Fast reading

- The facility generated a yield above comparable unsecured US dollar Egyptian sovereign bonds of similar tenor – reflecting the strength of the loan’s structure and the essential nature of the underlying commodity.

- The loan benefited from an unconditional and irrevocable guarantee from Egypt’s Ministry of Finance, clearly defined use of proceeds, and comprehensive covenants.

- To fund wheat imports, Egypt’s state buyer borrowed from an A1-rated multilateral development bank, of which Egypt has been a member of since 1974, therefore conferring preferred creditor status on the transaction.

During Ramadan, demand for subsidised bread in Egypt surges as families gather to break their fast. With roughly half of the country’s 120 million population living at or near the poverty line, the Egyptian government’s bread subsidy programme is a cornerstone of the national diet, providing heavily discounted baladi loaves to eligible households.

The scale is vast. The programme produces around 100 billion subsidised loaves a year, requiring approximately 8.5 million metric tonnes of wheat. Domestic production meets only part of that demand – about 3.5 million tonnes – leaving Egypt reliant on imports of roughly 5 million tonnes annually, more than any other country1.

As Ramadan approaches, wheat shipments into Egypt accelerate. Ensuring uninterrupted supply is not merely a logistical challenge but a fiscal one: subsidies weigh heavily on the state budget, even as they help preserve social stability.

Figure 1: Chicago SRW Wheat Futures

Why trade finance matters

Egypt’s state buyer – responsible for importing essential commodities – sources wheat through competitive international tenders. In recent years, volatile global grain prices and a weaker Egyptian pound have increased the cost and complexity of these purchases, reinforcing the importance of trade finance to help facilitate transactions.

To fund imports, Egypt’s state buyer borrows from the A1-rated trade finance arm of a leading multilateral development bank. Egypt has been a member of the development bank since 1974, with no history of payment delays or defaults over this time.

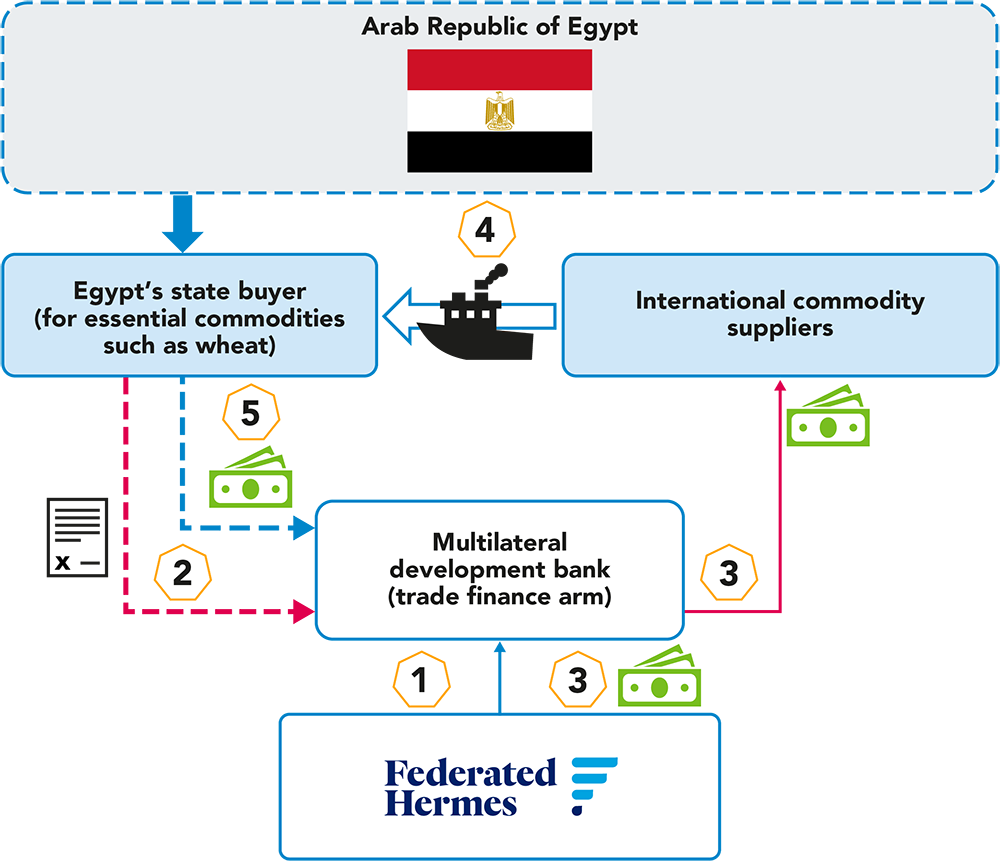

A typical transaction

Ahead of Ramadan last year, Federated Hermes joined a consortium of global banks in providing a US$1.3bn trade finance facility to the development bank’s trade finance arm, to finance wheat purchases for Egypt’s state buyer.

The structure offered lenders robust protection. The loan benefited from an unconditional and irrevocable guarantee from Egypt’s Ministry of Finance, clearly defined use of proceeds, and comprehensive covenants. The development bank paid suppliers directly, while the state buyer committed to repurchase the wheat after 12 months at a mark-up of 12-month SOFR2 plus 4%.

The loan structure offered lenders robust protection.

The financing was secured by title over the commodities during the transportation and supported by sales contracts. Shipments were fully insured, providing an additional layer of downside protection.

The facility generated a yield above comparable unsecured US dollar Egyptian sovereign bonds of similar tenor – reflecting the strength of the legal structure, the preferred creditor status of the development bank’s trade finance arm, and the essential nature of the underlying commodity.

Figure 2: Transaction flow

Source: Federated Hermes

Credit context

Egypt’s credit profile is supported by its large, diversified economy. The country’s nominal Gross Domestic Product (GDP) is approximately US$349bn and it boasts a stable political environment3.

The country’s GDP increased by 4.4% in 20254 and the International Monetary Fund (IMF) provides the North African country with robust support; in February this year the fund allowed Egypt to draw on about US$2.3bn from an earlier approved loan, noting that the country has made progress in restoring economic stability and reducing inflation as part of a reform programme.

The country’s net international reserves exceeded US$50bn in October 20255.

Federated Hermes

Federated Hermes was an early adopter of trade finance as an institutional asset class, launching its Strategy in 2009. The team has worked closely with the multilateral development bank for more than a decade, financing more than US$975m across 68 transactions.

The Strategy provides alternative credit globally, on a highly selective basis, utilising robust financing structures that are of strategic importance to the parties involved.

Our approach focuses on structured, short-term loans secured by underlying assets and off-take contracts. It seeks to maximise the benefits of portfolio diversification and generate higher potential risk-adjusted returns for investors – wherever in the world those opportunities may be.

1 Why Egypt’s price rise on subsidised bread matters | Reuters

2 The secured overnight financing rate (SOFR) is a rate that reflects the cost of borrowing overnight, backed by US Treasury securities in the repo market.

3 President Abdel Fattah el-Sisi has led the country since 2014.

5 Egypt’s net international reserves surpass $50bn for first time in October: CBE – Dailynewsegypt

BD017415