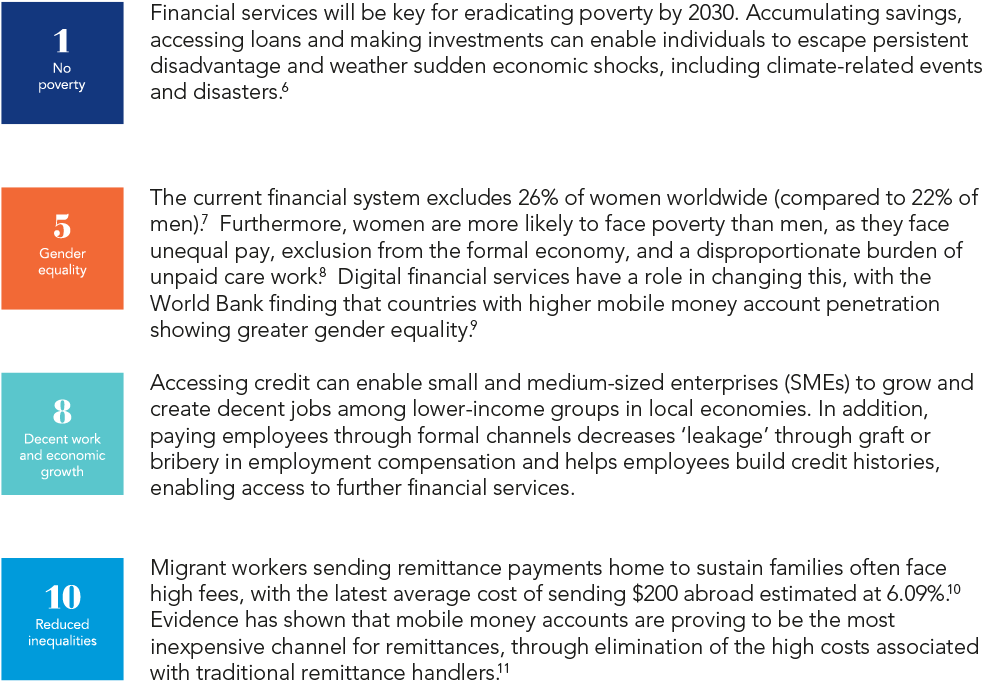

A bank account is a vital means to achieving the outcomes of a broad array of the UN SDGs, acting as a lifeline in times of crisis and a vehicle for social mobility. However, according to data published by World Bank this year, 1.4 billion adults remain excluded from the global financial system today.1

This is often the case for the poorest, most marginalised individuals, due to geographical barriers (for example, lack of access in rural areas), cost barriers faced by banks for issuing smaller loans, and insufficient education among customers in personal budgets and finance.

Impoverished households therefore rely heavily on cash and physical assets, such as livestock, for any financial stability. In the face of crises, such as health emergencies or natural disasters, they lack a buffer to maintain their livelihoods. Likewise, they struggle to access capital which may provide a lever out of poverty by starting a business, taking on education, or moving to access superior employment. This has been exacerbated by the Covid-19 pandemic, which has twisted the knife of poverty and disadvantage faced by cash-dependent households in periods of heightened unemployment, uncertainty, and volatility in basic living costs.

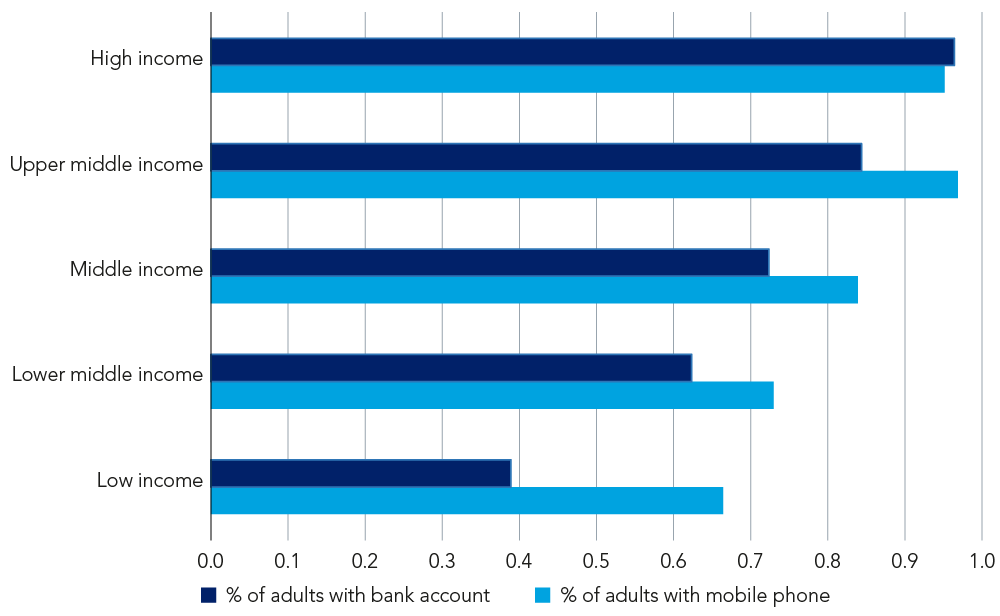

However, it is also true that two thirds of unbanked adults own a mobile phone.2 In many pockets of the world, digital financial services have stepped in to provide resources traditionally offered in brick-and-mortar banks; namely, via digital channels tailored to those with mobile access or potential educational gaps.

Banks rely on telecommunications providers to expand connectivity into underserved areas of the world to better deliver on promises of financial inclusion

A key ingredient is required to mobilise this: a mobile network connection. Banks therefore rely on telecommunications providers to expand connectivity into underserved areas of the world to better deliver on promises of financial inclusion, broadening their reach to more of the 2.3 billion people without internet access in 2021.3

Banks are stepping up their commitments to expand customer bases to underserved groups. In 2021, 28 banks committed to set targets to make credit more accessible, increase financial literacy and combat over-indebtedness through the Principles for Responsible Banking’s Commitment to Financial Health and Inclusion.4 In some cases, telecommunications firms are eliminating the need for a bank entirely by offering their own secure, trusted mobile money services, requiring only a mobile subscription to participate.

Figure 1: Mobile phone vs. bank account ownership, across low-to-high-income countries

Financial inclusion

At Federated Hermes, we recognise the role of financial inclusion as a catalyst for progress on a wide range of SDGs, particularly for vulnerable members of society, and to this end we regularly engage with banks and telecommunications firms to understand how financial inclusion can form a strategic and expansive element of their business strategies. To illustrate this point, we have included some examples below:

Akbank offers digital solutions for small and medium-sized enterprises (SMEs) to access credit and manage finances, and specialised products like its ‘Women-Owned SME Package’. We have engaged with the bank on how it can close skill and technology gaps within SMEs amid the green transition and a challenging economic backdrop and, in future, will focus on how it can measure and target meaningful impact for these clients.

Millicom’s mobile money service, Tigo Money, has reached 5 million users across many largely cash-based economies in Latin and Central America. This includes El Salvador, where 64% of adults do not have a bank account.12

Additionally, its ‘Conectadas’ platform, which aims to educate women and girls on digital and entrepreneurship skills, is an example of the company’s efforts to bridge the digital divide. Our engagement focuses on understanding how the company can leverage its already substantial success to expand services and its customer base.

Click here to find out more about our SDG Engagement High Yield Credit Strategy.

1 ‘The Global Findex Database 2021,’ published by the World Bank in 2022.

2 ‘The Global Findex Database 2017,’ published by the World Bank in 2018.

3 ‘The Global Findex Database 2021,’ published by the World Bank in 2022.

4 ’28 banks collectively accelerate action on universal financial inclusion and health,’ UNEPFI as at 2021.

6 ‘Igniting SDG Progress Through Digital Financial Inclusion,’ published by UNGSA in 2018.

7 ‘The Global Findex Database 2021,’ published by the World Bank in 2022.

8 ‘Why the majority of the world’s poor are women,’ published by Oxfam in 2022.

9 ‘Financial Inclusion: Overview,’ published by the World Bank in 2022.

10 ‘Remittance Prices Worldwide Quarterly,’ published by the World Bank in 2022.

11 ‘Remittance Prices Worldwide Quarterly,’ published by the World Bank in 2022.

12 ‘The Global Findex Database 2021,’ published by the World Bank in 2022.