Jason DeVito, CFA

Mohammed Elmi, CFA

Although sovereign and corporate credit spreads are at multi-year tights, we remain constructive on Emerging Market Debt going into 2025. The tight valuations in our opinion are largely justified when one considers how the asset class has successfully navigated the COVID inflationary burst and the resultant prolonged period of tight global monetary policy with minimal defaults.

From a debt, budgetary and external position perspective, a number of core and frontier Emerging Market economies have seen material improvements over the past 12 months. According to Bank of America Merrill Lynch almost three-quarters (73%) of new Emerging Market ratings actions this year moved in a positive direction, compared to the near-total spate of downgrades (93%) witnessed in 2020.

The external macro backdrop in 2025 is also likely to be conducive to Emerging Market Debt: moderating global growth and inflation, coupled with the US Federal Reserve and other major central banks continuing to ease monetary policy, will buttress the attractive Emerging Market yields on offer.

Despite the increased geopolitical risks; an unpredictable new US administration; and anaemic growth in China, we believe a combination of frontier and core Emerging Market names will likely outperform in 2025. Within frontier markets we continue to like Sub-Saharan African credits such as Ivory Coast and Kenya. Underpinned by improving credit profiles and attractive valuations, they also offer investors diversification benefits from potential macro headwinds.

In Latin America, a few darling stories exist. In Argentina, the significant abatement of inflation and a resumption of GDP growth has caught the eye of outside investors. This is occurring against a backdrop of governance and improvements in the regulatory framework. Additionally, El Salvador has seen healthy market access and may benefit as Trump looks to enhance investment into western hemisphere countries that have been strict on narcotics crimes. Furthermore, broadly speaking, any impetus to US economic growth can benefit commodity exporters, many of whom are in Latin America.

Nachu Chockalingam, CFA

Mitch Reznick, CFA

We see three key themes shaping European fixed income markets in 2025: 1) moderate economic growth 2) lower inflation and 3) declining rates. Although these themes are expected to be supportive of credit, how they interact with each other – and with a few ‘known unknowns’- will determine how fixed income markets behave next year.

Although southern Europe appears to be on relatively sound footing, structural reliance on struggling, legacy industries and exposure to China create headwinds for Germany and France. Moreover, with the prospect of further tweaks to the ‘debt brake’ in Germany and a probable increase in defence spending in Europe, we expect deficits to widen.

In a potential divergence play versus the US, the European Central Bank should continue unbridled along its dovish trajectory as core inflation migrates toward the more palatable level of around 2%. The UK is likely heading in a similar direction in both inflation and rates, albeit at a somewhat less certain pace. The combination of widening deficits, which can put pressure on the long end of credit curves, and declining ECB lending rates, which supports the front, mean the yield curve should steepen further.

In the context of spreads that skate close to historic tights, what portends for European credit? Corporate fundamentals are healthy and lower rates are a credit-positive. That said, this is a good opportunity to take advantage of spread compression between low- and high-quality by shifting up in capital structure and quality. It makes sense to earn a little less carry in order to take much less downside risk. Unless China’s coordinated attack on a struggling economy takes effect, the recent struggles of the automotive, chemicals, and steel sectors could continue. Despite a sensational run in subordinated bank capital in 2024, pockets of value remain depending on bond structure. Asset backed securities structures remain robust and are buttressed by the trajectory of lower rates. Well-structured collateralised loan obligations continue to protect investors from being overly vulnerable to the downgrades seen in loans.

The principal unknowns that can throw all of this off track are a deterioration in geopolitics and a shifting US trade policy that proves to be a headwind for economic growth and puts pressure on inflation.

John Sidawi

There is a growing chorus in global markets that US exceptionalism is under threat and that the reign of the US dollar is nearing its final chapter. This is a long book folks, the last few chapters could easily take another five to 10 years and that’s not even a certainty.

Protracted, secular USD weakness is not our base case outcome for 2025 by any degree. For this to occur, seismic economic and sociopolitical forces need to shift for the USD to lose its exceptionalism status and there is simply no evidence of this happening, just vague inferences. A debt-to-GDP US dollar crisis has floated in and out of market narratives for 50 years, but the recent US presidential election outcome breathed new life into this aging thesis.

Ironically, the policies of the upcoming administration are actually USD positive despite verbiage from President-elect Donald Trump for a ‘weaker USD’. Fiscal expansion and tariffs are inherently US dollar positive, with one caveat, that the levy of the tariffs are not egregious.

The roadmap for the USD in 2025 should closely resemble that of its preceding calendar year. Traditionally, global fixed income markets are designed to offer a hedge against general market volatility. However, at the onset of the 2019 global pandemic, and the ensuing surge to inflation, the recalibration of global borrowing costs became the epicentre of macroeconomic volatility. This progression umbilically tied the US dollar to the path of global interest rates more than any other regime that typically drives foreign exchange prices. Much as they did in 2024, global investors will continue to vacillate between a litany of US economic landing scenarios well into 2025. This development should extend the intense correlation between US monetary policy and the USD over other variables that typically lend a hand in determining foreign exchange valuations.

Finally, it is true that the trade weighted dollar is overvalued by a host of long-term metrics, but this was true in 2024, 2023, the year before that, and the year before that….and so forth. However, when placed in context with strong relative growth, an unmatched military, technical innovations, a robust political system, healthy immigration, and superior capital markets…’overvalued’ all of a sudden begins to look reasonable.

Figure 1: US debt to GDP ratio

Robert Ostrowski, CFA

The new Trump administration inherits what has been the strongest developed market economy recently, albeit with some unevenness between manufacturing and services. The soft landing and progress on the inflation front has allowed the Federal Reserve to begin a new easing cycle. But going forward, the election result has the potential to establish a more complicated and longer-term bond-unfriendly environment.

Similar to his first term, President-elect Trump’s tax policy plans seem likely to expand the deficit and fuel federal borrowing further, the previewed immigration policy could have an inflationary impact, particularly on the service component.

In the meantime, a combination of a doveish leaning Fed in the short-term and uncertainty about the long-term success of the new administration’s policies should result in further steepening of the US yield curve, as occurred after the 2016 election. This combination of actions may boost short-term inflation before it has fully retreated to the Fed’s target, causing the Fed to eventually ease less than anticipated in the current cycle.

For spread markets, positive growth policies could be good for corporate debt and in fact, the post-election trade has been positive as it has been in the equity market. But unlike in the equity market, animal spirits are not always best for bond risk investors, sometimes resulting in more volatile spread markets. With investment grade (IG) and high yield (HY) spreads already at historically tight levels, that volatility could be mixed for corporate bond returns.

Foreign policy shifts and the more aggressive wielding of tariffs that Trump promises may prove disruptive. Europe and China are already growth challenged and geopolitical conditions remain tense. A sudden geopolitical driven shift to risk-off by investors could quickly reverse the post-election run-up in the dollar, introducing new opportunities in non-US developed as well as emerging markets.

Figure 2: US Corporate Investment Grade Option-Adjusted Spread

Figure 3: US Corporate High Yield Option-Adjusted Spread

Mitch Reznick, CFA

The sustainable fixed income market is, to state the obvious, a subset of the full fixed income market. It is, therefore, governed by the same forces that shape the wider bond market.

During the year-to-date period, the capital markets witnessed an extraordinarily friendly market for fixed income. In broad terms, inflation has been falling globally. This has triggered reductions in central bank lending rates in many jurisdictions. This led to a material steepening in rates curves in the US and in Europe.

Meanwhile, macroeconomic data has generally been credit-supportive. Under these conditions, fixed income markets attracted record issuance of bonds and strong investment flows, providing a strong technical picture for fixed income.

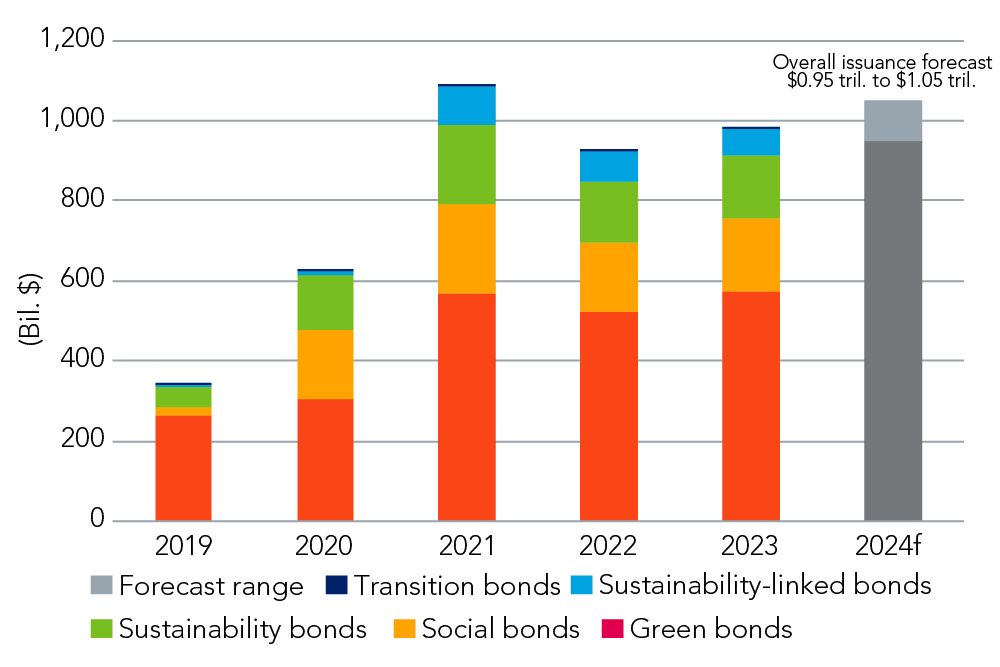

Year-on-year issuance of sustainability-labelled bonds surged and could very well exceed the record year of 2021. Although green bonds, with nearly 60% of issuance year-to-date, have been leading the way, all categories, except sustainability-linked bonds, have grown this year. We could see a total of US$1tn in total 2024 issuance.

Figure 4: Green, social, sustainability, and sustainability-linked bond (GSSSB) market forecast

Turning to investment flows, as at 3Q24, nearly US$40bn, or around 7% of all bond flows reached ESG bond funds, up over 20% versus 2023[1]. In Europe, (the principal market for ESG and sustainability bond funds), nearly 28% of all flows were directed to such funds, which now comprise over 20% of bond funds[2]. In the US, through 3Q24 there was a substantial increase versus 2023 inflows into ESG funds in the US: US$10bn versus US$2bn[3].

The extent to which the momentum for sustainable fixed income carries into 2025 depends on a myriad of forces. However, in many countries across the globe, fiscal policy and regulatory support for sustainability is progressing: corporate disclosure; fund labelling; green bond standards; incentive programmes for EVs, solar, ‘green’ mining, etc; and spending on technologies and innovation. In the US, sustainable bond issuance was never significant, so we don’t believe a new Republican administration will have a material impact on the supply side.

As we look ahead into 2025, while we fully expect the sustainable fixed income market to grow, the real story will be the evolution of the market as it rolls up its growth curve. Constructively, so-called “transition finance” will likely attract companies from the carbon-intensive industries. The health of the planet’s water – oceans and rivers – and the global water cycle will emerge as a specific focus from the wider topic of biodiversity. Judging by the hunt for capital to finance green innovation and technologies, private markets and blended finance will be consolidated around more standardised funding models. Next year is shaping up to be as dynamic as ever.

Further themes that will matter next year:

BD014996