In the world of ABS issuance, 2022 was an unusual year.

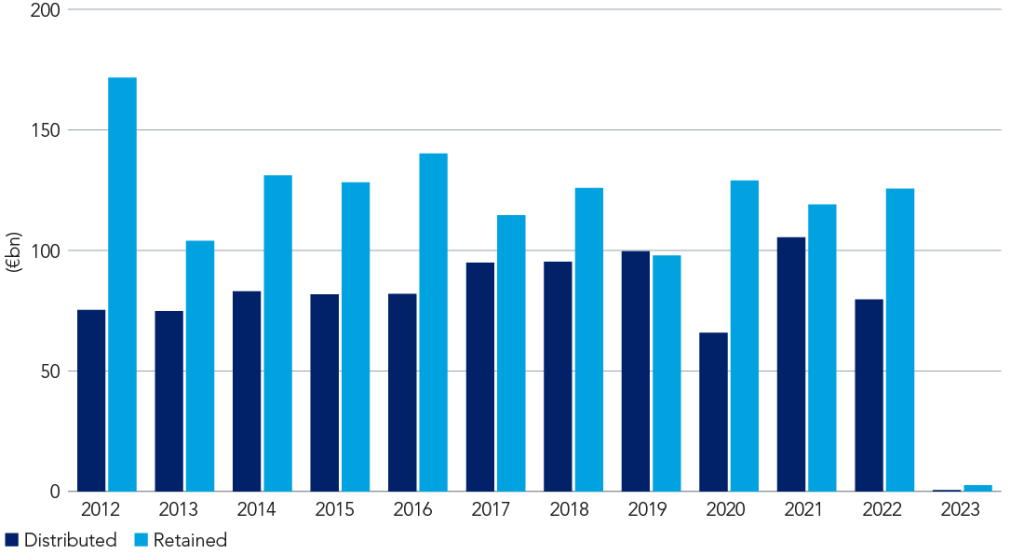

European ABS total issuance volumes

Source: JP Morgan International ABS & CB Research, Federated Hermes Limited as at 31 December 2022. Retained issuance represents securitisations that are not distributed to investors but retained by the originating institutions and typically used as collateral for repo purposes with central banks.

Asset Backed Securities (ABS) had an unusual 2022. Over the 12 months we witnessed the second lowest volume of distributed new issuance in European securitisation (excluding CLOs) in the past decade, second only to Covid-impacted 2020.

Why was this? Well, with the pick-up in returns versus investment grade corporate credit remaining attractive, demand for senior, AAA-rated European ABS was robust and investors – including banks treasuries, asset managers and insurance companies – looked to retain issuance for collateral purposes.

Meanwhile, the selling of structured credit from Liability-Driven Investment (LDI) accounts following the UK’s mini budget in Q3 2022 proved there is significant liquidity in the product with large volumes trading in a short space of time.

According to the Office for National Statistics (ONS), more than 1.4 million UK households are due to roll off the fixed-rate periods of their mortgages resulting in an increase in the rates those borrowers are paying. Despite the expected increase in mortgage delinquencies and defaults, ABS origination processes and securitisation structures have been designed to withstand these kinds of higher interest rate stresses.

Issuance forecasts can be wide of the mark due to the number of moving parts, but the outlook would suggest 2023 issuance will be in line with 2022.