The latest research from the team reveals that:

- Environmental factors have become a statistically meaningful driver of shareholder returns over the past two years

- Avoiding the ESG laggards, and those whose standards are slipping, is a crucial way to capture the ESG premium

- Real Estate and Energy are the exceptions; companies in these sectors with the worst or worsening environmental practices relative to peers tended to outperform

In the 2020 research conducted by the Global Equities team ‘How Covid-19 accelerated the social awakening’, they demonstrated that governance and social factors had a meaningful impact on shareholder returns.

The pandemic cemented the importance of social impact, with more socially responsible companies tending to outperform. Previously there was weak evidence that environmental factors had similar properties, but the historic relationship was volatile and did not reach the necessary hurdle to be considered significant. That has changed over the last two years, with environmental factors supporting performance on a par with social and governance. This confirms that across the environmental, social and governance pillars, the link between ESG and performance is clearly in evidence.

The non-linear shape of ESG

In the team’s inaugural ESG research, published in 2014, they demonstrated a striking aspect of the relationship between governance and shareholder returns, often overlooked in other studies. Namely, the relationship is non-linear. Companies with leading or improving corporate governance scores outperform peers with poor or worsening standards. However rather than performance deriving from the leaders outperforming, the governance premium is largely driven by the underperformance of the laggards. This same pattern exists for the social factor and for the environmental factor.

Lewis Grant, Senior Global Equities PM, said, “For investors, avoiding the ESG laggards, and those whose standards are slipping, is a crucial way to capture the ESG premium.”

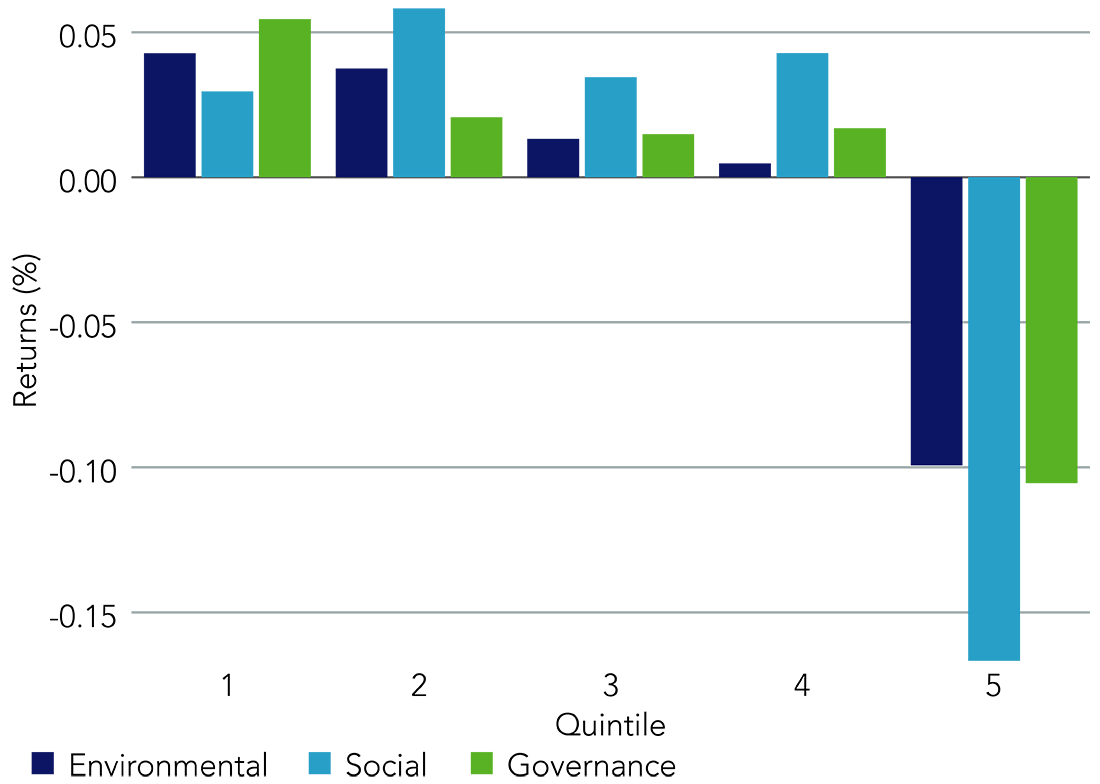

Figure 1. Companies with poor ESG practices have historically underperformed over the long- term

Average monthly total relative returns of companies in each quintile, based on environmental, social and governance scores, from 31 December, 2008, to 30 June, 2022.

Source: MSCI, Federated Hermes, as at 30 June 2022

Figures are calculated using constituents of the MSCI World Index, assuming monthly rebalancing.

A worrying exception

The findings are surprisingly consistent across economic sectors, with the notable exceptions of Real Estate and Energy. Within these sectors, the companies with the worst or worsening environmental practices relative to peers have tended to outperform. For the Energy sector in particular, this result is concerning, if sadly not surprising.

Grant continues, “Some investors simply avoid the entire sector in the name of environmental considerations. Does this exclusion by many sustainable investors result in the sector being more influenced by those less concerned by sustainability? If sustainability-focused investors are not acting as stewards of the Energy sector, it may be asked, who is?”

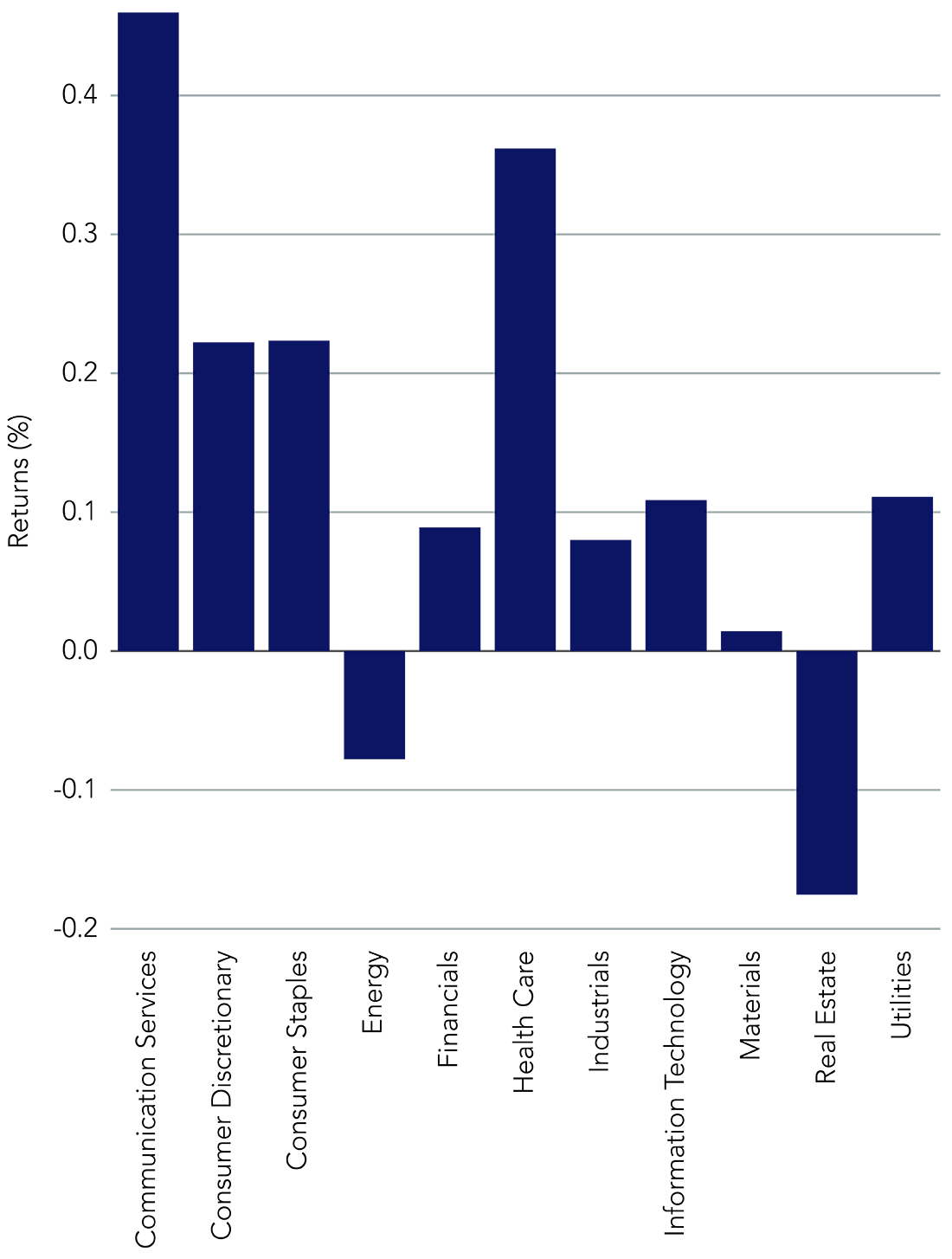

Figure 2. Notable exceptions: Real Estate and Energy break the pattern of ESG outperformance

Average monthly total relative returns of companies in each quintile, based on environmental, social and governance scores, from 31 December, 2008, to 30 June, 2022.

Source: MSCI, Federated Hermes, as at 30 June 2022

Long term thinking

Awareness of sustainability continues to grow across every sector. Embracing sustainability in general is not just about avoiding risks, it is about finding business opportunities.

Grant explains, “We stand by the belief that sustainability requires a long-term focus and can deliver the opportunity for long-term results. In the developing environment, we believe businesses with the right longer-term focus will be the ones who thrive.”