Conditions in global credit markets have materially changed over the course of 2022. Tightening policies by central banks to control inflation and investors’ fears of economic slowdown has resulted in a material jump in corporate borrowing costs, a significant reduction in primary issuance and a deterioration in the secondary market.

However, we see a silver lining for creditors in the form of increased leverage during covenant negotiations as issuers look to ‘amend and extend’ existing debt or tackle refinancing in the current environment.

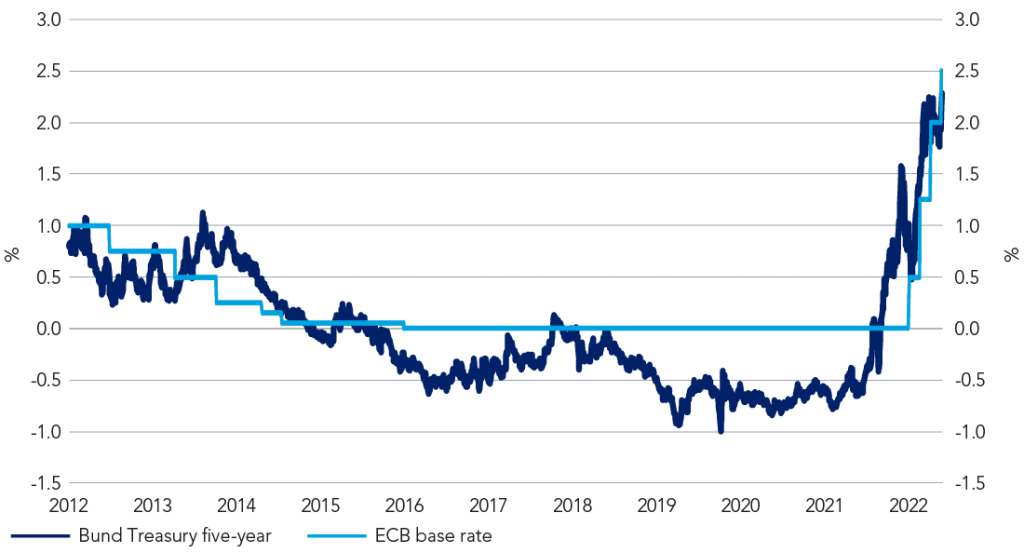

Figure 1: 2022 has seen a sharp increase in borrowing costs

Easy monetary conditions and the rise of covenant-lite funding

In 2022, investors witnessed the end of a decade-long period of rock-bottom government rates and exceptionally cheap corporate financing. This environment created highly liquid credit markets as lenders chased yields and borrowers took advantage by proactively refinancing capital structures. One consequence was a shift in negotiation power, with borrowers leveraging easy access to capital to improve covenant flexibility in their favour. In turn, over the past decade, lenders have seen credit protections weaken in line with declining yields.

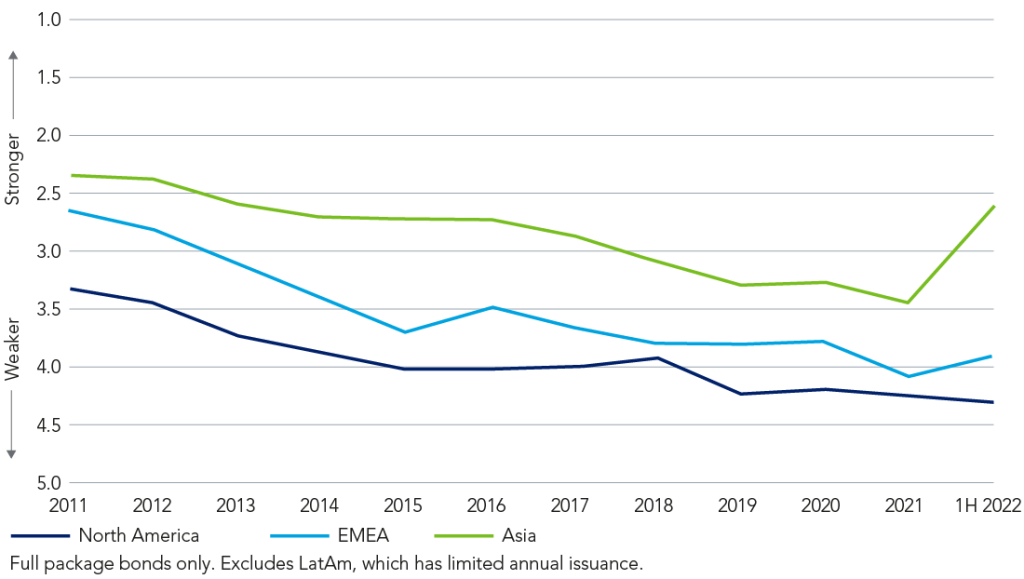

Figure 2: Year-over-year average high yield bond covenant quality score

A shift in negotiating power

Moving into 2023, broad economic, geopolitical and monetary uncertainty, coupled with higher interest rates, makes for a continuation of challenging markets. While corporate borrowers have proactively extended their maturities profiles, some borrowers have near-term refinancing requirements. As such, we anticipate a shift in lender negotiation power, with signs in late 2022 indicating that this shift has already begun. Specifically, we have noticed situations where borrowers which don’t have the luxury of waiting for more favourable financing conditions opting to ‘amend and extend’ existing debt to avoid high-single to double-digit borrowing costs. This has shifted the negotiation in favour of the lender, giving rise to an increase in lender protection.

When it comes to negotiations, certain elements of the debt document are easier for lenders to improve. For example, ‘flex’ provisions1 are often negotiated and include changes to pricing, original issue discount (OID), call protection and most-favoured-nation (MFN) terms2. Other areas of lender focus are historical case studies where lender protection has failed, creating a material loss in value. These include improving the language around provisions such as ‘Chewy’ and ‘J.Crew’ clauses.3

To date, the most prominent example we have witnessed was during a Term Loan ‘amend and extend’ transaction for a US cable operator. Faced with a debt maturity wall that included repayments due in 2024, 2025 & 2026, the borrower opted to support its balance sheet by extending the maturity profile of its term loans. During this transaction, lenders successfully negotiated 11 covenant changes, including provisions related to MFN, the inclusion of ‘J-Crew’ blockers, express ‘Serta’4 and ‘Chewy’5 protection, added restrictions on dividends/share repurchases/repayments of subordinated debt, as well as asset sale proceeds being required to pay down debt.

Strengthening clout of lenders offers a substantial credit-positive development

We recognise that the current environment is unlikely to benefit lenders evenly across credit markets. Higher rated borrowers with stronger balance sheets will face less aggressive negotiations given their ability to absorb increases in borrowing costs. We expect that more lenders will be able to flex their negotiation power with lower-rated, higher-levered issuers, particularly those with limited time horizons. While these lender-favouring conditions won’t last forever, we recognise the importance of the changing dynamics, and support any opportunity to regain some of our creditor protection.

To find out more about our credit offerings, please visit this link.

1 Flex provisions: Provisions designed to give the borrower and the underwriter some flexibility as to the terms of financing.

2 Most-favoured-nation: An agreement whereby the first lender will be entitled to the same or better covenants than the second lender.

3 J.Crew: A controversial provision that used a retail borrower to siphon assets away from secured creditors.

4 Serta: The ability to subordinate senior liens to super senior liens without requiring the consent of each affected lender.

5 Chewy: Such transaction may allow for creation of a non-wholly owned subsidiary of a loan party who is then required by the terms of the credit agreement to be automatically released as a guarantor.