While there is no single ‘right’ approach for extending portfolio duration, there are two basic ways to consider as a starting point. For example, an investor may use a barbell approach, allocating 50% to cash and 50% to an intermediate or long-duration fixed income strategy. Conversely, the investor could choose a single investment offering a shorter or longer duration than that created by the barbell. Theoretically, each strategy could result in a similar aggregate duration. However, depending on how the yield curve changes, the bullet and barbell approaches may experience different relative performance.

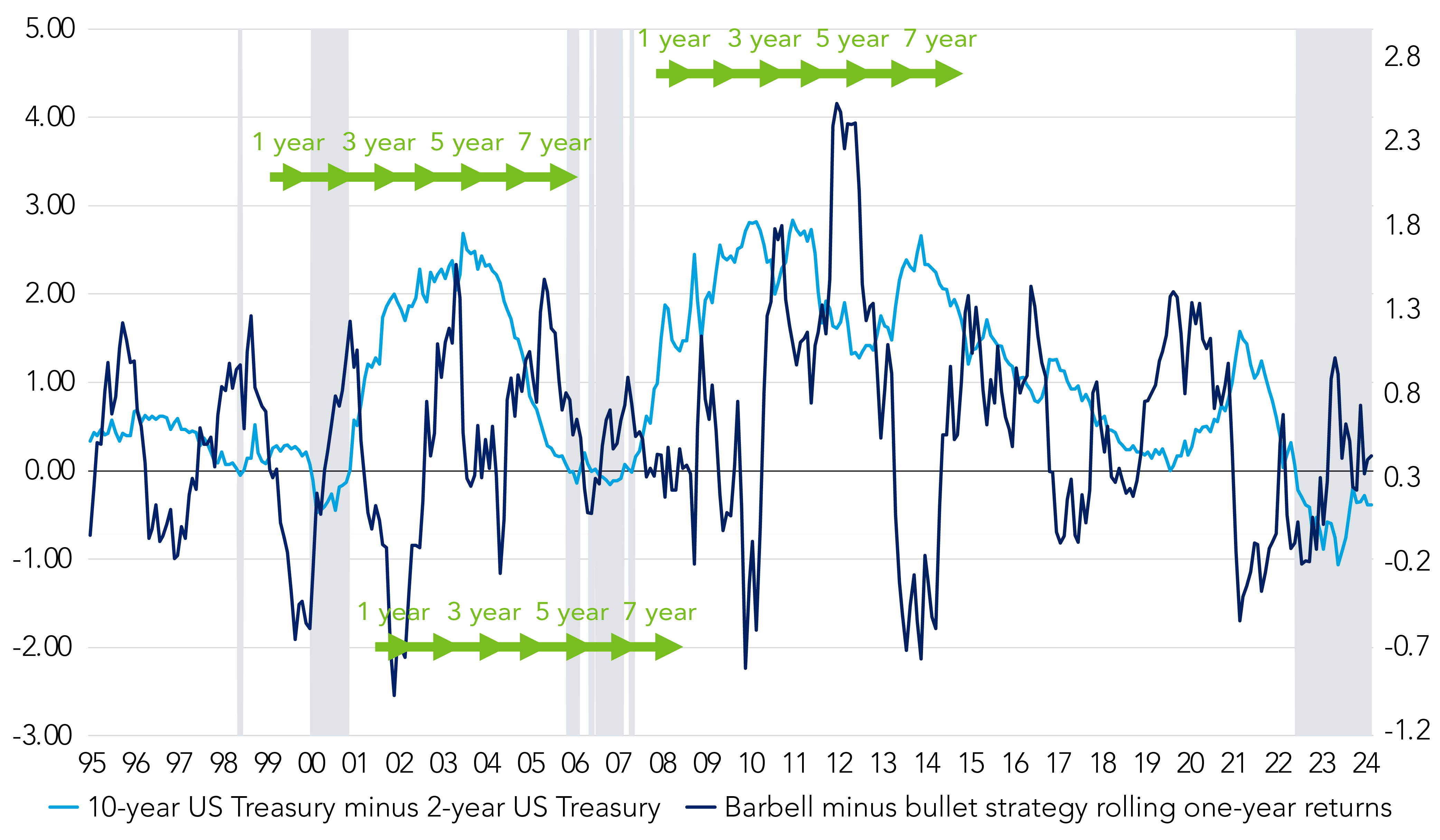

The chart below (Figure 1) shows the 12-month rolling return of a hypothetical barbell strategy (50%/50%) versus a bullet strategy. When the dark blue line is above 0, the barbell strategy outperformed. Shaded regions indicate yield curve inversion, represented by the 10-year US Treasury yield minus the two-year US Treasury yield (the spread) being negative because the two-year yield is higher. The red timeline represents years following a period of yield curve inversion.

Figure 1: Periods of bullet and barbell outperformance vary

Past performance is not a reliable indicator of future results

Figure 1: Periods of bullet and barbell outperformance vary

Past performance is not a reliable indicator of future results

- Rolling returns favoured each approach at different times. The barbell strategy outperformed during inversions, and again two to three years after the yield curve normalized. The bullet strategy outperformed immediately after inversions for a period of one to three years.

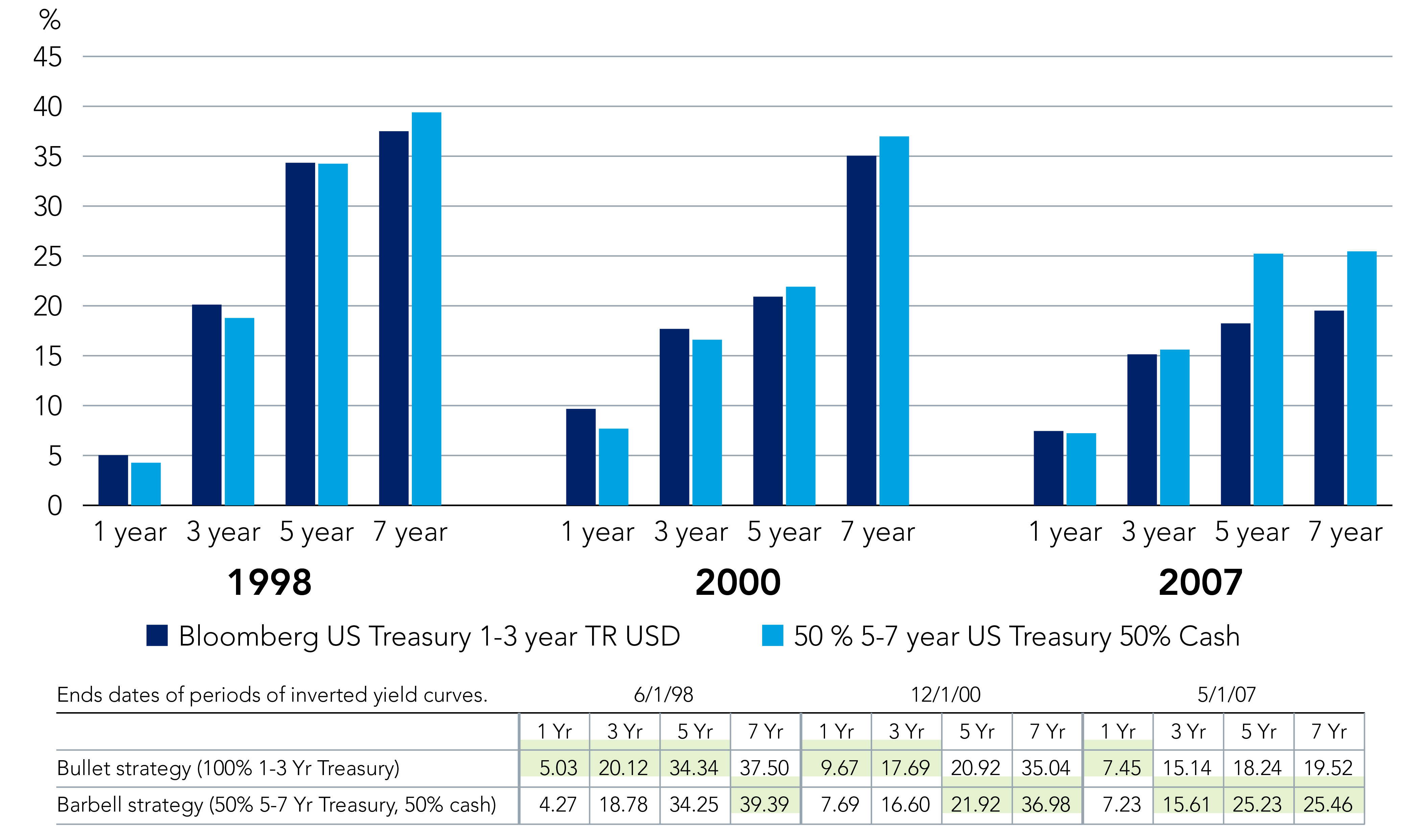

- A comparison of one-, three-, five- and seven-year returns following past inversions showed that the bullet strategy provided higher one- and three-year returns, whereas the barbell strategy provided higher five- and seven-year returns.

- Over the full period (1 January 1995 to 31 March 2024), however, the bullet strategy exhibited less volatility and provided more periods of positive 12-month performance compared to the bullet strategy. The barbell strategy had larger drawdowns.

- Overall, investors may benefit from adding duration to their portfolios, and the mode of adding this duration (bullet or barbell) may differ due to investor preference. Each approach may perform differently as the yield curve normalises again.

- This barbell strategy was also much more volatile than the bullet and had larger drawdowns and more periods of rolling performance in negative territory.

- Viewing this same relationship from a cumulative returns perspective also illustrates that one- and three-year returns following historic inversions were better in the short duration portfolio. Five- and seven-year returns were better in the barbell strategy with exposure to more duration.

Past performance is not a reliable indicator of future results

Bond prices are sensitive to changes in interest rates and a rise in interest rates can cause a decline in their prices.

- Morningstar USTREAST-Bill Auction Ave 3 Mon Index measures the performance of the average investment rate of US T-Bills with the maturity of 3 months.

- Bloomberg Treasury 1-3 Year Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. To be included in the index, securities must have at least one and up to, but not including three years to maturity.

- Bloomberg U.S. Treasury 5-7 Year Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. To be included in the index, securities must have at least five years and up to, but not including, seven years to maturity.