In 2012, the European Organization for Nuclear Research (CERN) particle accelerator finally uncovered proof of a theory advanced almost 60 years previously by Robert Brout, François Englert and Peter Higgs to explain the origin of ‘mass‘1.

After years of planning, and a few technical hiccups, the CERN physics experiment – which saw particles collide at unfathomable speeds – delivered firm evidence that the ‘Higgs Boson’ (the so-called ‘God particle’) was a real entity, despite flickering in the data for only an infinitesimal period of time.

The now proven existence of the Higgs Boson was consistent with the then outlandish theory put forward by the three scientists in 1964 – that an invisible, omnipresent field is responsible for creating all physical mass in the known universe.

Today known as the Brout-Englert-Higgs (BEH) Field, this universal backdrop decides the fate of particles, giving mass to those that interact strongly with it while others (such as the familiar light photon) flow through uninterrupted and weightless.

The discovery of the Higgs Boson was a triumph for 21st century science, plumbing the most in-depth theories of physics with a technological prowess that involved reconstructing obscure processes occurring at a timescale in the order of 10-22 seconds.

But while physicists have been contemplating the mass mystery for decades (if not centuries), observers of the financial world have only recently turned their focus to an increasingly influential background force known as ‘shadow banking’.

Shadow banking – a term first coined by the economist and money manager, Paul McCulley, in 2007 – refers to all financing activities that occur outside the sphere occupied by traditional, regulated banks.

Initially, this new breed of powerful competitors to mainstream banks emerged in the US, where a regulatory grey area allowed institutions beyond the aegis of the Federal Reserve to expand into mainstream financial services.

Taking advantage of the regulatory vacuum, firms such as private equity (PE) funds, insurance companies, private debt providers and specialist consumer lenders rapidly spilled into the shadowy space, gaining an ever-greater share of some core banking business.

To some extent, the asymmetry between the light-touch (or no-touch) shadow banking industry and mainstream regulated banks mirrors the situation exposed in the previous Fiorino – where we explored how the unregulated big tech sector is encroaching into the rule-heavy financial services market.

Shadow banking perhaps represents a more direct threat to the power of mainstream banks, as both sectors operate among related market forces while tech giants such as Google and Facebook enter from different fields.

However, if shadow banking has been like the BEH Field, exerting its influence almost in secret, we are beginning to gather more evidence of its increasing heft. Even before the onset of the Covid-19 era, shadow banks were gaining market share in commercial lending at the expense of the traditional banking sector.

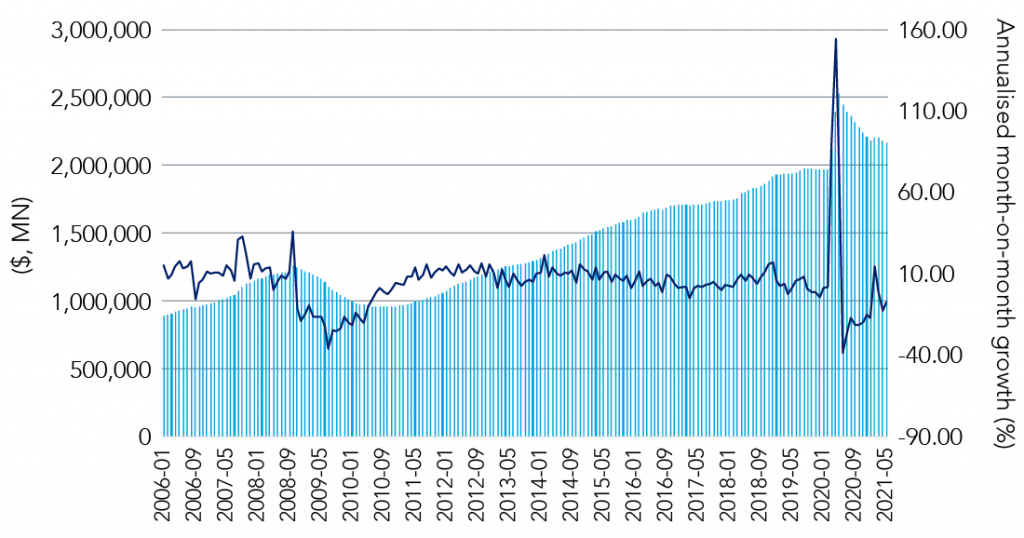

As the graph below illustrates, the commercial and industrial (C&I) loan business is one of the most important lending segments in the US market, making it the primary battleground in the clash between traditional and shadow banking.

Figure 1. Commercial and Industrial (C&I) loan business

Source: Federal Reserve, H.8 Assets and Liabilities of Commercial Banks in the United States for Jun 11, 2021

Another way to find the ‘God particle’ of the shadow banking sector is to examine data sourced from the private equity (PE) industry. For example, a leading PE player, Apollo, publishes a useful classification and outlook for the asset class.

According to Apollo, almost 10% of the outstanding leveraged finance market – essentially, high-yield (HY) bonds and leveraged loans – could migrate to the shadow banking land. As an indicator of what is at stake here, at the time of writing the Corporate, Municipal, Government, Mortgage-Backed and Private Placement loan and bond market (CUSIP) is sailing towards $3tn (up from $2.6tn in January 2020).

Figure 2. Size of the market.

SIze of the market ($, bn) | 2014 | 2019 | 2024E |

|---|---|---|---|

Direct Lending | 200 | 400 | 1,000+ |

Investment Grade (Private placement) | 60 | 100 | 200+ |

Structure Credit | 500 | 1,100 | 2,500 |

Source: Federated Hermes. Based on Apollo November 2019 Investor Presentation

At the same time, factors including regulatory pressures and low interest rates have pushed players such as life insurers and pension funds out of the sunlit (and increasingly desolate) territory of high-grade bonds and into the shadow banking game.

In fact, regulated banks have retained a monopoly in only a few niche subsets of their traditional terrain – such as mortgage warehouse financing or capital calls – as their shadow rivals cast about for further opportunities.

And even Europe is latching on to the shadow banking trend. The continent, which is famously more bank-centric than the US, has recently inked plans for an ambitious Capital Market Union (CMU) under the guidance of the European Commission (EC) that could add to the growing mass of shadow banking in the region.

Specifically, the CMU six-point action plan 2, in the first of its three key objectives, explicitly encouraged non-traditional financing channels:

- Action 4 encourages more long-term and equity financing from institutional investors; and,

- Action 5 directs small-to-medium enterprises (SMEs) to alternative funding providers.

Europe, of course, is not known for speedy actions (and, in this case, we can definitely rule out the timeless ‘spooky action at a distance’ phenomenon first mooted by Einstein for entangled particles).

But, hopefully, we won’t have to wait 50 years to implement the CMU, nor see it disappear in the blink of a Higgs Boson.

G.K. Chesterton

1 For more information, see CERN, ‘The Large Hadron Collider’

2 See European Commission, ‘Capital markets union 2020 action plan: A capital markets union for people and businesses’