Fast reading

- Q2 2024 results revealed a slowing demand for cars, especially in Europe and China, because of elevated interest rates and a soft economic environment.

- Automotive suppliers are more negatively impacted compared to their original equipment manufacturer (OEM) customers.

- Protectionist measures in response to the influx of cheap Chinese electric vehicles have created a murky backdrop to producers’ commitment to electrification.

The automotive sector was hit by weak second quarter results in 2024, as previously strong fundamental performance brought to a screeching halt. It led to multiple manufacturers and suppliers revising full-year guidance downwards because of softening market conditions. We have been cautious on the automotive sector since the start of the year in anticipation of higher interest rates and weak economic growth negatively impacting demand. Despite this, we have seen and continue to see opportunities in US automotive names over their European counterparts, the former of which we believe is supported by a more resilient outlook.

Slowing global production

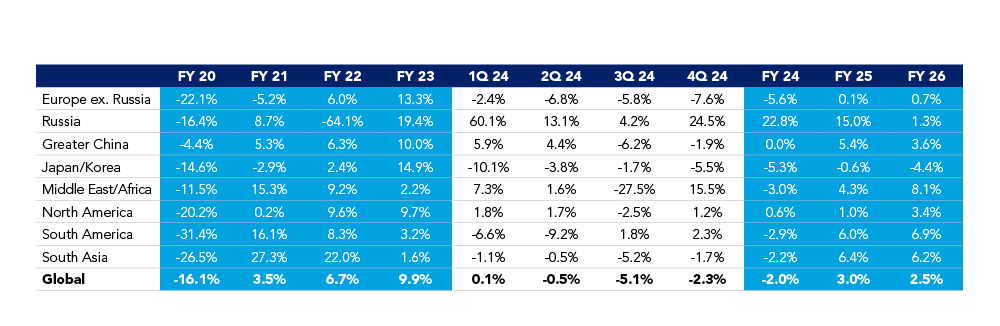

Sluggish economic conditions have caught up to the automotive sector. In July, IHS (S&P Global Mobility) materially revised global light vehicle production forecasts for 2024 downwards, with US growth flatlining but resilient, a weaker outlook for China, and Europe turning even more negative (Figure 1).

Figure 1: IHS July 2024 global production growth rates update

August, September and October revisions saw these trends largely maintained.

Regional divergence

In the US, strong fundamentals came despite higher labour costs from United Auto Workers negotiations last year, higher financing rates, and recent mixed macro indicators. Although 80-90% of all vehicles are financed through credit1 and vehicle lease and loan payments have increased by more than 30% since Q4 20192, Ford and General Motors both surprisingly revised guidance upwards, citing resilient pricing and volumes. This can be attributed to a continued increase in vehicle density in the US3 and lower Chinese exposure.

This contrasts with the situation in Europe, where the majority of European original equipment manufacturer (OEMs) have revised expectations downwards. The higher exposure to weak European and Chinese macroeconomic conditions is impacting European OEMs more than US OEMs. However, OEM balance sheets are in good shape, with a number of OEMs under our coverage receiving positive ratings actions this year, and none receiving negative actions.

Supplier woes

Auto supplier margins are more susceptible to compression than their OEM customers due to OEMs passing down price decreases and lower volumes, resulting in less fixed-cost absorption. A large majority of suppliers under coverage reported downwards revisions, with many also seeing negative ratings actions this year.

EVs losing their spark?

Demand for electric vehicles (EVs) is weakening for a myriad of reasons, including higher prices versus internal combustion engine vehicles (ICEs), low ranges, and long charging times. This has consequences for suppliers: EV parts have a higher margin than ICE parts, so a lower percentage of production attributed to EVs negatively impacts overall margins. Many OEMs are struggling to reconcile the higher costs associated with EVs with weakening price points. Europe is ahead in terms of the transition, so it is unsurprising that US names, with lower exposure to EVs, are handling this trend more comfortably.

Protectionism even without Trump

Exported Chinese EVs are also undercutting legacy OEM offerings, further pressurising pricing and market share, and adding to the pain. Subsidies for Chinese manufacturers have encouraged a multitude of new entrants, e.g. Li-Auto, Geely and BYD, to mass-produce EVs at affordable prices. The average Chinese EV is valued at US$13,800, versus US$28,300 in Europe and US$36,600 in North America4.

In June, the EU responded with planned tariffs of up to 38% on Chinese EVs, in a bid to protect domestic production. This is a double-edged sword: the new regulations also impact vehicles produced by European OEMs in China that are exported back into the EU. While we have not yet seen a significant response from China, there is a risk of retaliation, with Germany, the most vocal in opposing such measures, being the most exposed: their OEMs have the highest Chinese exposure amongst its peers in an economy that is already one of the weakest in Europe.

Sluggish economic conditions have caught up to the automotive sector.

On top of this there is the burgeoning friendship between Telsa chief Elon Musk and presidential candidate Donald Trump, which has added a meme-stock-like uncertainty to the outlook of US EV production, the US already introduced tariffs on Chinese EVs in May. Regardless of who wins the upcoming US election, one would expect protectionist measures to continue as China becomes a larger global player.

Spreads unreflective of fundamentals

After a strong Q1, both US dollar-denominated and euro-denominated high yield (HY) autos have underperformed their respective US and EUR HY benchmarks year to date (see Figure 2).

Figure 2: HY auto total returns vs. benchmark

Source: Bloomberg, BAML-ICE H0AU, HW0C and ER00 Indices as of 31 Aug 2024. Past performance is not a reliable indicator of future performance.

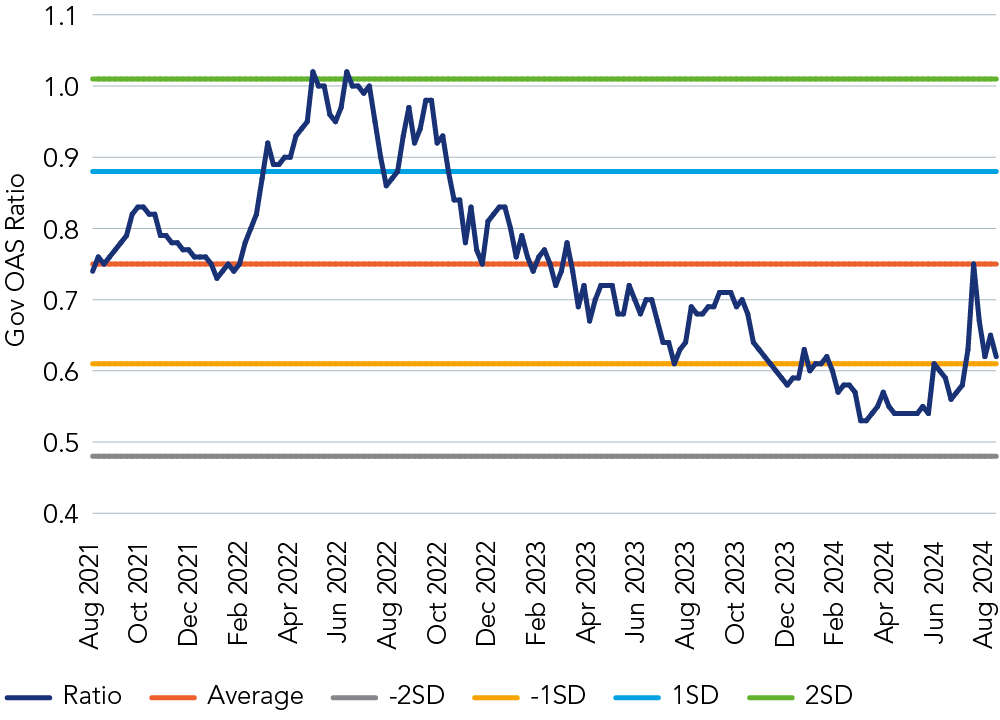

We believe that euro performance is reflective of its regional fundamental outlook, so we have reduced exposure to protect against further shocks in Europe, especially given its relative richness versus euro-denominated HY (see Figure 3).

Figure 3: Historical spread relationship of FHL constructed EUR HY Autos vs. EUR HY (ER00)

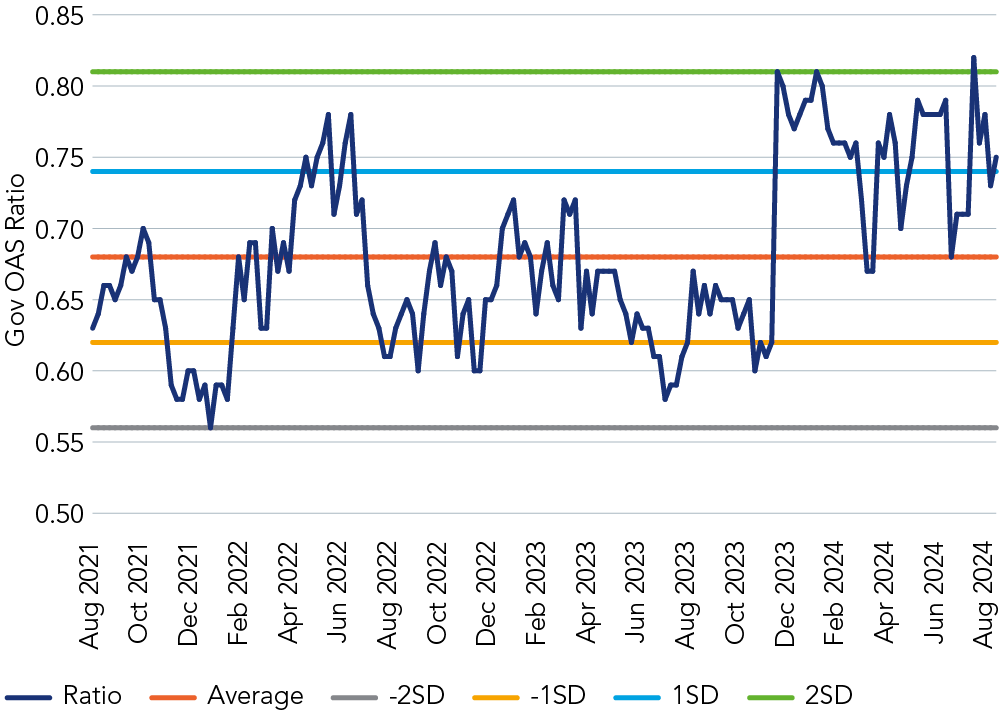

Figure 4: Historical spread relationship of US HY autos (H0AU) vs US HY (HW0C)

We see selective opportunities in the US (see Figure 4), reflecting our divergent regional views, while looking to avoid missing the exit. We remain vigilant on the rapidly evolving trends within the sector.

Find out more about our wider credit offering.

For more insights about fixed income and the US election, click here.

1 Citi: Slide 13, ‘The good, the bad, and the ugly. Autos & Auto Parts – Q4 2023’, Harold Hendrikse, Sanjay Bhagwani, Soumava Banergee, 27 Oct 2023

2 GS Research, ‘The price is right? The case for Tesla to be more selective on US price cuts; analysis on EV pricing and IRA’, Mark Delaney, Will Bryant, Morgan Leung and Aman Gupta, March 2024

3 2024 Vehicle Density Survey, Citi, June 2024

4 ING Research, ‘What EU tariffs on Chinese electric vehicles could mean for the energy transition’, June 2024

BD014806