- Short-term loans to facilitate physical cross-border transactions can reconcile the divergent needs of an exporter and importer.

- Trade finance has a critical role to play in addressing snags in global supply chains and ensuring that vital commodities continue to flow.

China is heavily reliant on soybeans, which are used as protein feed for hogs and poultry, as well as in everyday staples such as tofu and soy sauce. To meet the huge demand, about 85% of the soybeans China consumes are imported1 and the majority – 58.1 million tonnes last year2 – are shipped from Brazil.

Soybeans are a perishable commodity. Rains and drought in Brazil have delayed the harvest in recent years – playing havoc with shipments which have to travel more than 20,000km by sea – and squeezing available soybean supplies in China.

While many in the West often associate imported goods with high-end items, for much of the developing world such shipments cater to more basic needs. Indeed, transactions between developing nations – so-called south-south trade – has increased at an exponential rate over the last couple of decades3.

The soybean trade between Brazil and China illustrates how trade finance, essentially short-term loans to facilitate physical cross-border transactions, can play a crucial role in reducing risks and reconciling the divergent needs of an exporter and importer.

Trade finance introduces a third party to transactions to mitigate the payment risk and supply risk. It provides the exporter with receivables or payment according to the agreement while the importer might be extended credit to fulfil the trade order. The loans, which are made to finance a specific transaction, are collateralised by the goods being financed and are self-amortising from the proceeds of the transaction.

Federated Hermes4 has been offering trade finance in a fund format to institutional investors since 2009. The risks inherent in any transaction are analysed on a case-by-case basis to determine how they can be mitigated, while at the same time ensuring the risk-adjusted return remains attractive.

A differentiated strategy

To effectively analyse and mitigate risk in any trade finance transaction, rigorous legal and operational due diligence is required from the outset.

Federated Hermes sources deals through a network of leading global banks and the due diligence process probes a wide range of investment criteria, including environmental, social, and governance (ESG) factors.

The loan rates float at a spread over a short duration index, allowing for adjustment to inflation and the lenders build risk mitigants into the deals to reduce the chance of loss.

As a short-duration asset class, most banks hold their positions to maturity and as a result there is a limited secondary market. Extensive documentation is required; trade settlement occurs in 10-20 days and is considered illiquid.

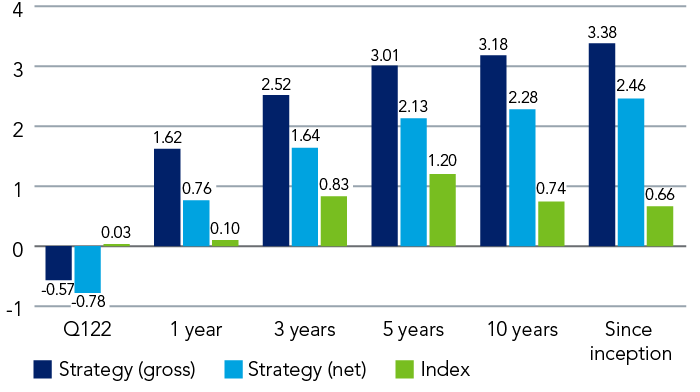

Figure 1: Federated Hermes trade finance (annualised returns, US$)

Past performance is not a reliable indicator of future performance.

Uncorrelated returns

Federated Hermes’ trade finance strategy offers investors the potential to access uncorrelated alpha with limited reliance on traditional return drivers; and sidestep the macro risks and volatility that have dogged public markets this year because of soaring inflation, rising rates and the war in Ukraine.

Unexpected events can always happen, of course. The speed with which Russia’s invasion has upended global trade is unprecedented and the full impact has yet to be felt. The conflict has led to a shortage of fertilisers – such as nitrogen, phosphorous and potassium – and sent pricings skyrocketing, which is likely to have a knock-on impact on food supplies. In response, farmers in many developing countries have taken to rotating crops and using fewer nutrients, which could reduce crop yields.

But such risks in any individual transaction can be navigated and reduced; risk mitigation techniques include collateral management of the goods, permanent control of the title over the goods, ring-fencing cash flows and trade credit insurance. The payments, consisting of both principal and interest, are made on a predetermined schedule, ensuring that the loan will be paid off by the end of an agreed-upon term.

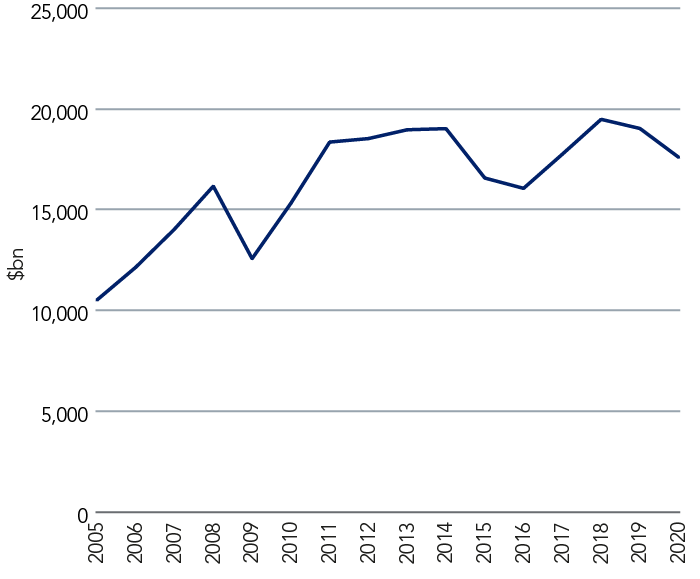

Figure 2: global export value of trade in goods (2005 to 2020)

Supply-chain snags

As countries around the world emerge from the Covid-19 pandemic and grapple with the fallout from the Ukraine conflict, trade finance has a critical role to play in addressing snags in global supply chains and ensuring that vital commodities continue to flow. (In the aftermath of the 2008-2009 global financial crisis, it was trade finance that helped keep shipments moving, according to the International Monetary Fund5.)

Many developing countries are dependent on key cross-border transactions. In Egypt, for example, wheat imports form the cornerstone of the government’s bread-subsidy programme that millions of people rely on. The Egyptian government buys wheat in regular international tenders; last year more than 80% of its wheat imports came from Russia and Ukraine6. As global grain prices soar because of the conflict, trade finance can help the government secure alternative sources of supply and ensure these vital transactions take place.

Although the demand for trade finance continues to grow, a complex regulatory environment coupled with a lack of understanding of the asset class has contributed to a global shortage of trade financing. The gap for global trade finance opportunities has been valued at $1.5tn by the Asian Development Bank7 creating enormous opportunities in next few years. Amid an uncertain economic backdrop, a diversified pool of trade transactions has the potential to deliver the kind of ‘pure alpha’ that many investors are searching for.

Greensill: a totally different model

Greensill Capital, which filed for insolvency last year, represented a sub-set of the wider trade finance market. It’s worth pointing out how its business model was completely different to the trade finance operation practiced by Federated Hermes.

Greensill offered supply-chain finance, essentially a short-term cash advance to help corporate clients extend the time they have to pay their bills. These cash advances were then packaged into insured bond-like securities to offer investors higher yields than they could receive from bank deposits. While the securities were insured in order to get high investment grade ratings, the vast majority of Greensill’s revenues came from non-investment grade borrowers.

Rival asset managers then offered products heavily reliant on Greensill’s trade finance notes. However, when insurers declined to renew policies that covered Greensill’s securitisations amid concerns about losses, the asset managers were forced to close the funds and Greensill filed for insolvency in March 2021.

Such models, relying on formal agreements, are totally different from the bespoke trade finance strategies practiced by Federated Hermes as outlined in this article.

2 China’s Jan-Feb imports of Brazil soybean up on year, U.S. cargoes fall | Reuters

3 The Rise of South-South Trade: Polycentric Patterns (manchester.ac.uk)

4 Federated Hermes refers to Federated Hermes, Inc (FHI)

6 Egypt’s Hunt for Wheat Takes on New Urgency as Stockpiles Shrink – Bloomberg

7 Asian Development Bank, 2019 Trade Finance Gaps, Growth, and Jobs Survey.