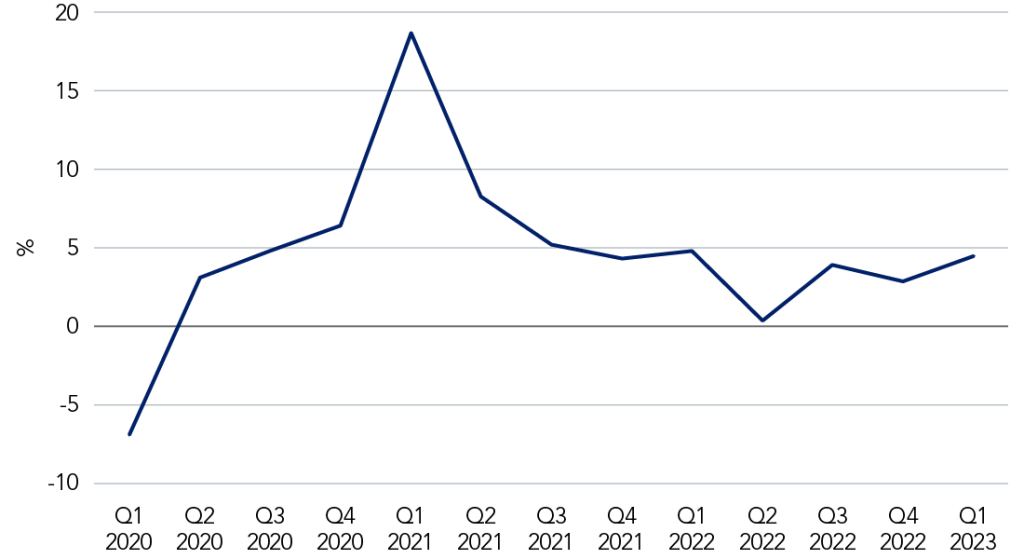

- China’s GDP jumped 4.5% year-on-year in Q1, beating expectations of a 4% rise, amid robust growth in exports and a rebound in retail sales following the end of zero-Covid.

- UK inflation fell to 10.1% year-on-year in March – defying forecasts of a bigger drop – making it more likely that the Bank of England will increase rates at its next meeting.

Better-than-expected Chinese Q1 GDP data provided a slight lift to stock markets this week as investors look for shafts of light amid ongoing concerns about inflation and the possibility of a credit crunch following turmoil in the banking sector last month.

China’s gross domestic product (GDP) jumped 4.5% year-on-year in Q1, beating expectations of a 4% rise, amid robust growth in exports and infrastructure investment as well as a rebound in retail sales following Beijing’s abandonment of its strict zero-Covid policy at the turn of the year1.

Figure 1: Quarterly GDP growth rate in China

“Momentum in Chinese economic activity is likely to remain sustained into Q2, leaving Chinese GDP growth on track to overshoot the government’s official GDP growth target of 5% for 2023,” says Silvia Dall’Angelo, Senior Economist, Federated Hermes Limited. “However, clouds over the medium-term outlook will linger, given the challenges with respect to demographics, productivity, the transition to a more advanced and sustainable growth model, and the prospect of an intensifying tech competition with the US.”

After jumping 1.7% on Monday, Hong Kong’s Hang Seng Index closed down 0.14% on Wednesday. In Europe, the Euro Stoxx 50 closed down 0.20% on Thursday while the FTSE 100 ended up 0.05%. Despite general uncertainty, global equities are up year to date (Euro Stoxx 50 up 15.59%, US blue chip S&P 500 up 7.74%) as at 16:30 on 20 April2.

Things are not yet proving to be as bad as many feared they would be

Market sentiment, however, remains muted with large intra-day swings in this week’s trading sessions, both at index level and within individual shares, suggesting a general nervousness following recent earnings announcements as well investors ‘buying the dips’, says Lewis Grant, Senior Global Equities Portfolio Manager, Federated Hermes Limited.

“Overall the market is left somewhat directionless as investors await further macro releases and forthcoming earnings announcements. With few earnings shocks thus far, news that UK inflation remained stubbornly in double digits has, once again, brought central bank action to centre stage,” he adds.

UK double-digit inflation

UK inflation fell to 10.1% year-on-year in March – defying forecasts for a bigger drop from February’s 10.4% – making it more likely that the Bank of England (BoE) will increase interest rates at its next meeting in May3.

Britain remains the only large, advanced economy to still have double-digit inflation as the country’s ongoing cost-of-living crisis shows no sign of easing. Food price inflation, for example, hit 19.1%, the highest in more than four decades.

“With the labour market and wage growth remaining resilient, we expect to see further rate rises by the BoE as it fights to bring inflation under control,” says James Rutherford, Head of European Equities at Federated Hermes Limited. “The BoE faces a difficult balancing act in reducing the rate of inflation – which has been far more ‘sticky’ than its major peers in Europe and the US – without tipping the economy into a recession. Investors will have to be selective, picking the beneficiaries of inflation and avoiding the victims.”

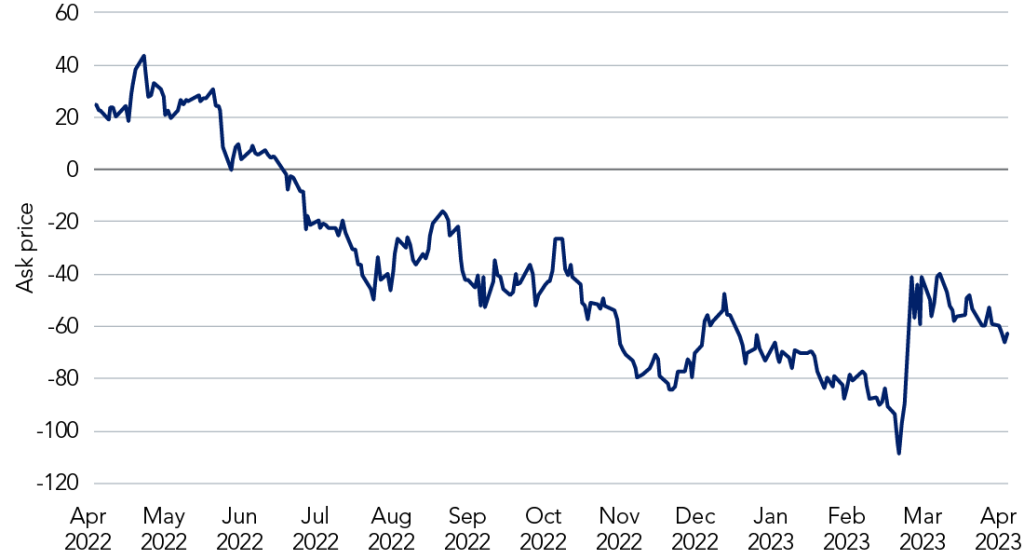

Figure 2: Under control? Two-year versus 10-year US treasury yields

In the US, the yield curve implies that investors are expecting inflation to be under control in late 2023, with rates expected to peak – and even fall – by year end as fears of a hard landing for the US economy ease, Grant adds. The yield on a 10-year US Treasury dropped to a seven-month low this month and was trading at 3.5% at 16:30 on 20 April4.

“Many companies have been pro-active in preparing for recession and are beginning to benefit from more efficient cost structures. While there is no reason for outright optimism, once again things are not yet proving to be as bad as many feared they would be,” Grant says.