Did you know?

In an election year, what is the average annualised return of the S&P 500 since the administration of Herbert Hoover (1929-1933)?

Answer: 6.2%

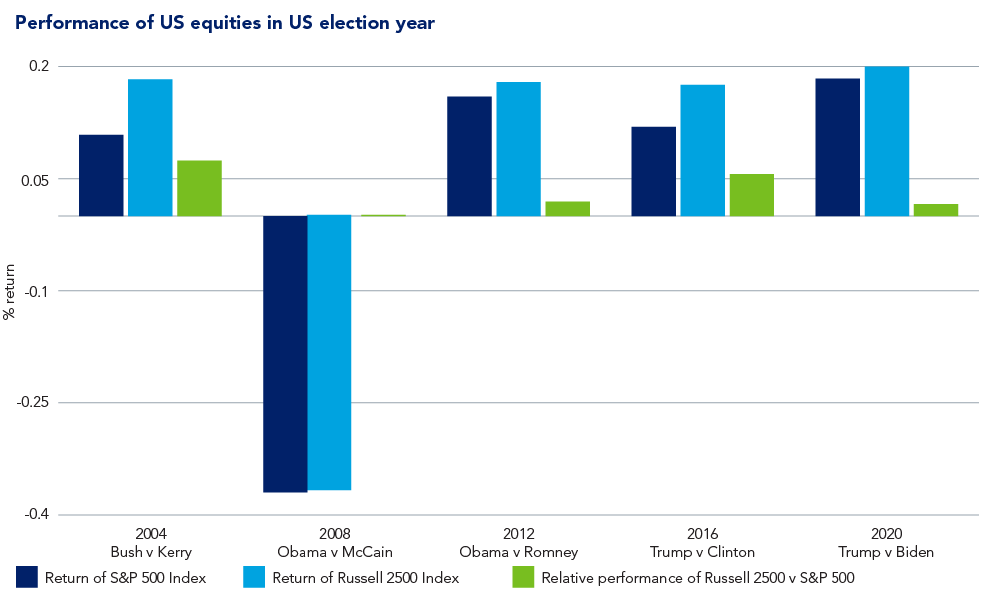

US election years, such as 2024, tend to be good periods for small and mid-cap (SMID) investors as the higher relative domestic exposure of these companies (c.70-80% versus c.50% for the broader S&P) typically benefits performance. Presidential candidates across the political spectrum recognise that a strong economy wins votes and domestic smaller companies – the backbone of the US economy – benefit from this.

The data appears to back this up. Since the Hoover administration, the S&P 500 has delivered an average of 6.2% annualised return in an election year.1 The Russell 2500 doesn’t have data going back to the 1930s, but since its inception in 2003, it has outperformed the S&P 500 in every election year.2

Notable also to the negative is the 2008 election, held in the midst of a significant economic downturn. While the returns from both indices were poor, SMIDs did not meaningfully underperform large-cap stocks. While one datapoint doesn’t make a trend, it is something for those waiting on the sidelines (or hiding in ‘safe’ mega-cap tech, perhaps) to ponder.

Good news for small and mid-cap businesses?

Will 2024 follow this pattern? The Presidential race so far has been fraught. Up until the withdrawal of President Biden in favour of Democrat nominee Harris, most pundits had concluded that a Trump win was all but ensured (and the market had responded accordingly). Since then, however, much has changed. Betting markets now see the outcome as much more finely balanced with either candidate a possible winner and the result ultimately depending on a small number of swing states and a matter of only a few thousand voters. We shall see.

Given this uncertain backdrop, we believe the best way to invest is in high-quality companies with durable competitive advantage and sustainable growth. In our view, these are the stocks that are likely to continue to perform irrespective of who ends up in the White House. This will be the US SMID team’s fourth election cycle and a key lesson in that time is that economics – pardon the pun – always appears to trump politics.

Monetary policy and macro factors

So let’s look at the Federal Reserve: we are anticipating 150bps of further cuts over the coming months (in addition to the recent 50bps cut). This should act as a helpful tailwind to the economy and aid in achieving the much-desired soft landing (we would take a bumpy landing, which we feel may be more realistic..).

On the macro front, inflation appears to be moving in the right direction and cracks in the economy (particularly the lower-end consumer) seem to be contained at this stage. Employment, although patchy in places, remains robust.

The winners of the last few years may not prove to be the biggest winners in the market going forward.

Yet the valuation of SMID cap companies remains subdued, both relative to large caps and their own history as much bad news has been baked into stock prices. We believe this is likely to change over the coming quarters as the ‘broadening-out’ trade, which we witnessed in July, reasserts itself.

Specifically, we would anticipate ongoing profit-taking in the ‘Magnificent Seven’ stocks coupled with reinvestment in a broader section of the market. This, we believe, should reduce the valuation gap (currently c.25%+) from historically high levels. We expect a change in earnings momentum to be the catalyst for this: the winners of the last few years may not prove to be the biggest winners in the market going forward.

Valuations: SMID caps versus S&P 500, 2014-2024

Elections typically generate a lot of noise. Given this, it’s important not to get distracted and remain focused on company fundamentals. As things stand, the economic outlook appears acceptable, rates and inflation are heading down and SMID valuations are at historic lows. This gives us confidence that, as in previous election years, the outlook for US SMID companies is promising. Since the team’s inception in 2009, a focus on high-quality, cash-generative businesses bought at reasonable valuations has ensured attractive long-term returns, whichever party held the White House. There doesn’t seem to be any reason to change that expectation now.

Watch this series of videos to hear more from the US SMID team.

To learn more about US SMID Equity, please also click here.