Evidence shows that bonds issued by private companies offer no premium versus those with public equity market capitalization. Historic data coupled with elevated risks highlight why Fraser Lundie, Head of Credit at the international business of Federated Hermes, views this as a mispricing.

In an investment world ever more attuned to responsible investing, one might assume that governance issues such as company ownership would be an area of increasing scrutiny. On the contrary, if valuations are a gauge then credit investors when posed the question “who owns it?” seemingly respond with, “who cares?”.

But they should care – public companies’ financial information tends to be more readily and freely available, whereas private companies often have complex firewalls blocking access to information, reducing transparency for investors, who should in turn be compensated for this. Furthermore, access to homogenous reporting, management commentary and earnings calls provide investors in public companies with a full toolkit to make well informed decisions.

Moreover, real time valuations via stock exchange prices offer investors valuable information for relative value analysis and to gauge market sentiment. Companies with public equity have an additional lever to pull in their capital raising options, something of greater value in times of market stress when debt markets can be more prone to closure. Longer term, public companies tend to be more closely aligned with sustainable long-term growth objectives than private equity sponsors, who are contrarily and frequently driven by a near-term ‘exit’ strategy.

Our analysis finds that market participants show apathy in the absence of premium attached to the bonds issued by companies without public traded equity. High Yield is an area that is traditionally associated with private company debt financing, having rooted itself in US-leveraged buyout boom. Today however, the asset class has evolved dramatically and around two thirds of high yield companies are now publicly owned. It is therefore an optimal universe from which to compare companies of different ownership.

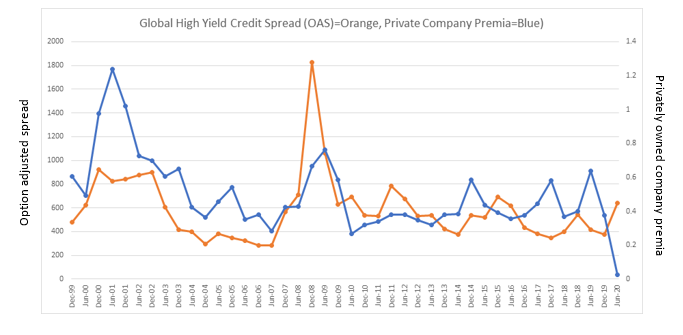

Using data from the Global High Yield universe1 over the past two decades, we compared factors such as bond price, yield and credit spread evolution for public- and privately-owned constituents. In our sample, we found a consistent premium attached to the privately-owned companies over a 20-year period, with elevated levels during periods of crisis, including the 2008 global financial crisis, the Eurozone debt crisis of 2011 and the 2015 US energy crisis. Yet today and even during the deep market stress of March, we found investors are not demanding a premium for the credit of privately-owned companies.

This seems counterintuitive. It would be expected, as in previous crisis situations, that the premium should rise given times of market stress to compensate investors for taking on extra risk, including illiquidity and lighter covenants typically more prevalent in privately-owned companies.

Additionally, private companies are more politically challenging to aid during times of crisis, which can to lead to a higher default risk – demonstrated by recent default rates being much higher in the US than in Europe where state bail outs have been more commonplace. Even when normalising for differences in credit quality and sectors, with private companies typically being lower quality and less cyclical, it remains that no risk premia exists.

We view technical effects as the primary cause of this mispricing with both central bank purchase programmes and passive investors directed by credit ratings but not company ownership status. In particular, the aggressive monetary stimulus in response to the pandemic has caused the market illiquidity premium to drop, as evidenced by bid-offer spreads narrowing and reduced difference between the most recently issued securities and those still outstanding.

This lack of cost presents an opportunity to manage debt-laden companies privately without penalty. A live example being Patrick Drahi, via his holding company, Next Private, offering €2.5bn to buy out minority shareholders of Altice Europe, and delisting the company from the stock exchange. Similarly, in Japan we have seen renewed speculation of take-private of the conglomerate, Softbank, with founder Masayoshi Son eyeing a chance to right the perceived mismatch of their individual holdings’ valuations versus the discount attached to their equity. Crucially, this theory depends on being able to do so without pushing borrowing costs and therefore the cost of capital higher. While this lack of discrimination exists, more deals will surely follow.

This deal flow will help normalise the relationship via the natural equilibrium of supply and demand. Looking further ahead, the real pain in the economy is yet to come. With default rates heightened and worsening recovery rates to creditors in restructurings likely to persist – trends that affect private companies more, with their lower quality and weaker covenants – means that we should expect to see a re-emergence of the long-standing premia attached to privacy.