On November 8, the blood moon eclipse pushed more earthbound topics – such as war, inflation and near collapse of the UK financial system – momentarily to the sidelines as people around the world paused to marvel at the blushed red hues of our nearest celestial neighbour.

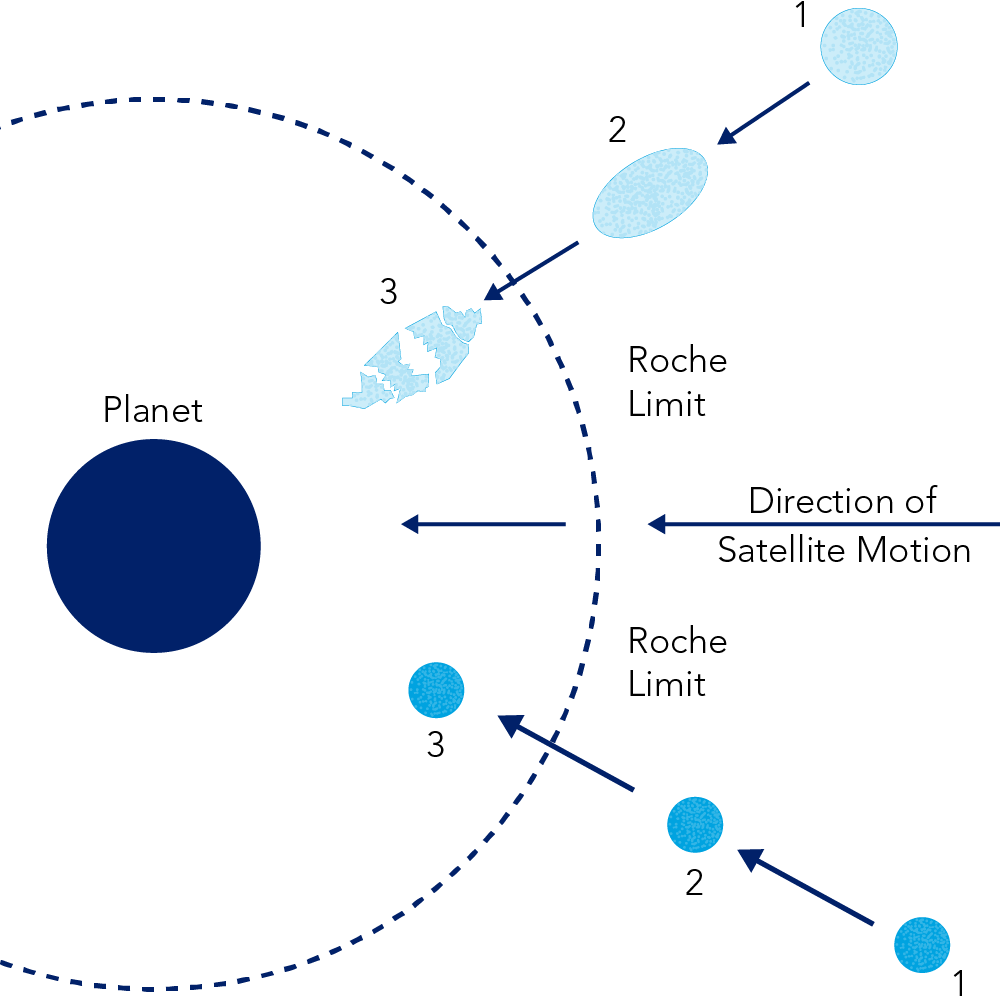

Some may have gazed up and wondered how the moon manages to stay there at all. While gravity explains why the moon remains in orbit, it was French polymath Édouard Roche (1820–83), who postulated why it’s unlikely that earth’s only natural satellite will come crashing down any time soon.

It was Roche who put his name to the calculation that sets the minimum distance to which a large satellite can approach its primary body without gravitational forces ripping the junior partner to pieces.

Once an orbiting satellite passes the Roche limit (or ‘lobe’) – the theoretical threshold is about 2.5 times the radius of the larger body if both are of similar composition – tidal forces overcome the internal gravity holding it together.

Figure 1: the Roche limit

The moon is about 21 times the distance outside the Roche limit with Earth; so the lunar lightshow (available in blue, blood, yellow or white) will continue for some time.

But what happens when planet-satellite relationships break down? Just ask Saturn, where its famous rings are thought to be the remains of satellites that strayed beyond the Roche lobe: pretty to look at, not much good for walking on.

Mini budget sends markets spinning

“Prepare for destined events to take place: endings, revelations, breakthroughs and breakdown,” the New York Post astrologer warned on the eve of the 8 November blood moon.

However, the astrological alarm came more than a month too late for UK financial markets as forces unleashed by the government’s disastrous mini budget pushed sovereign bonds (gilts) to the brink of a hitherto unrecognised ‘Roche limit’.

On September 23, then Chancellor of the Exchequer, Kwasi Kwarteng, set out plans for billions of pounds in unfunded tax cats, leading to huge expansion, which caused sharp spikes in UK gilt yields.

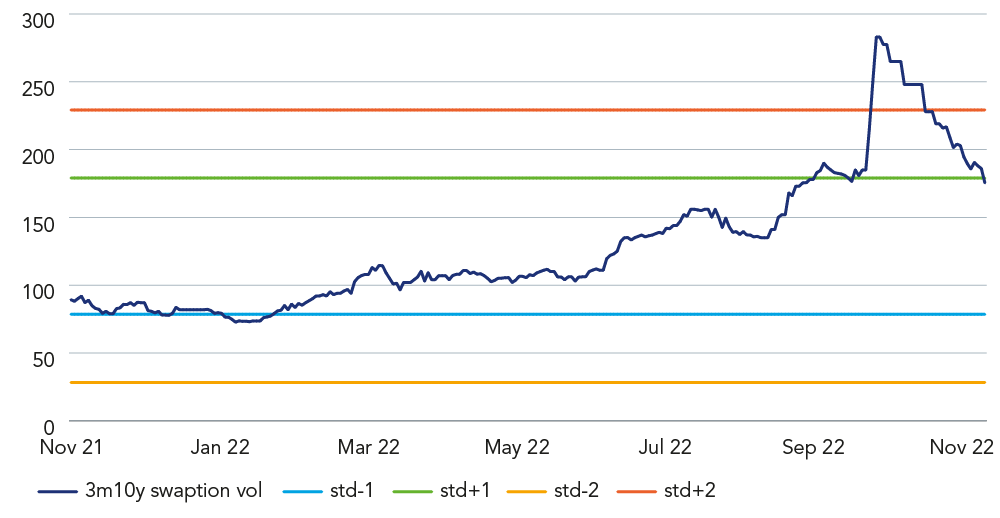

As the chart below shows, early October was an exceptionally volatile period for UK assets.

Figure 2: Gilt volatility (Swaption standard deviations)

This upsurge in turbulence in the gilt markets dragged many defined benefit (DB) pension funds into the maelstrom because a commonly used risk management tool – LDI strategies – compounded the chaos.

Many DB schemes had adopted the so-called liability-driven investment (LDI) strategies as a seemingly secure way to meet funding goals in a process that involves leveraging up bond portfolios via swaps (receiving fixed, paying floating) and repos to hedge the rates component.

At the same time, LDI portfolios typically added beta (through equities, private credit, illiquids etc) to cover deficits.

But when the gilt market entered the danger zone, DB funds suffered a number of indirect consequences, including:

- DB funds that had hedged with swaps were significantly out-of-the-money on those instruments, triggering collateral calls to bolster low cash balances;

- schemes exposed to hedging strategies using levered gilts had to unwind as losses burnt through the asset value – again requiring them to post more capital or sell gilts; and,

- panic selling pushed UK government bond yields higher still, pushing swaps and levered gilts further out-of-the-money, which in turn led to more collateral calls in a doom-loop only forestalled by a Bank of England (BoE) emergency bond-buying intervention.

As the BoE put it: “[…] some liability-driven investment (LDI) funds were creating an amplification mechanism in the long-end of the gilt market through which price falls had the potential to trigger forced selling and thereby become self-reinforcing. Such a self-reinforcing price spiral would have resulted in even more severely disrupted gilt market functioning. And that would in turn have led to an excessive and sudden tightening of financing conditions for households and businesses”.1

In hindsight, the recent gilt crisis bears a strong resemblance to the Covid-crash of March 2020 for its impact on sterling credit markets. UK corporate bond spreads closed the week 20-100 basis points wider in the wake of the LDI dash-for-cash and BoE action.

Various trading desks reported exceptionally high flows. Both volume and enquiry on some days was triple the longer-run average. In a highly irregular move, portfolios were trading the UK currency multiple times during a day at the peak of the crisis.

The UK LDI debacle is yet another example of how leverage can wreak havoc in even the sleepiest corners of the financial system. Notably, LDI-like strategies are common in other parts of the world – and given the old and creaky US sovereign debt infrastructure, the impact of a more direct shock on treasury market liquidity when desperation takes hold is impossible to calculate.

DB Pension Schemes

The UK private pensions market is dominated by defined benefit (DB) schemes – at least for assets under management. Pension scheme data collected by the UK Office for National Statistics counts 10.1 million DB scheme members as at March 2022 with more than £2tn of assets: meanwhile, defined contribution (DC) pension assets stood at just £233bn covering 27.4 million members. Despite having just over one-third of the members in DC schemes, DB scheme members have nearly nine-times the assets.

Obviously, this discrepancy will change over time as nearly half the DB scheme members are already in retirement while ‘active’ members represent just 7% of the total. Very few DB schemes remain open to new members, guaranteeing the market will shrink as the funds mature. By contrast, DC schemes have received a huge boost from the recent auto-enrolment legislation.

DB schemes escape gilt freefall

Rising gilt yields are generally good news for DB pension schemes’ funding positions as liabilities fall faster than assets in such a scenario. All DB scheme liabilities are priced at present value, now much-improved using a higher discount rate, but the impact of falling bond markets on portfolios as interest rates rise is proportionately less as funds only allocate a certain amount to fixed income assets.

Putting aside the LDI fireworks that lit up the UK in the last days of September, the UK DB pension scheme market is actually now in a much better funding position compared to recent history.

Based on the market value of DB scheme assets versus the ‘buyout’ value of the liabilities, the funding ratio has risen from 63% (average for the last 15 years) to 88%, PwC estimates, or to 112%, according to actuarial consultants Lane, Clark & Peacock (LCP). In other words, the DB pension industry is now close to a fully funded position2.

However, this year’s LDI near-death experience will have long-term consequences for the DB sector, such as:

- a greater demand for scheme buyouts. This side of Christmas the ultimate size of the buyout opportunity has most likely shrunk by about £1tn, in line with falling liabilities. Yet experts are predicting a marked pick-up in demand for Bulk Purchase Annuities (BPAs) – where corporates offload pension responsibilities to insurers. Over the next four years, LCP sees demand rising from circa £40bn per annum to more than £50bn. Currently, eight BPA writers ply the UK market.

- reduced demand for LDI products as DB schemes will not need the leverage offered. Already the notional value of the LDI market has slumped from £1.4tn to £1tn with much further to go; and,

- DB scheme de-risking will hit asset managers segregated and pooled pension mandates, especially if insurers do not expand BPA writings.

Re-floated after casting off leverage and adopting revised asset allocation plans, there is some optimism that the UK pension system has escaped the terrible gravitational riptide fate awaiting orbiting astronomical bodies wandering past their respective Roche limits.

The world enjoyed two blood moons this year; the next one is due 14 March, 2025.

Eugene Wigner (1902-1995), Nobel laureate in Physics