Debt might be the atom of the financial system; the basic unit that underpins a complex molecular world of banking and commerce.

As quantum-era physics has shown, however, atoms aren’t the end of the story in a yet-be-concluded narrative that has landed, for now, on a short list of suspects deemed as fundamental to the plot.

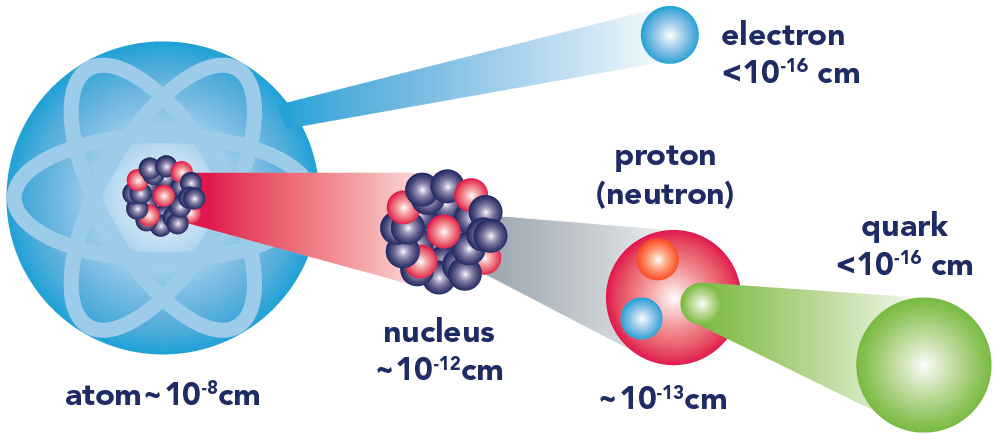

Physicists consider an object ‘elementary’ if there is no evidence it consists of even smaller units – the electron, for instance.

But early 20th century physics unveiled an ever-expanding cast of allegedly ‘elementary’ particles in a series of experiments carried out on new-fangled, high-energy accelerators.

The steady arrival of new particles famously prompted Nobel Prize-winner Isidor Isaac Rabi to query ‘who ordered that?’ when a surprise experimental twist introduced the muon to the mix.

It took the genius of another Nobel laureate, the Yale- and MIT-trained Murray Gell-Mann, to organise the unruly mob of sub-atomic particles into a rational framework based on mathematical symmetry in the mid-1960s.

Under the system that evolved from his earlier ‘Eightfold Way’ model, Gell-Mann classified the then-known strongly-interacting particles – or hadrons – into two groups that explained, among other things, the magnetic properties of protons and neutrons.

The theoretical beauty of the Gell-Mann model, though, required physics to welcome aboard three new, then-undiscovered, elementary particles that he baptised ‘quarks’.

Despite some early critics dismissing quarks as imaginary, accelerator experiments later identified the particles as real components of matter, allowing physicists to focus their understanding of the universe to a scale some eight orders of magnitude smaller than the atom.

Figure 1: The building blocks of the universe

Asset quality: the non-performing nucleus of bank outperformance

Debt at the sub-atomic level has not quite reached the quark-stage but financial sector analysts have identified a range of underlying factors to probe the state of the banking sector at increasingly granular resolution.

And asset quality (AQ) ranks as perhaps the nucleus of the bank-ranking hierarchy, held together by several elementary forces.

In fact, analysts on both side of the Atlantic have cited high bank AQ – as gauged chiefly by the ratio of non-performing loans (NPLs) – to explain the strong performance of financial stocks in recent years.

NPLs remain at cyclical lows in Europe despite another year of relatively high interest rates, giving investors’ confidence that the financial sector still has a sizable loss-absorbing buffer.

The average NPL ratio of eurozone banks held flat at a low 2.4% of loans (Figure 2) over the last 12 months even as interest rates barely budged.

Furthermore, loan quality is generally stable, or even mildly improving, at an already historically strong peak, according to ‘transparency exercise’ data released by the European Banking Authority (EBA) in November 2024. As shown in Figure 2, for the first time, too, no bank supervised by the European Central Bank has reported an NPL ratio of more than 5%; the threshold that triggers tighter regulatory scrutiny.

Figure 2: Banking sector NPLs (by country)

Strong financial forces: a four-factor model

Since the 2008-09 global financial crisis (GFC), the performance of European economies, while not stellar, has at least been supportive of the financial sector.

Nonetheless, the relative strength of banks in the eurozone has still surprised on the upside with four main factors likely driving the outcome, including:

- Resilient economies – the unemployment rate in the region is holding up well and is even going down in some countries, such as southern Europe’s two biggest economies: Italy and Spain.

- Fiscal backstops – many countries offer state guarantees of bank loans.

- Better risk management – post the GFC, in particular, bank internal risk controls have markedly improved.

- Rise of synthetic risk transfer (SRT) – allowing banks offload risk to external parties such as pension funds, has become increasingly common practice in the EU (see breakout box).

The economic struggles of many European nations long after the nominal end of the GFC (2009), with high unemployment in countries such as Spain dragging on economic performance until at least 2014. Spanish unemployment, for example, peaked during that period (hitting 26%) before halving to 13% at the end of 2022 (and falling below 11% by January this year).

Furthermore, governments in Europe utilised a much wider set of tools during the Covid-19 pandemic (compared to GFC-era measures) including furlough programmes that stopped widespread layoffs.

Even the current tepid GDP-growth in the eurozone appears to pose a threat to employment expectations only in specific sectors rather than across-the-board.

Unless unemployment increases significantly, the risk of a consumer debt crisis remains subdued. Any fallout is likely confined to low-income households… and therefore not a major threat to banks.

Not now.

Not yet.

Set against post-GFC readings, the current debt-stress indicators in Europe are hardly flashing a warning.

For example, the Spanish real estate crisis saw NPLs in the country top-out at 14%; including foreclosed property, total non-performing assets (NPAs) in Spain reached a high of about €275bn, equating to a ratio of circa 20%.

Similarly, Italian NPAs soared to a ratio of roughly 17% in 2013 and stayed there until 2016.

Despite the pandemic-driven downturn, NPA levels have continued to decrease as rises in defaults have been kept at bay thanks to moratoria, state-guaranteed loans (and in Spain also a moratorium on insolvencies).

Set against post-GFC readings, the current debt-stress indicators in Europe are hardly flashing a warning.

GACS, cracks and counter-facts

Of course, government support mechanisms can’t completely paper over all the cracks in the financial system.

In Italy, for instance, the government Guarantee on Securitisation of Non-Performing Loan (or GACS) offers a wider variety of workout tools for under-stress banks in the country but it comes with at least one major side-effect: prolonged loan recovery times.

Italian small-to-medium enterprise debt recoveries take, on average, more than six years to complete, double the European level. In a serious downturn, Italian NPA levels could spike higher for longer while prompting banks to dial-up bad loan provisions.

The loan-recovery time-drag explains the structurally higher cost of risk at Italian banks relative to Spanish banks. A reform of the Italian judicial system (including a much-awaited new insolvency code) has long been on various government agendas… sadly without any tangible progress.

Regardless of these niggles, the European ‘AQ miracle’ continues to hold the regional banking system aloft… but for how much longer?

Risk always lurks; the credit cycle never dies

Some immediate challenges are in plain view such as commercial real estate loans and the worsening risk profiles of mid-sized German banks.

Huge flows into fixed income funds might also be masking underlying vulnerabilities such as debt sustainability in the US, UK and several eurozone countries.

Other, less obvious, dangers might threaten the miraculous European AQ ratio including French bank exposure to fair-valued Les Obligations Assimilables du Tresor (OATs) – French government bonds – that sits at a high, if manageable, 10% to 25% of tier 1 capital.

Elsewhere, the return of US protectionism could tip several European economies, including Germany and Italy, into the quicksand of inflation. Higher yields on Japanese government bonds will attract the attention of domestic investors, potentially prompting them to sell off US Treasuries. We could see the financial universe knocked off its axis.

Conclusion

When Murray Gell-Mann conjured up the quark in 1964 he opened up a way to understand the physical world at a much finer level of detail than ever before.

The European banking sector is, arguably, more difficult to model than the inner-workings of the atom but to succeed as portfolio managers we need a similar firm grasp of granular details, a deep understanding of systemic structures and the ability to absorb new ideas.

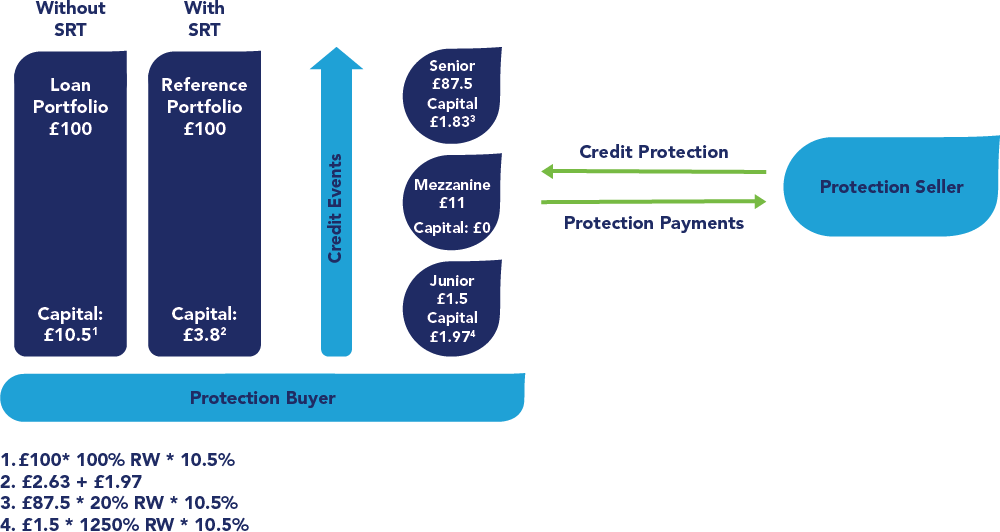

Real synthetics: how SRT changed European banks (and analysts)

Synthetic risk transfer (SRT) allows banks to book capital relief by selling-off significant debt liabilities to external investors including hedge funds, private equity, insurers, pension schemes and sovereign wealth funds.

Introduced with Basel II in 2004, the SRT trade took off in 2017 after the European Banking Authority (EBA) clarified the rules for institutions to claim the capital relief.

Under the revised EBA conditions, banks using SRT vehicles:

- Need to transfer 50% of risk-weighted assets in the mezzanine tranche (see chart below) in a three-tranche securitisation.

- Must transfer of at least 80% of nominal first-loss piece in a two-tranche structure.

- The capital relief must be less than the losses transferred.

Figure 3: How SRT works

Source: IMF

Today, almost every European bank uses SRT. And the trade is currently being exported to the US where the Federal Reserve is warming up to the capital relief concept. Industry sources suggest there is more demand from specialised SRT funds than supply of collateral by the lenders.

Inevitably, the transparency of such risk-transfer deals under pillar 3 disclosure standards will improve over time. Contrary to popular opinion often espoused in the media, the SRT system is a positive development for the banking system – adding another tool for institutions to reduce risks at point of default and free-up capital.

However, the evolution of risk-transfer options also requires analysts and investors to dig deeper into disclosure to better-understand the spilt between organic – or core –bank profitability and SRT-induced capital generation.

Murray Gell-Mann (1929–2019), Physics Nobel Laureate and inventor of quarks.

BD015436