View from the top

Lying at the heart of flexible strategies is the ability to invest throughout the credit spectrum. An unconstrained approach lets investors form a panoramic view of fixed-income markets and only take on risk when particular areas offer attractive risk-adjusted returns. We considered the rising popularity of flexible-credit strategies in the first instalment of our series, and now turn our attention to unconstrained allocation.

Credit markets have developed rapidly over the past two decades as post-financial crisis regulation and the growth of emerging markets have encouraged investors to look at different regions, sectors and instruments. In a fast-changing environment, a top-down allocation process can help credit investors identify new opportunities.

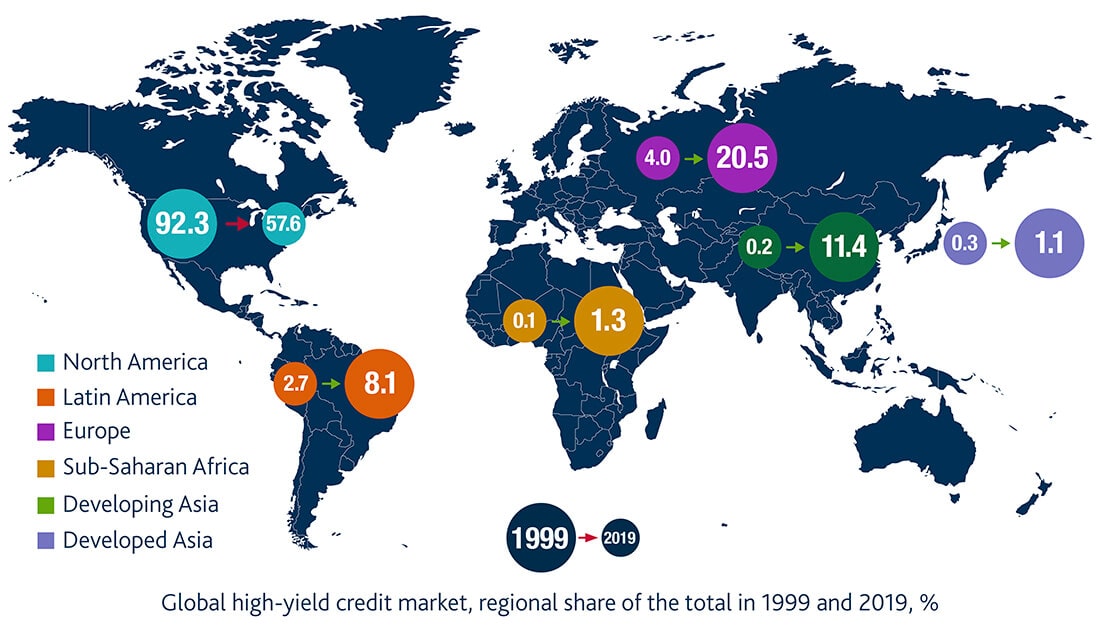

The fixed-income universe has globalised at a particularly impressive pace over the past 20 years (see figure 1). Because markets outside the US have grown, allocating capital to other regions can help optimise a portfolio’s risk-return profile. And as countries exist at different stages of the macroeconomic cycle, a global approach helps investors take uncorrelated positions and capture alpha (we discussed this in more depth in our Spectrum newsletter last year).

Figure 1: A more diverse credit ecosystem

Bond issuance in non-US-dollar currencies has also risen. Boosted in part by the birth of the euro in 1999, the non-dollar part of the market has expanded from less than 5% in the early 2000s to almost 25% in 2018. Flexibility means investing in the most attractive currencies and taking advantage of mispricing through instruments like ‘reverse Yankees’.1

Flexible strategies also invest across different credit classes, from corporate debt with investment-grade and high-yield ratings to loans, asset-backed securities, credit-default swaps and other credit derivatives. Access to a plethora of investment opportunities can help fund managers deliver returns across different markets and interest-rate environments.

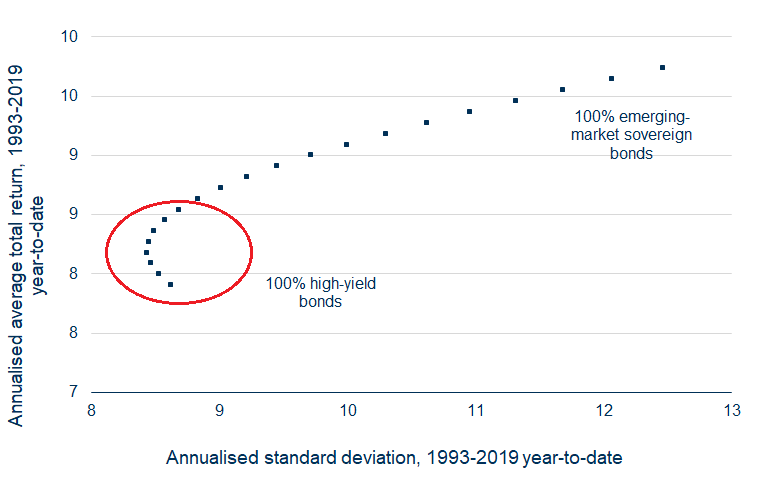

Moreover, adding extra credit classes with different underlying drivers and behaviours can improve the risk-reward profile of portfolios – or the ‘efficient frontier’. Figure 2 shows that by introducing emerging-market sovereign risk into a portfolio of corporate bonds, investors are able to improve its overall potential and deliver attractive returns.

Figure 2: Driving efficiency

But flexible strategies go further than diversifying between credit classes. A truly unconstrained approach invests across the credit curve, sectors, ratings and liquidity profiles. This means that the returns of flexible-credit strategies are therefore driven by a broad range of factors, helping investors diversify their sources of alpha and reduce volatility.

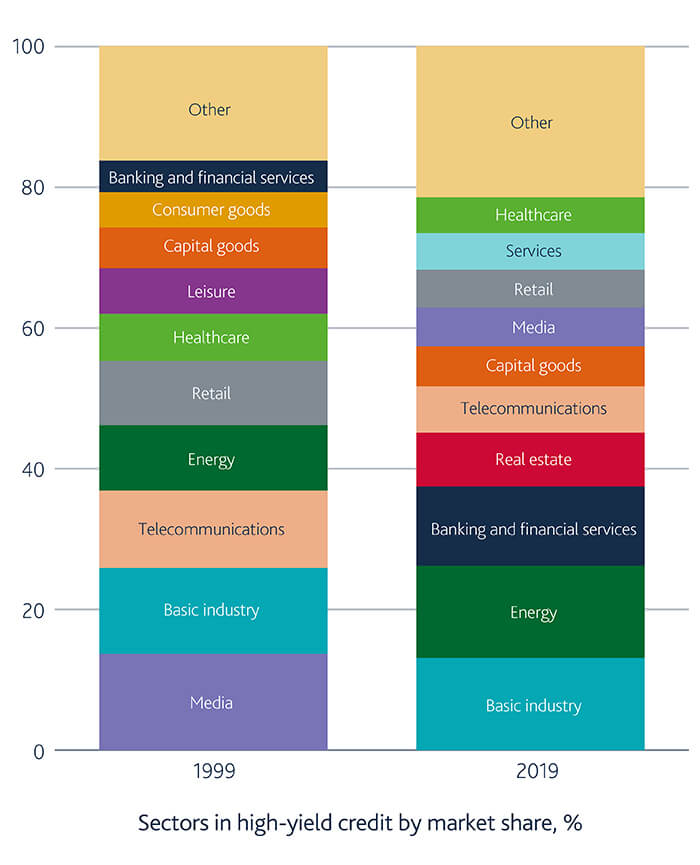

Allocating throughout the credit spectrum also increases investors’ exposure to expanding industries. The share of banking and financial-services issuers in the high-yield universe has more than doubled over the past two decades, as the footprint of media firms – previously the largest sector – has fallen by almost two-thirds (see figure 3).

Figure 3: Shifting trade winds

Regulations brought in after the financial crisis also encouraged companies to issue new types of instruments (see figure 4). ‘Coco bonds’, or AT1 instruments, were first issued in 2014 as a way to make the banking system more robust and able to withstand external shocks. Five years later, the European market is worth more than $200bn. Meanwhile, the market for hybrids – instruments with debt and equity features – has grown to $150bn as investors develop a better understanding of the product.

Figure 4: Instruments in the global high-yield credit market

Instrument | 1999 | 2019 |

|---|---|---|

AT1 | ||

Cash | ||

Junior subordinated | ||

Hybrids | ||

Senior secured | ||

Senior | ||

Subordinated | ||

Tier 1 | ||

Tier 2 | ||

Upper tier 2 |

Source: Bank of America Merrill Lynch, as at September 2019.

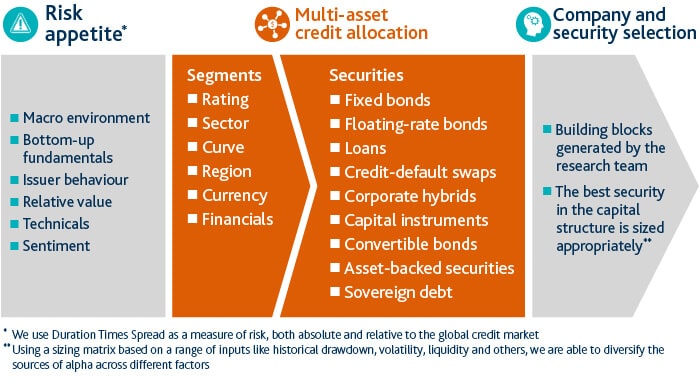

Hermes' approach to allocation

We champion flexible credit investing and determine top-down allocations during our bi-monthly credit-strategy meetings, where we consider a range of factors that drive global markets: the macroeconomic environment, bottom-up credit fundamentals, corporate behaviour, technicals, sentiment, relative value and tail risk. This analysis enables us to determine our risk appetite (see figure 5).

Figure 5: Hermes' credit allocation process

Source: Hermes, as at September 2019.

We then turn our attention to strategic asset allocation across credit markets, considering different regions, ratings, parts of the curve, sectors and currencies. Finally, we set our medium-term asset allocation across credit classes. Once we have defined our allocation strategy, credit selection is driven by high-conviction, bottom-up security analysis (we will focus on this in the third instalment of our flexible-credit series, which will be published next month).

We consider valuations very carefully and if our sentiment indicators show that investors are bullish about a particular segment of the market, we will typically take a contrarian view and reduce its score in our rankings. Our focus on fundamentals rather than prevailing sentiment helps us take advantage of undervalued credits.

Liquidity is also a core consideration. Accessing good liquidity is always important, but even more so at times when it is in short supply – like today. We believe that investing globally throughout large capital structures helps us achieve better portfolio liquidity than constrained strategies are able to secure. For example, our ability to allocate capital to credit derivatives can provide us with extra liquidity during volatile periods.

Our flexibility also allows us to have an up-in-quality, large-cap bias when our risk appetite is low and our strategy defensive. Favouring quality, more-liquid instruments provides us with a good degree of flexibility when we are looking to reallocate capital. Sufficient liquidity also lets us act quickly during periods of volatility – something that paid off at the end of last year.

Q4 2018: navigating storms – flexibly

Storm clouds started to gather in the middle of 2018 as declining macroeconomic indicators and slower earnings growth prompted fixed-income investors to turn their attention to fundamentals.

Fears that the end of the credit cycle was approaching also caused restlessness about the size of the BBB-rated bond market,2 which had risen from $1-$5tn in the decade since the crisis. Concern about the quality of these bonds and speculation that they could become ‘fallen angels’3 prompted a sell-off in credit markets.

At a time when many investors panicked, our flexible allocation process helped us navigate the volatile and illiquid environment. The options overlay that we had in place acted as a powerful hedge during the market sell-off,4 while our conservative allocation to quality bonds earlier on in the year helped us take advantage of decompression in the fourth quarter.

In addition, our focus on large capital structures – combined with our defensive options exposure – allowed us to search global fixed-income markets for instruments whose fundamentals were dislocated.

Hyperlocal weather

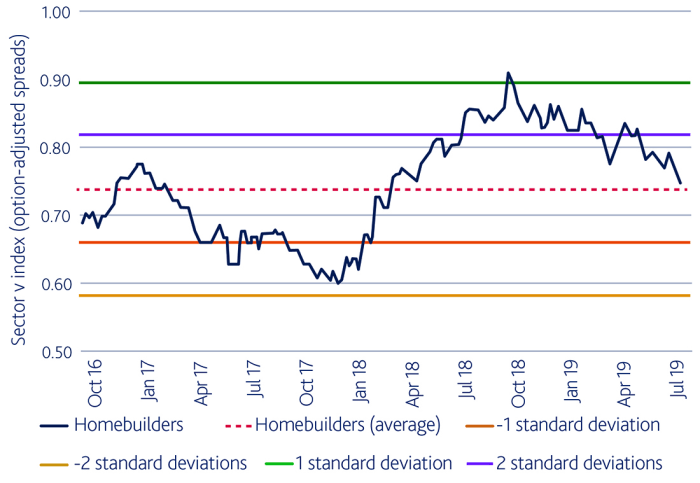

Our analysis of sectors helped us see that the US homebuilders industry was trading two standard deviations cheaper than its three-year average, as investors worried that issuers could default in the face of rising interest rates and slowing growth (see figure 6).

Figure 6: Fundamentals for US housebuilders eventually compressed spreads

Source: Hermes, as at September 2019.

But the market failed to consider how the sector’s fundamentals had improved since the financial crisis. Lower levels of sub-prime lending have resulted in the average borrower having a stronger financial profile, while the focus of companies on option-based land purchases has helped lower risk and possible costs. In addition, significant consolidation in the sector means that the largest issuers are currently in a much better position to weather economic volatility. We saw an opportunity and invested, finding value in issuers with more sustainable corporate structures.

We also noted that falling oil prices had caused the energy-hybrids sector to underperform the credit market as a whole. But we realised that mid-stream energy companies were largely inoculated from declining prices as their earnings tend to be generated by contracts that are based on long-term volumes. We invested in Calgary-based Enbridge and benefited from its strong balance sheet and ability to generate cash at a time when others had reduced exposure to energy issuers.

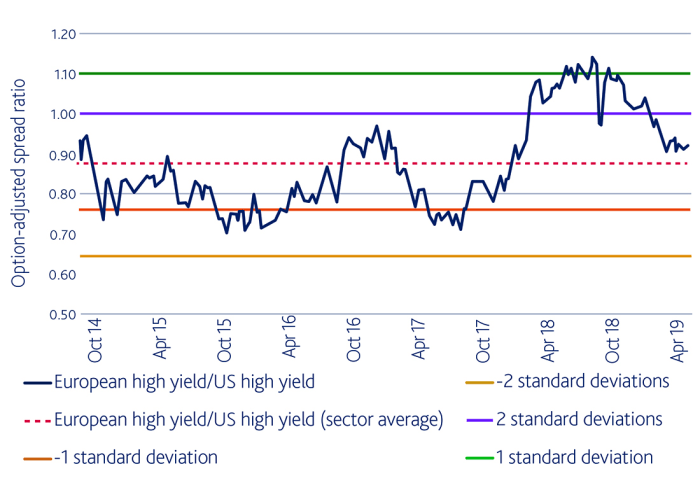

Having the flexibility to invest across different currencies throughout the globe also enabled us to take advantage of dislocated valuations in the European high-yield market (see figure 7). Our unconstrained approach meant we could tap into what we saw as the best way to exploit this opportunity – reverse Yankees.

Figure 7: Thirst for Europe

Source: Hermes, as at September 2019.

Because many European asset managers don’t cover US issuers, and US managers often don’t have the flexibility to invest in euro-denominated debt, it is not uncommon to see reverse Yankees underperform in periods like the end of last year.

In some capital structures, euro bonds were trading with the same level of risk as dollar-denominated bonds, but at twice the spread. Our flexible approach meant we could move quickly to capitalise on this dislocation, which later corrected.

Flexibility helped us navigate volatility at the end of 2018. Going forward, we believe that unconstrained allocation will mean we are better placed to deliver returns in a low-yield world. The global stock of negative-yielding bonds has reached $17tn, while Europe appears to be experiencing ‘Japanification’. In this environment, it is more important than ever for investors to scan the entire credit spectrum for opportunities to generate alpha.

Be prepared for all seasons

The dislocation that we saw at the end of last year emphasised how important it is to invest with flexibility throughout the entire credit spectrum. In a global and rapidly changing market, a flexible approach to credit allocation can help identify undervalued areas and take advantage of opportunities generated as regions, sectors and instruments evolve. This top-down view of global credit markets can then be complemented by bottom-up, high-conviction security selection – which is the focus of the third instalment of this series.

Share:

Risk profile

- Past performance is not a reliable indicator of future results.

- The value of investments and income from them may go down as well as up, and you may not get back the original amount invested.

- Targets cannot be guaranteed.

- It should be noted that any investments overseas may be affected by currency exchange rates.

- This information does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.

- Where the strategy invests in debt instruments (such as bonds) there is a risk that the entity who issues the contract will not be able to repay the debt or to pay the interest on the debt. If this happens then the value of the strategy may vary sharply and may result in loss. The strategy makes extensive use of Financial Derivative Instruments (FDIs), the value of which depends on the performance of an underlying asset. Small changes in the price of that asset may cause larger changes in the value of the FDIs, increasing either potential gain or loss.

1 Euro-denominated debt issued by US companies

2 The lowest tier of investment grade

3 Downgraded to junk status

4 In the fourth instalment of this series, focused on downside-protection strategies, we will explore options strategies in more detail.