If 2022 and 2023 were characterised by the market responding in lockstep to the latest messaging from central banks, 2024 promises to be a year where, once more, issuers can be considered on their own merits.

Here, we believe fundamentals have re-asserted themselves. Earnings are softening, leverage levels, defaults and levels of distressed debt are all ticking up – even as interest coverage is beginning to fade.

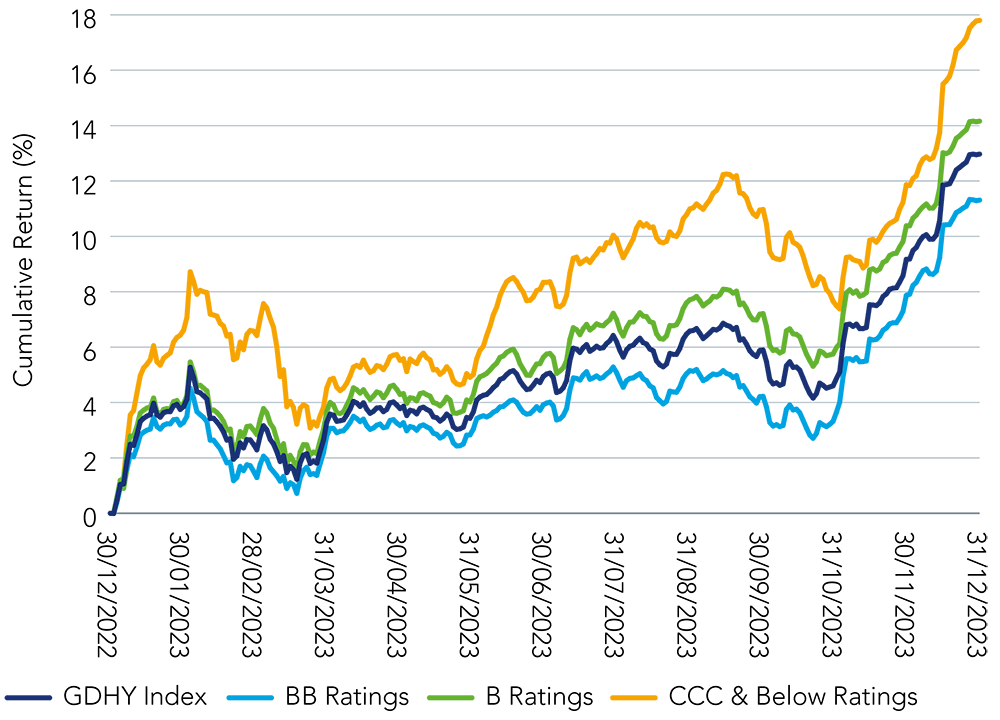

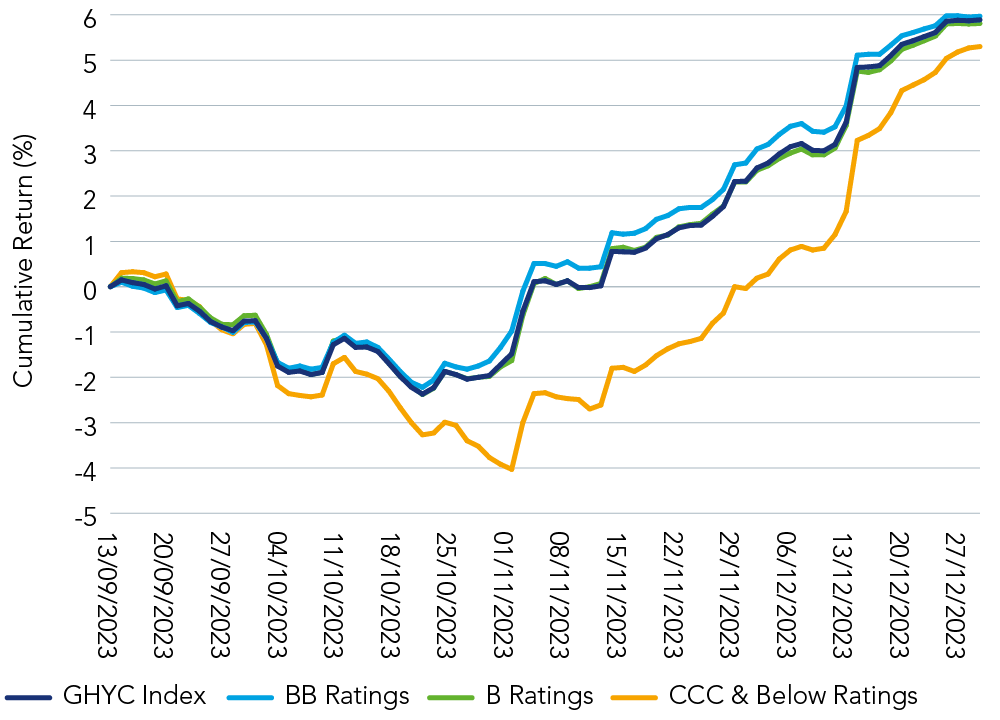

Last year, the lower quality component of the market outperformed due to the absence of the hard landing scenario and limited issuance. This year, we expect a reversal of the ‘trash’ rally and an opportunity for investors to position themselves in the higher quality part of the market.

Investors with the flexibility to position themselves across the credit quality spectrum may be able to take advantage of these trends.