollar has created relative value opportunities in European credit markets on a cross-currency basis, improving all-in yield prospects for global investors.

BD017823