Atoms.

The. Single. Most. Important. Units. Of. Reality.

Or as renowned Nobel Prize-winning US physicist, Richard Feynman, replied when asked to distil the essence of all scientific knowledge into one sentence, “all things are made of atoms”.

Feynman expanded the concept in his eponymous series of lectures on physics, noting: “If we were to name the most powerful assumption of all, which leads one on and on in an attempt to understand life, it is that all things are made of atoms, and that everything that living things do can be understood in terms of the jigglings and wigglings of atoms”.1

But the atomic theory goes way back to ancient times, for example, in thoughts expressed by Roman poet and philosopher Lucretius around 60 BC. In his classic poem, De Rerum Natura2 it is posited that the universe is an expanse of empty space (a void), peppered with an infinite number of irreducible particles of matter (or atoms).

Feynman and other leading lights of modern physics, of course, went far beyond the poetic notions of Lucretius, adding an exceptional amount of intellectual rigour and mathematical detail to create two internally consistent, but collectively incompatible, models of reality. On one side sits the ‘Standard Model’ of physics that marries three sub-atomic forces (electromagnetic, weak, and strong nuclear) into seamless relationships. Then, standing alone, Einstein’s theory of general relativity introduces gravity as a rogue fourth force, bending spacetime and confounding efforts to conform with Standard Model thinking.

And despite decades of research, the several ‘theories of everything’ touted to date – a group including string theory, loop quantum gravity and new entrant, entropic gravity – have yet to square the circle (or cube the sphere).

While physicists clash on the theoretical borders of reality, their real accomplishments in revealing some of the fundamental atomic operations of nature remain impressive. By contrast, our understanding of the modern economy and financial markets has made far less progress.

For instance, currencies – in many ways the ‘atoms’ of economies – are still shrouded in almost medieval mystery and constrained by operational systems unfit for the Digital Age.

The decline of physical cash and the advent of ‘cryptocurrencies’, however, has triggered a race among the still-dominant monetary authorities of central banks to quickly get up to speed on the future of money.

Today, policymakers in most major jurisdictions, and many minor ones, are seriously investigating the potential of central bank digital currencies (CBDC) to create a nuclear revolution in the financial core.

Figure 1. Features of traditional vs. CBDC currency

Source: Federated Hermes International, International Monetary Fund (IMF), Riskbank, European Central Bank (ECB)

In recent months, central bankers from Europe to Japan have made several speeches and media commentaries on CBDCs. Last year, the Bank of England (BOE) produced a seminal paper outlining the principles and pragmatisms of a CBDC for the UK; at the same time, the US Federal Reserve turned a full 180 degrees from its previous opposition to the concept to scoping out a CBDC implementation plan.

Meanwhile, the Chinese government has moved beyond talk to a real-life CBDC trial, setting an experimental example for other central banks.

Everything is made of money: the what, why and how of CBDCs

In a rough approximation of operational reality, CBDCs would simply act like an electronic version of the banknotes and coins used as sovereign-backed money for thousands of years. As explained by the Swedish central bank, Sveriges Riksbank, in a recent primer3, monetary authorities would issue CBDCs for consumer use in everyday payments just like physical cash, denominated in the national currency and exchangeable at par with commercial bank money.

This simplistic definition, however, ignores many of the practical technical, social, and political challenges central banks would face in implementing CBDCs compared to printing banknotes – and hence explains why all are mapping fundamental currency models to digital avatars.

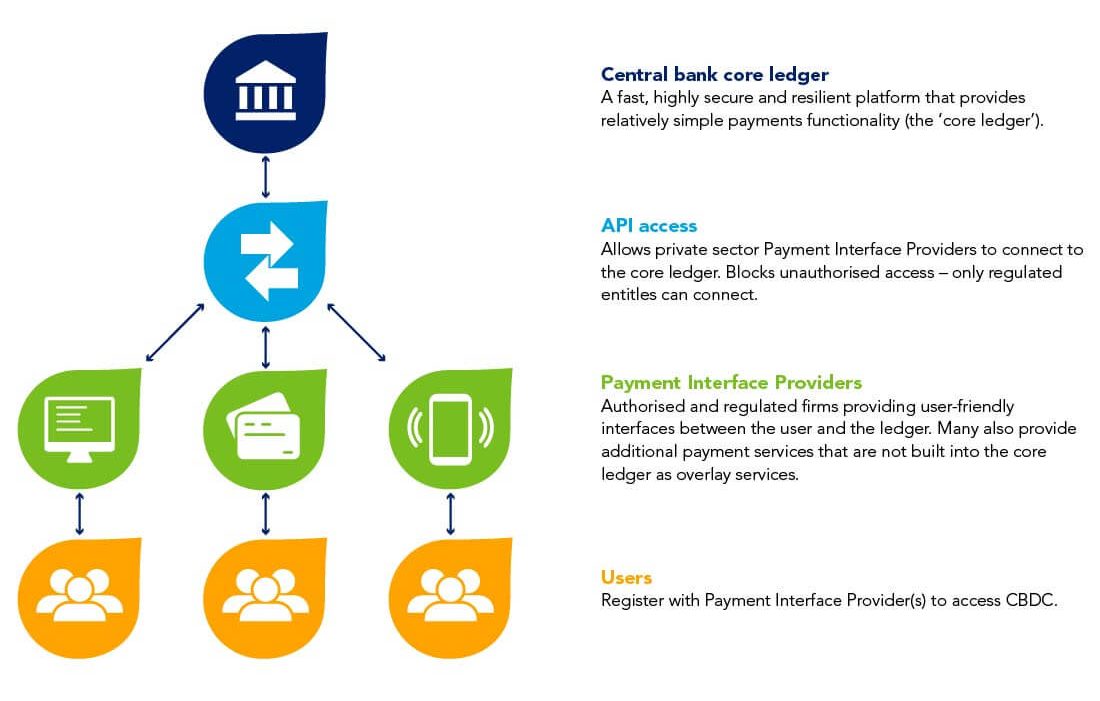

Figure 2. The CBDC platform model

Source: Federated Hermes International, Bank of England.

As mentioned earlier, physical cash has been falling out of favour for many years, as consumers welcome the convenience of card-based electronic transactions. According to a Bank of England (BOE) discussion paper, Central Bank Digital Currency: Opportunities, challenges and design4 the use of cash as a means of payment in the UK fell from over 60% of transactions in 2006 to 28% by 2018.

The Covid-19 pandemic has accelerated the decline in cash usage in economies across the world, with many pundits suggesting CBDCs could provide a long-term substitute.

Regardless of the noise emanating out of private ‘crypto’ markets, switching the global economy over to digitally enhanced central bank currencies is no easy task. Monetary authorities, who must answer to governments and societies, face some very complex CBDC design decisions that require careful calibration with existing systemic arrangements.

Central banks will want to make CBDCs attractive enough that they are used – but not so attractive that they draw funds away from the banking system.

CBDC risks, though, are balanced against several benefits, including:

- Operational resilience – CBDCs will be built to the highest technical standards, creating a more robust system that should make payments outages – such as the 2018 glitch caused by a Visa hardware malfunction – far less likely;

- Alternative to the US dollar as a reserve currency – domestic economies could potentially better protect themselves against exchange shocks triggered by volatility in the dominant US dollar – a power former BOE governor Mark Carney labeled as a “destabilising asymmetry” – with strong CBDCs;

- Financial inclusion – a well-designed CBDC could help the 1.7bn adults globally who currently have no access to banks;

- Improve competition on payments – CBDCs may reduce the duopolistic pricing power of Mastercard and Visa;

- lower credit risk – central banks don’t go bust; and,

- Potential powerful monetary tool – central banks could use CBDCs to more efficiently implement monetary (or even fiscal) policy, making the issuance of so-called ‘helicopter money’, for example, a simple task.

For commercial banks, however, the prospect of CBDCs come with some anxiety, posing a threat both to their own survival and the stability of the broader credit-based financial system.

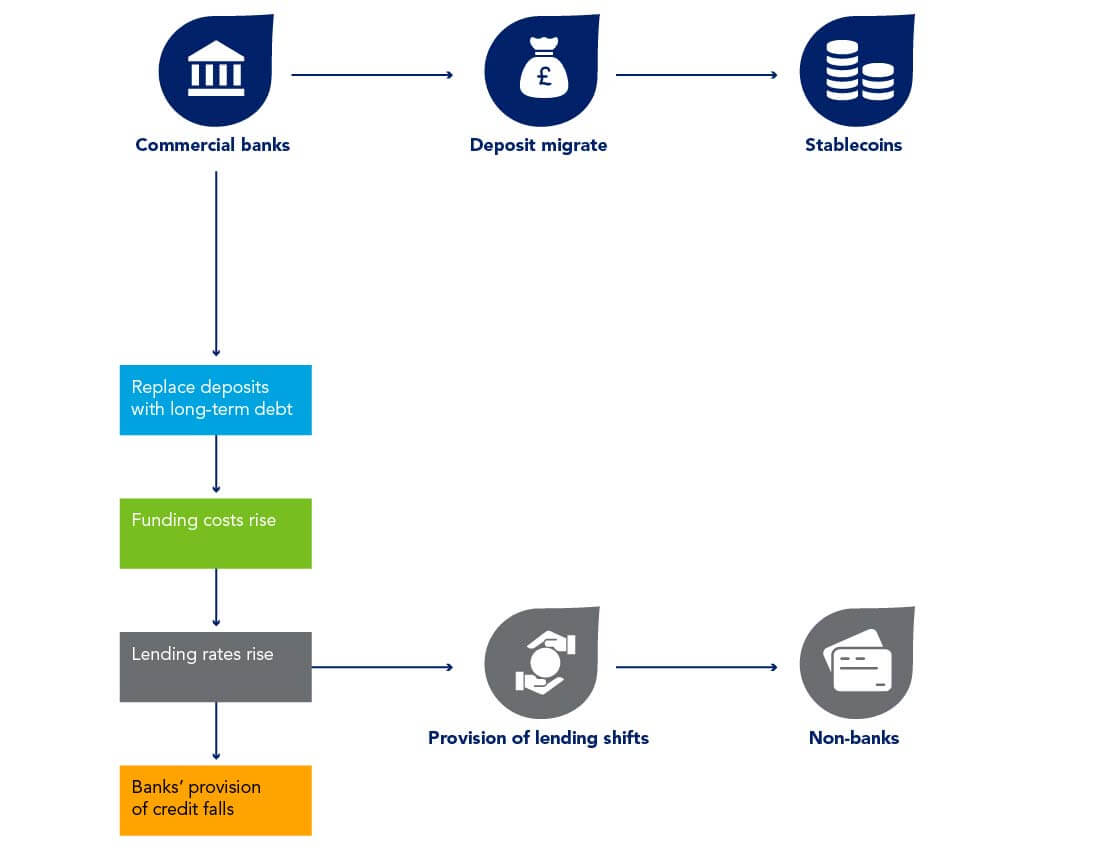

Figure 3. An illustrative example: what might CBDC mean for banks?

Source: Federated Hermes International, Bank of England

According to the central bank estimates, and depending on design features, CBDCs could draw up to €1trn of sight deposits away from European banks, compared to €1.4trn banknotes in circulation. At flows of this magnitude, commercial banks in Europe could face liquidity ratio stress and see earnings unmoored from interest rates.

Thankfully, central banks are aware of the disintermediation dangers presented by unconstrained CBDCs and have proposed several ways to limit the risk. For example, the European Central Bank (ECB) has floated the idea of capping CBDC holdings to €3,000 per citizen.

All the central bank CBDC reviews and consultation papers also devote a lot of attention to managing the financial stability risks of digital currencies. For example, the ECB notes: “The digital euro should be an attractive means of payment but should be designed so as to avoid its use as a form of investment and the associated risk of large shifts from private money (for example bank deposits) to digital euro.”5

And the BOE does a masterful job of describing how a switch from cash to CBDC could be safely negotiated in the previously mentioned paper6.

Clearly, central banks are thinking hard about how to contain any fallout for the financial system if governments choose to opt for the nuclear option of CBDCs with remuneration (interest payments), tiering and holding limits all on the table.

For the moment, monetary authorities are mainly preoccupied with how a CBDC could be introduced smoothly into their own respective jurisdictions, but some are also weighing up the global consequences.

The BOE paper, for instance, notes: “Individual domestic CBDCs could be designed around a common set of standards intended to support interoperability. This might enable ‘atomic’ transactions between CBDC systems: where the transfer of CBDC in one currency is linked with a transfer of CBDC in another currency, in a way that ensures each transfer occurs if — and only if — the other does.”7

As in physics, the CBDC theory of everything remains elusive but we now, at least, can make out the jigglings and wigglings of the atoms.

Ernst Mach (1838 –1916), Austrian physicist

1 Richard P. Feynman, The Feynman Lectures on Physics (1963)

2 Lucretius, W H. D. Rouse, and Martin F. Smith. De Rerum Natura. Cambridge, Mass: Harvard University Press, 1982.

3 See Sveriges Riksbank, Payments Department and Research Division, On the possibility of a cash-like CBDC (February 2021)