Ludwig van Beethoven was hardly a late-bloomer, laying down his first musical composition at the age of 12.

But it was during the last decade of his life battling deafness and ill health that Beethoven produced some of the finest work in the entire classical music catalogue. Over the 10-year period ending in his death in 1827, the great composer churned out, among other hits: Missa in D (Opus 123); the Ninth Symphony (Opus 125); the last five piano sonata; and, the String Quartet No. 14 in C♯ minor (Opus 131).

Just as Beethoven finished on a crescendo, the influential Swiss mathematician Leonard Euler (1707-83) turned in an incalculable late-life performance. Despite encroaching blindness, Euler – aided by devoted servants and a formidable memory – produced half of his most enduring mathematical insights after 1776.

Euler, of course, is best-known for the famous mathematical ‘identity’ that bears his name. His simple formula condenses five of the fundamental constants with four operations, with eiπ + 1 = 0 often described as ‘the most beautiful’ equation in the maths universe. And the ‘Euler Identity’ combines both rate of change and degree of rotation, which may be a useful tool to quiz bond markets on the turn.

Investors could do well to look to Beethoven and Euler for inspiration on how to thrive amid late-cycle dynamics.

It’s the same old song (but with a different feeling for insurers)

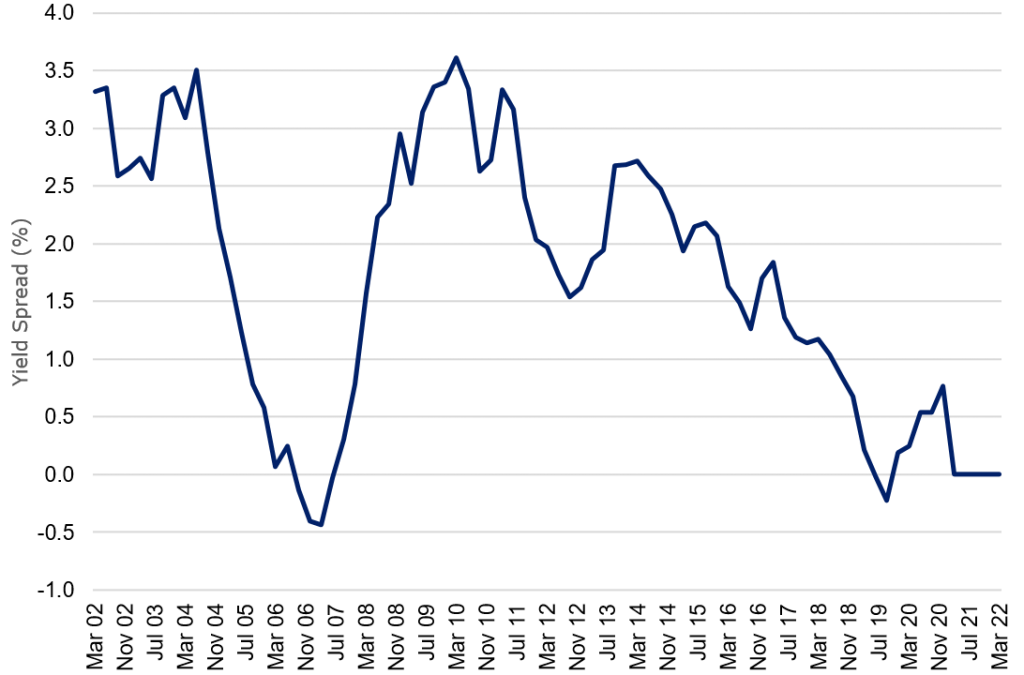

The financial sector has been fighting senility since the global financial crisis (GFC), befuddled by ever-more intrusive regulation and the declining interest rates now diagnosed as ‘financial repression’. As shown below, the infusion of cheap money has been one constant of the post-GFC era.

Figure 1. The impact of ‘cheap money’ on the US yield curve over the last 10 years

Source: Federal Reserve Bank of Cleveland, Yield Curve and Predicted GDP Growth

In the western hemisphere, and according to received wisdom, ageing populations have lowered the ‘equilibrium interest rate’ (or ‘r star’ in economic parlance), which in turn drives even lower interest rates.

And ultra-low rates have an inordinate influence on the financial sector through multiple channels.

For asset-heavy banks (mostly operating in developed markets), the equation follows a simple, logical path: lower rates + flatter yield curve = lower Net Interest Income (NII). NII is usually the largest revenue component for commercial banks.

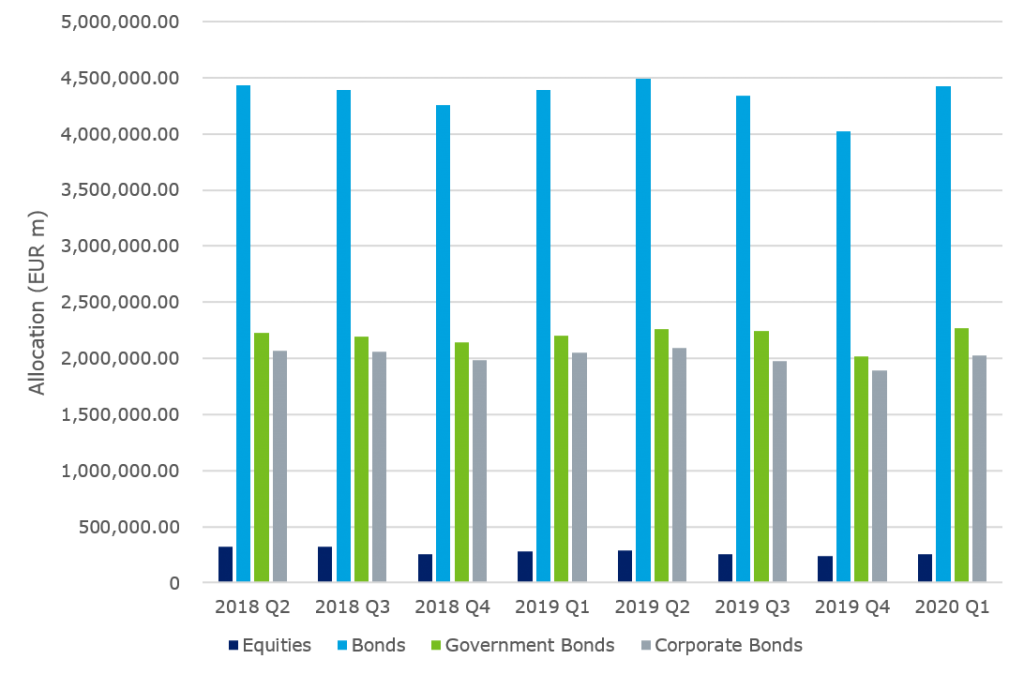

The maths is slightly different for insurers where lower rates, simplistically, equate to reduced investment income. As a rule, insurers pool most of their assets in fixed income securities – principally, sovereign bonds but also credit and (in the US, at least) mortgage-backed securities (MBS). Figure 2, below, shows the aggregate investment allocation of European insurers.

Figure 2. European insurers asset allocation from Q2 2018 – Q1 2020 (€m)

Source: European Insurance and Occupational Pensions Authority, as at Q1 2020.

The super low interest rate environment – and the yields of financial portfolios versus the guaranteed yields of legacy life products – is perhaps the biggest challenge facing insurers at the moment. But not all insurers are equally exposed: we can assess their sensitivity to interest rates across a number of metrics, including:

- the volume, and average rates, of product guarantees;

- the ability to reduce rates; and,

- asset-liability duration mismatches.

The ultralow interest rate environment is possibly the most significant challenges that life insurers are facing. Key determinants of an insurer’s sensitivity are: i) the prevalence of product guarantees, average guaranteed rates, ii) the ability to reduce rates, and iii) asset-liability duration mismatches.

In Europe financial groups have been contending with low rates, even negative since the first Targeted Longer-Term Refinancing Operations (T-LTRO) auction, for US financials this has been another unwelcome side effect of the Coronavirus pandemic.

US banks slow-dance to the low-rate beat

While insurers must deal with particular side-effects of near-zero interest rates, European financial institutions in general have been contending with the issue for some time – coping even as some rates slumped into negative territory in the wake of the TLTRO auctions first tabled by the European Central Bank in 2014.

Last year, US financials experienced some of the pain of their European counterparts as interest rates fell to the zero-bound in response to the Covid-19 outbreak. In the last few weeks, we have seen some pick-up in the risk-free rates but US banks have already been hit by the emergency monetary policies.

As measured by Net Interest Margin (NIM) – perhaps the best way to view bank profitability – the US banking sector has declined significantly over 2020. For instance, data from the Federal Deposit Insurance Corporation (FDIC) shows US bank NIM held at record lows during the second half of 2020.

According to the FDIC figures, the average US bank NIM slid to 2.68% in the third quarter of last year, representing a decline of about 0.6% year-on-year.

At the same time, the broader NII metric fell for a fifth consecutive quarter in the final three months of 2020, dropping by $5.4bn (3.9%) compared to the same period in 2019. The year-on-year NII decreased in spite of US bank funding costs, which also hit record lows. About 43% of US banks reported lower NII in 2020 compared to the previous year, the FDIC data shows.

Changing tunes: investors note long-end yield rise

February 2021 could well mark a new phase in the late-cycle music, with upbeat economic forecasts over-powering the melody of a fading pandemic. Covid-19 cases have eased considerably in most major economies – including a 70% decline from peak pandemic statistics in the US.

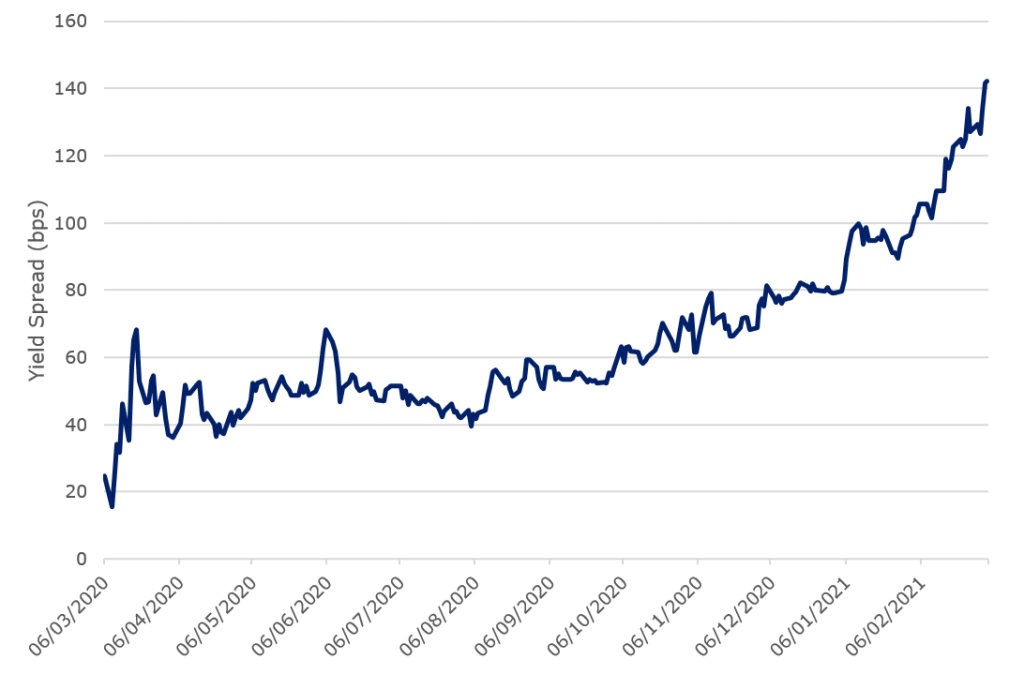

Markets have also factored in a quicker-than-predicted return to normal as vaccination numbers rise, pushing up interest rates at the long-end of the curve. For example, the 10-year US Treasury yields flirted with 1.6% on 4 March, as bond investors reacted to a non-committal stance from US Federal Reserve chair, Jerome Powell, on reining-in long-term rates.

Figure 3. 10-year US yields have increased dramatically since March 2020

Source: Bloomberg data on market matrix US sell 2-year and buy 10-year bond yield spread

In fact, this February saw the fourth-largest increase in 10-year US yields since 2010, as long-end rates rose 0.36% over the month. Markets have now priced-in the non-trivial probability of more than one Fed hike by December 2022 and a 25% likelihood of more than two increases by mid-2023.

Finale: why the last could be best

It’s still unclear whether the early 2021 yield spike signals the final coda of an almost 40-year bond symphony or a brief interlude before the main theme resumes. However, investors are keeping their eyes and ears closely attuned to how the mood shift plays out in various markets. In banking circles, for example, the Additional Tier 1 (ATI) sector has suffered from the recent rate rise, despite limited effective dollar duration and a business model that typically benefits from steeper yield curves – a subject, perhaps, for a future Fiorino.

Right now, financial institutions and fixed income investors could be nearing the end for easy money and ever-declining rates, putting serious pressure on ageing strategies. But as Beethoven and Euler proved, the final years can bring out the best by blending experience with creativity.

Intellect with interest

“Calculemus”

G.W. Leibniz, German philosopher and mathematician.