Downside risks are rising in the current environment

A series of tailwinds that arose in late ’22 and helped the global economy get off to a strong start this year were overwhelmed in mid-March by the failure of two large US regional banks and the collapse of confidence in Credit Suisse. The events led the International Monetary Fund (IMF) to lower its global GDP growth forecast to 2.8% this year from 3.4% in 20221 , with the potential for growth to decelerate further to 2.5% (which would represent the third-slowest outcome since 2001) if stress in the financial sector deepens.

The base case in our London office is still a mild recession in the US in either the back half of this year or early ’24, spilling over to other advanced economies soon after. While March’s banking panic raised odds of a recession down the line, the swift and decisive policy response that followed averted more immediate and significant macroeconomic consequences. That said, recent events have changed the balance of risks to the downside as the banking stress adds to tightening financial conditions already underway due to 14 months of central bank rate hikes.

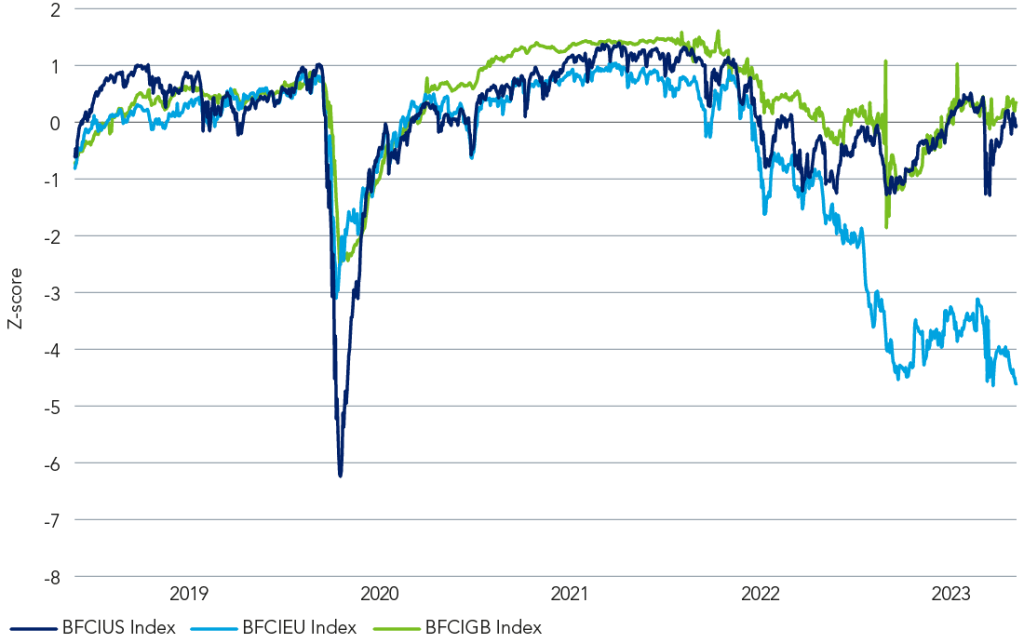

Figure 1: A tightening of financial conditions resulting from March banking stress

Source: Bloomberg, as at April 2023.

More generally, it is now clear that risks of accidents in financial markets have risen as the environment has shifted from extremely easy to somewhat restrictive monetary conditions. There is a renewed awareness that this uncertainty is making for fragile sentiment and more volatile financial conditions, with the recent stress episode in the banking sector seemingly leaving a permanent mark.

There is a renewed awareness that something else could break, risking more episodes of stress in financial markets.

Inflation remains top concern

Even as headline consumer price inflation has come down across major economies, largely due to lower energy prices, various price gauges continue to run well above central bank targets. The composition of inflation is evolving in a concerning way, becoming more pervasive with core inflation proving increasingly sticky.

We still expect inflation to stay on its downward trend through 2024, abetted by lower commodity prices (and related base effects), further normalisation of global supply chain disruptions and, later, the impact from slower demand. Even so, it is likely to end this year well above targets—at 3-3.5% in the US and the eurozone, and 4.5% in the UK. Whether it converges to target in 2024 depends on developments in economic activity and, crucially, labour markets. Year-to-date, labour markets remain tighter than expected, with buoyant wage inflation fuelling services inflation—the largest and most persistent component of inflation.

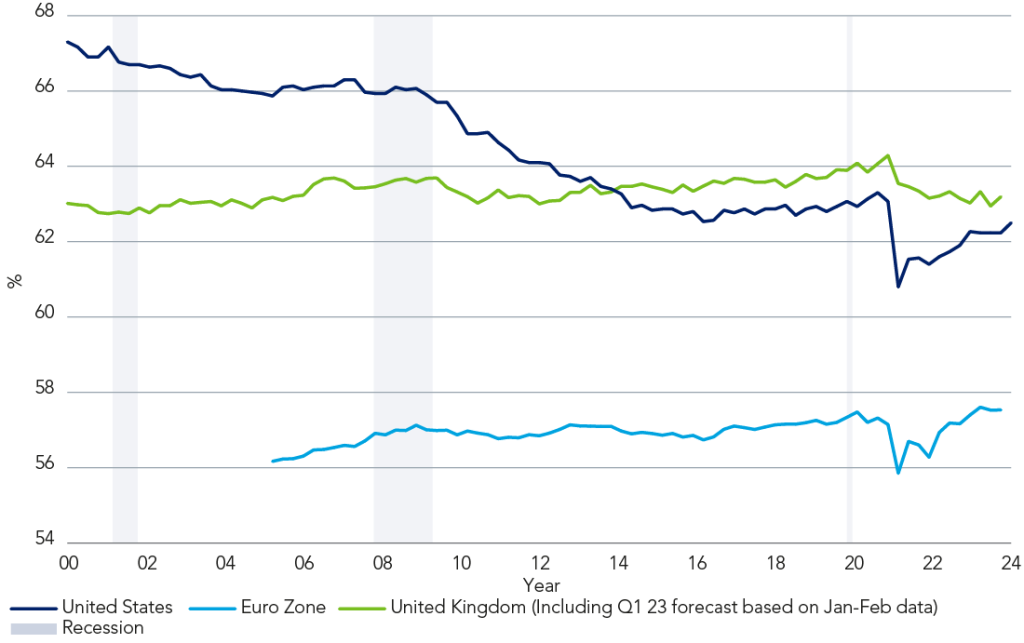

Did Covid permanently impair labour markets?

A key question is whether or not the Covid-19 pandemic built on pre-existing negative demographic trends, thus resulting in a permanently impaired labour supply across advanced economies. The pandemic-related drop in labour supply was initially considered temporary, but participation in the US and UK has yet to recover to pre-pandemic levels, as shown in Figure 2. This is not true in the eurozone, however, where participation rates are now running above pre-Covid levels (though still below prevailing levels in the US and the UK). There are, however, significant differences across EU countries.

Figure 2: Activity rates (15+) in the US, the eurozone and the UK

Source: Refinitiv Datastream, based on OECD data, as at April 2023.

Over the long term, labour force growth prospects are uncertain in all advanced and middle-income economies as the population ages. While the pandemic marked a reversal in the post-global financial crisis trend of higher participation among 50+, cyclical (performance of the economy and financial markets) and structural factors (the need for sustainable public finances) will likely be bigger drivers of older-age labour participation in coming years. The pandemic showed that investment in human capital (education/lifetime training, healthcare) can enable people to work for longer.

The US/China tech ‘Cold war’

It is now a consensus view that the US and China are in a de facto tech ‘Cold War’, with the process of decoupling already underway in strategic sectors such as semiconductors. This decoupling is likely to become more pervasive over time, but slowly and, importantly, in a non-linear fashion as Western positions on China are mixed. The US has focused, in a bipartisan way, on China’s containment for some time while leaders in Europe, which has stronger economic ties with China, have been more cautious and less coordinated. At the same time, China has doubled down on its self-reliance goals, increasingly focusing on the domestic developments of key technologies.

It is not clear that businesses will toe the political line as companies have been reluctant and opportunistic in reconsidering their supply chains. Indeed, Western businesses are keen to keep (or even increase) their access to the huge Chinese market, and will likely move reactively to new regulations, sanctions and incentives, making for a particularly drawn out and bumpy ride. A recent Brookings Institution paper investigating the current status of globalisation concludes that while global trade, capital and labour flows have all slowed since the global financial crisis, there has yet to be a reversal of globalisation.2

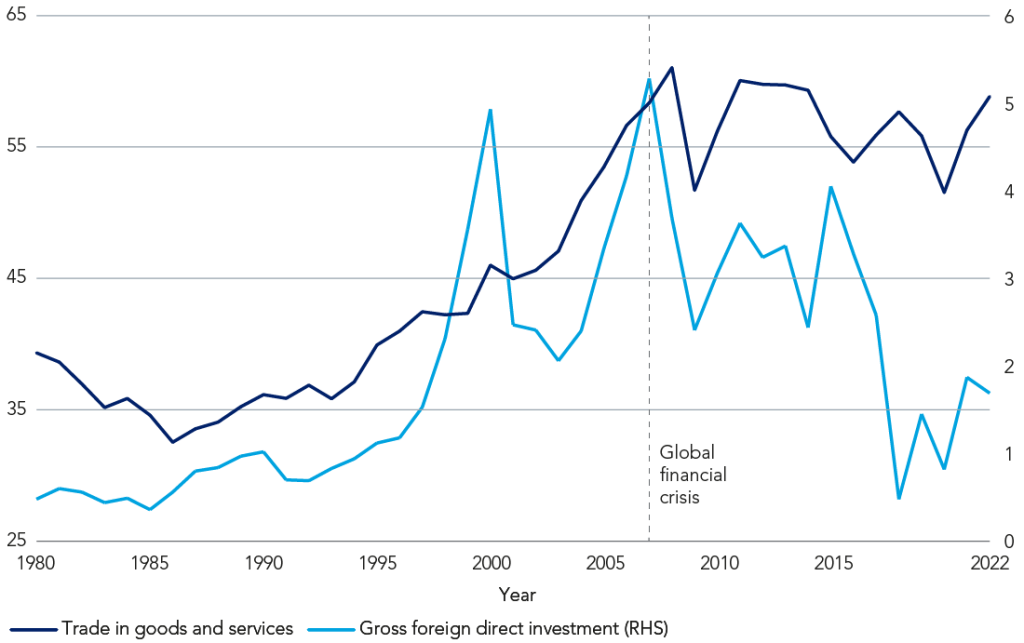

What about ‘slowbalisation’?

Russia’s invasion of Ukraine has sharpened the focus on onshoring and friend-shoring, but the Brookings study notes the US has always shown a tendency toward trading with countries perceived as friendly. An IMF review of the impact of geoeconomic fragmentation found global direct investment already had shrunk from 3.3% of global GDP in the 2000s to 1.3% in 2018-20223 , with investment increasingly concentrated in geopolitically aligned countries. Its model-based scenarios suggest foreign direct investment fragmentation could reduce global output by about 2% in the long term, with the effects being particularly pronounced for emerging economies.

Figure 3: ‘Slowbalisation’ (% of GDP) is more pronounced in foreign direct investment than in trade

Source: International Monetary Fund, ‘A Rocky Recovery’, as at April 2023.

Overall, our conclusions from last year’s 2023 outlook still hold. We think current geopolitical trends will likely weigh on future prospects for globalisation, the main source of worldwide productivity gains in recent decades. While this ‘slowbalisation’ will likely develop gradually and opportunistically over the very long term, it does imply higher costs and efficiency losses, resulting in inflationary pressures and weighing on economic growth globally.

Archive: Previous editions

Please see the most recent editions of our quarterly macroeconomic update below:

Plus, for further insights from our Senior Economist, Silvia Dall’Angelo, please see below:

1 International Monetary Fund, ‘A Rocky Recovery’, as at April 2023.

2 Is the global economy deglobalizing? And if so, why? And what is next? (brookings.edu)

3 International Monetary Fund, ‘A Rocky Recovery: Chapter 4’, as at April 2023.