Fast reading

- The Fed, the European Central Bank (ECB) and the Bank of England (BoE) all opted to keep rates unchanged this week in their final meetings of the year.

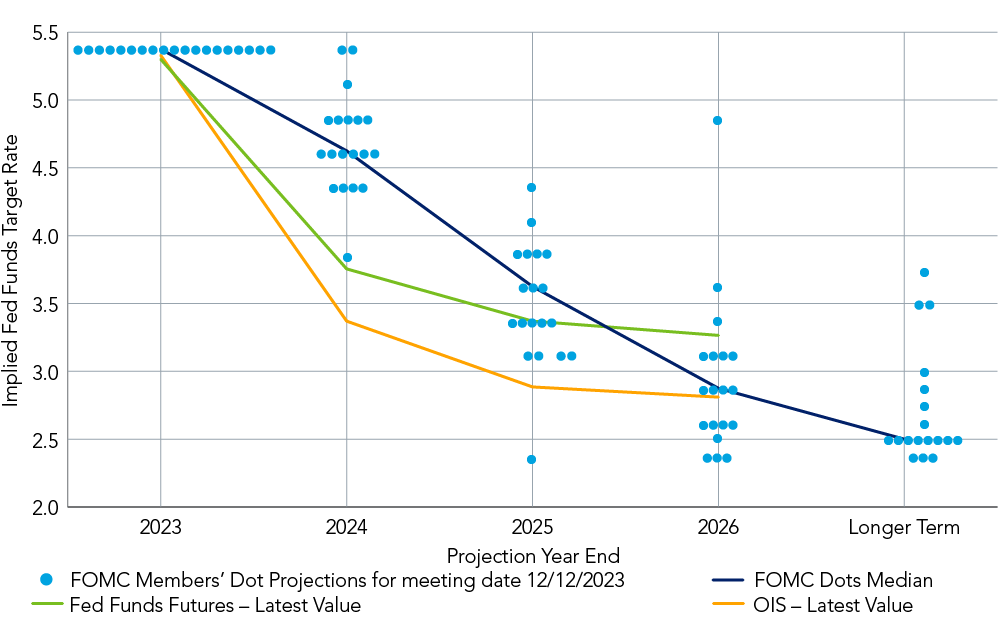

- The latest forecasts from Fed officials suggest 75bps of cuts next year, exceeding previous expectations.

- Officials from the ECB and BoE urged caution in the face of ongoing inflationary pressures. But market’s response suggests significant easing also expected next year.

Equities rallied and bond yields tumbled this week as investors bet that central banks – led by US Federal Reserve – are going to slash rates more aggressively than expected next year.

The Fed, the European Central Bank (ECB) and the Bank of England (BoE) all opted to keep rates unchanged this week in their final meetings of the year.

On Wednesday, Fed chair Jay Powell gave the clearest signals yet that the US central bank’s tightening campaign is over. The federal funds rate stands at 5.25-5.5% – a 22-year high. The latest forecasts from Fed officials suggest 75bps of cuts next year, exceeding previous expectations.

Figure 1: Implied Fed funds target rate

On Thursday, the ECB and BoE also kept rates on hold, although officials from both central banks urged caution in the face of ongoing inflationary pressures.

“The Fed paused for the third consecutive time leaving many investors wondering if three holds signify an end to its rate hiking cycle,” says Mark Sherlock, Head of US Equities at Federated Hermes Limited. US Treasury Secretary Janet Yellen said on Wednesday that she saw a consistent pattern of inflation gradually declining towards target.

“Dis-inflation has moved faster than anticipated, and shows progress towards the Fed’s stated commitments to either reach a 2% inflation target, (or at least visibility to a path back to 2% inflation),” Sherlock says. “We hope for clarification on some of the factors around the FOMC future decision-making framework. Perhaps a timeframe or acknowledgement of additional factors such as the continued easing of financial conditions, evidence of labour-market cooling, as well as the acknowledged inflation trajectory,” he adds.

Figure 1: Implied Fed funds target rate

Europe’s dilemma

In addition to maintaining its benchmark deposit rate at its highest-ever level of 4% for the second consecutive meeting, the ECB also cut its inflation forecasts for 2023 and next year.

The BoE, meanwhile, kept rates steady at 5.25% as BoE Governor Andrew Bailey warned there was “still some way to go” before inflation hit its target.

“The ECB and the BoE stuck to their guns today, maintaining a hawkish tone at their last meetings of the year, and resisting the temptation to follow the Fed on a dovish turn,” says Silvia Dall’Angelo, Senior Economist at Federated Hermes Limited,

“Once again European central banks are slow to react. Two years ago, they delayed their fight against high inflation for too long. Now, they are running the risk of inflicting severe pain of restrictive rates to their already stagnating economies,” Dall’Angelo adds. “Granted inflation concerns have not disappeared, and European central banks do not want to be seen as complacent.”

The UK continues to struggle with sticky core inflation – 5.7% in October – as well as alarmingly elevated wage inflation, as ongoing supply side constraints put pressure on prices. In the eurozone, inflation has recently declined more quickly than expected (down to 2.4% in November from 2.9% in October) but still running above target.

“For Europe, 2024 will provide more clarity on the depth of the economic malaise that many investors expect but has not fully materialised,” says Lewis Grant, Senior Portfolio Manager for Global Equities at Federated Hermes Limited. “As rates reduce – and barring further macro and geopolitical shocks – we anticipate a broadening rally. However, while investor risk appetite has recovered, it remains fragile and we anticipate quality remaining important to investors.”

In Europe, the Europe Stoxx 600 index soared on early trading before closing up 0.87% on Thursday, while the FTSE 100 closed up 1.33%, following a rallies in the US on Wednesday. In bond markets the yield on the two-year US treasury had dipped to 4.3% at 16:30 GMT on Thursday while two-year German Bund yields had fallen to 2.5%1.

For further insights into equities, please see our Q4 2023 SDG Engagement Equity case study