We believe long-term investment in high-quality companies generates excess returns over market cycles and also provides downside protection in adverse conditions.

Portfolio stocks are analysed using fundamental factors in a systematic process.

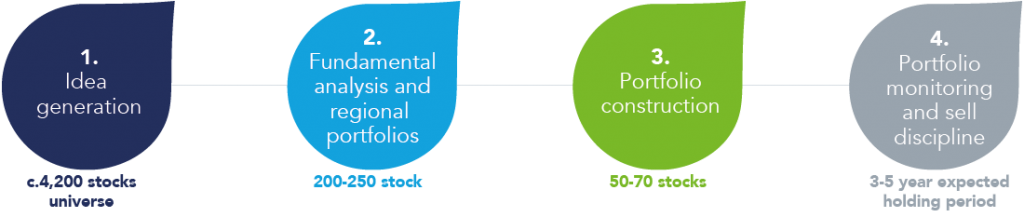

Our usual holding period of three to five years allows us to participate in the secular growth characteristics of many small-cap stocks, and exploit typical market short-termism.

We are an active owner and partner. In practice, this means we maintain a regular dialogue with the companies we own and encourage strong ESG practices.

Federated Hermes Limited has managed regional small cap strategies since 1987.

Hamish Galpin

Head of Smaller Companies

Mark Sherlock, CFA, FCA

Head of US Equities