Countries that score highest on environmental, social and governance (ESG) issues benefit from tighter credit default swap (CDS) spreads than those with lower ESG scores, according to new research from the Credit and Responsibility teams at Hermes Investment Management and the Macroeconomic Research team at Beyond Ratings.

Pricing ESG risk in sovereign credit, examines the relationship between ESG risks in sovereigns and their relative credit spreads. Analysing 5-year CDS spreads and ESG scores from 59 countries during 2009-2018, the research found that:

- Spreads: Countries with the lowest ESG scores have, on average, the widest spreads and countries with the highest ESG scores have the tightest spreads

- Governance: Among the three dimensions of ESG, governance has the strongest relationship with CDS spreads

- Pricing: Utilising the data, the team has created a pricing model for ESG risk in sovereign credit markets

- Ratings: There appears to be a positive correlation between sovereign ESG scores and credit ratings. However, the distribution of ESG scores per credit rating are very wide giving rise to additional risks and externalities which might not be picked up in conventional credit ratings

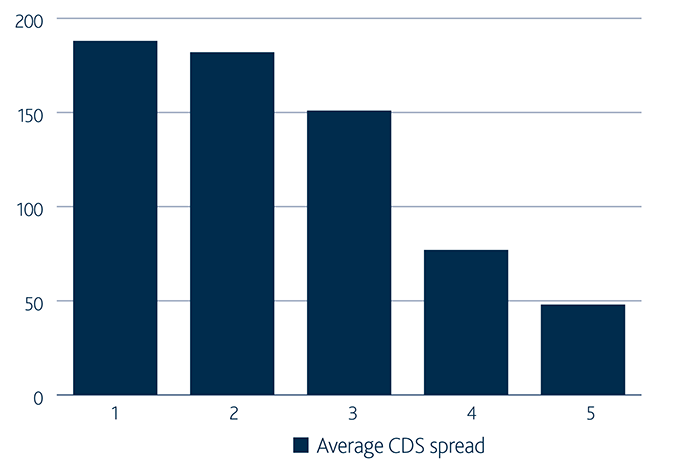

Figure 1 shows the results for the overall ESG score, highlighting the countries with the highest ESG scores tend to have the lowest CDS spreads (quintile 5). Whereas, countries with the lowest ESG scores (quintile 1) tend to have the highest CDS spreads. The difference between these quintiles in terms of basis points is approximately 140bps.

Figure 1: Average CDS spreads by ESG quintile, 2009-2018

1 = lowest ESG score 5 = highest ESG score

Source: Own calculations using data sourced from Beyond Ratings and Bloomberg, as at April 2019

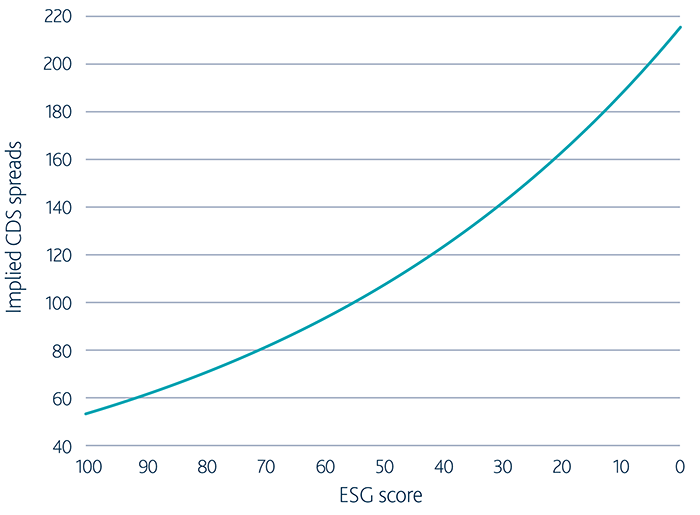

Given the significant relationship we identified between ESG scores and CDS spreads of sovereigns, we derived a sovereign pricing model using a robust quantitative approach over a nine-year period. The study aims to investigate if the above relationship still existed even after controlling for credit ratings, which – in theory – should also take ESG risks into account.

The empirical results indicated a significant negative relation between ESG scores and CDS spreads meaning on average, the higher the ESG score, the lower the CDS spread. Using this analysis, an “implied CDS spread” per ESG score was then calculated and plotted in Figure 2, our pricing chart. The chart clearly implies a strong relationship still stands when controlling credit ratings and quantifies the compensation investors should receive for a given level of ESG risk.

Figure 2: The relationship between implied CDS spreads and ESG scores

Source: Own calculations using data sourced from Beyond Ratings and Bloomberg, as at April 2019

Mitch Reznick, CFA, Head of Credit Research and Sustainable Fixed Income, Hermes Investment Management, said:

“Following on from the research we pioneered on pricing ESG risks in corporate credit, we have now partnered with Beyond Ratings on this ground-breaking study into pricing these risks in sovereign credit, an asset class that remains largely under investigated in relation to ESG considerations. We believe that the integration and pricing of ESG and engagement information into the sovereign investment space will add further precision into the analysis of risk and ultimately make more informed investment decisions.”

Dr. Michael Viehs, Associate Director – ESG Integration, Hermes Investment Management added:

“The research shows that there is a significant relationship between ESG scores and CDS spreads of sovereigns, which enabled us to derive a pricing model for ESG risk in this asset class. This model could be used by investors to identify countries with wide spreads and high ESG score (outperformers) and those with tight spreads and poor ESG performance (underperformers) which might be exposed to more risk than identified by traditional credit ratings. This research will also have implications for investors in other asset classes, such as money market funds and the like who need to assess a sovereign’s ESG risks and exposures.”

Julien Moussavi, Ph.D., Head of Economic Research, Beyond Ratings, added:

“This research, conducted in partnership with Hermes, allowed us to highlight the financial materiality of ESG risks on the sovereign bonds asset class. Beyond trends in some parts of the world, the analysis of the ESG performance of countries that have experienced significant stress periods has led us to understand how the decline of some ESG factors has structurally weakened some economies (Greece, Ukraine, Argentina) and thus brought periods of marked macroeconomic and financial instability leading to defaults for two of them.”

In 2017, Hermes published Pricing ESG risks in credit markets, examining the relationship between a company’s Quantitative ESG (QESG) Score and credit default swaps (CDS).This study was replicated and expanded in 2018 in Pricing ESG risk in credit markets: reinforcing our conviction.