Complex bank capital structures have created a confusing stack of acronyms for investors in global financials – even before the coronavirus complications – but the Maximum Distributable Amount (MDA) is a key metric to keep an eye on.

The Basel III framework introduced a new concept into the already-crowded lexicon of bank capital jargon. MDA, as implemented in Europe through a raft of directives, sets a limit on a bank’s distributions to investors if its capital level falls into a zone just above the minimum regulatory requirements.

According to the MDA rules, as capital ratios fall deeper into this zone – called the Combined Buffer Requirements (CBR) – banks will face ever-tighter restrictions on their ability to pay distributions via methods including hybrid coupons (both on additional and legacy Tier 1 issues), dividends and bonuses to management teams, too.

However, regulators eased some bank capital restrictions as the coronavirus crisis struck, such as reductions to ‘Pillar 2 Requirements’ (P2R) under Basel III. For instance, the European Central Bank (ECB) has brought forward part of a new directive allowing P2R to be partly covered by Additional Tier 1 (AT1) and Tier 2 capital – to the tune of 19% and 25%, respectively – instead of being fully backed by common equity, or shares, as per current rules.

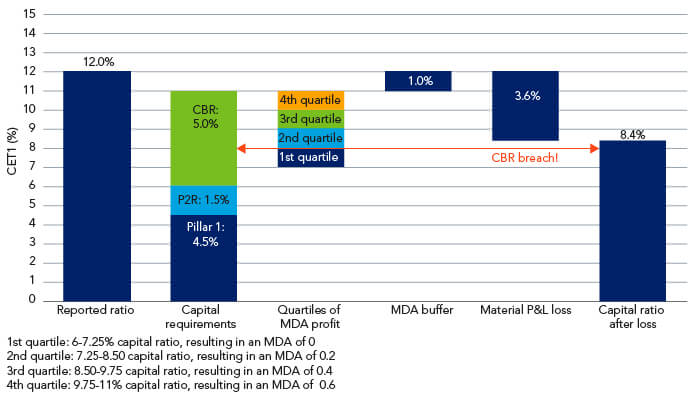

Figure 1. How bank capital stacks up

Source: Federated Hermes as at July 2020. For illustrative purposes only.

Under Basel III, any excess AT1 can spill over into the Tier 2 bucket (but not vice-versa!) in a move that lowers a bank’s Common Equity Tier 1 (CET1) requirements, changing the mix but not the overall capital levels. In theory, and in more normal times, adjusting the capital mix as above can boost return on equity for a bank. However, in pandemic conditions tweaking the mixture frees up bank capital to cover extra lending or rising loan-default provisions.

As at the end of Q1, most European banks reported capital at a lowered CET1 level with a wider gap above the MDA. But if banks have not filled the now-increased AT1 and Tier 2 requirements, the end-quarter capital figures could be overstated because the shortfalls must be covered by equity.

Investors, therefore, need to monitor capital levels above the Tier 1 and Total Capital requirements as well as for CET1. For example, late in Q2 Deutsche Bank printed a $500m Tier 2 capital raise (with a coupon of 5.882%) following a similar €1.25bn issue (with a 5.625% coupon) on May 11.

Deutsche Bank presumably wants to reduce the differential between its CET1 MDA headroom and Total Capital MDA headroom. The $500m Tier 2 issue adds a further 13bps to Deutsche’s Total Capital MDA buffer, increasing it from 192bps to 205bps (compared to a CET1 MDA of 239bp).

Ditto for Commerzbank, which increased its buffer over its MDA total capital ratio from 237bps to 300bps after raising €750m via a Tier 2 issue and €1.25bn in AT1 capital this June.

While this strategy works for banks constrained by the total capital buffer, others, such as Barclays, face challenges on the equity side of the ledger. Institutions in the latter situation can only improve their CET1 MDA buffers by increasing equity.

On 14 July Barclays rushed out a statement before the blackout on new capital guidance for Q2, after it has adopted all the various new capital changes. The bank expects to report an increase in CET1 at the end of Q2 to about 14%, up from about 13.1% at the close of Q1. A further reduction in the MDA hurdle means their coupon buffer rises to 280bps from 160bps – resulting in an increase in its buffer by well over £3bn to almost £9bn at quarter end.

Figure 2. Meeting the MDA: select European banks

Buffers to MDA (bps) | |||

|---|---|---|---|

Q120 | CET1 supervisory review (new) | to CET1 | to total capital |

ABN Amro | 9.62% | 768 | 1120 |

Barclays | 11,50% | 280 | 312 |

RBS | 10% | 659 | 800 |

Deutsche Bank | 10.45 | 238 | 205* |

DNB | 14.61 | 309 | 329 |

BNP Paribas | 9.31% | 269 | 214 |

Commerzbank | 9.65% | 355 | 300** |

Source: company disclosures and Federated Hermes calculations as at July 2020. Note: we have holdings in all issuers named above. *Pro-forma as result of T2 issuance in Q220. **Pro-forma as result of AT1/T2 issuance in Q220.

MDAs and coupon-cancellation risk

Bank capital ratios falling into the MDA buffer zone certainly raise red flags for investors, but the risk is more nuanced than it first appears. The MDA warning light, for example, does not automatically signal coupon cancellations will follow.

In the higher quartiles of the CBR, the MDA distribution framework still allows banks to make good on coupon payments, assuming the institution remains profitable.

Let’s consider a hypothetical bank with a CET1 of 12% consisting of a Tier 1 stack of 1.5% at an average coupon rate of 7%, where distribution to Contingent Convertible (CoCo) bond holders is only 9% of profits. The distribution to CoCo holders is very low compared to the possible 60% if the bank capital remains in the top quartile of the MDA buffer, or 40% in the third quartile, and 20% in the second quartile.

It’s also worth noting that bank management teams are also incentivised to avoid capital buffer-related restrictions, as their bonuses, of course, are linked to MDA levels.