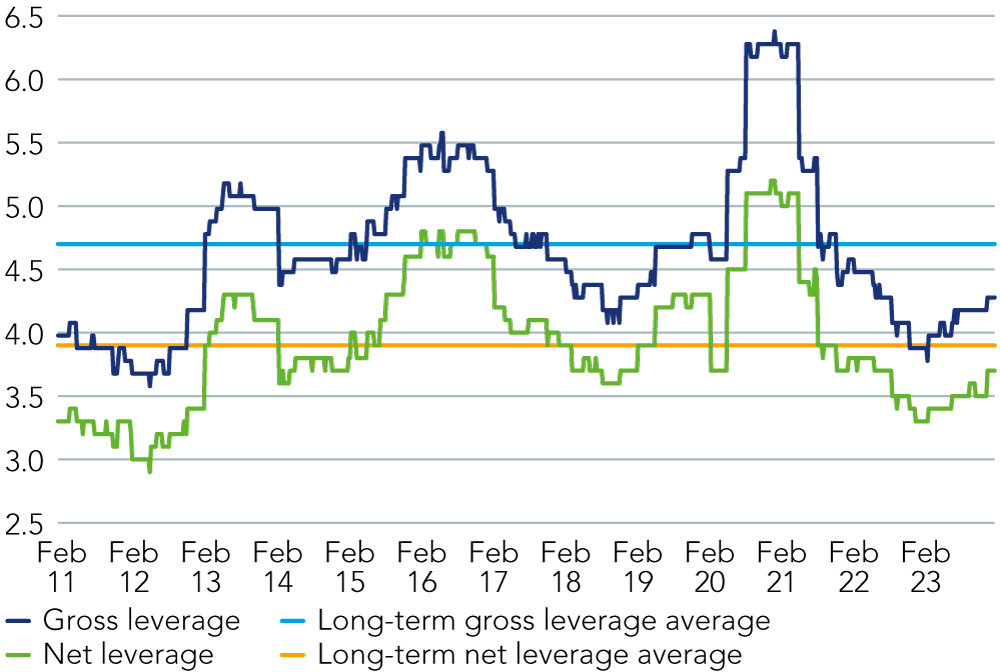

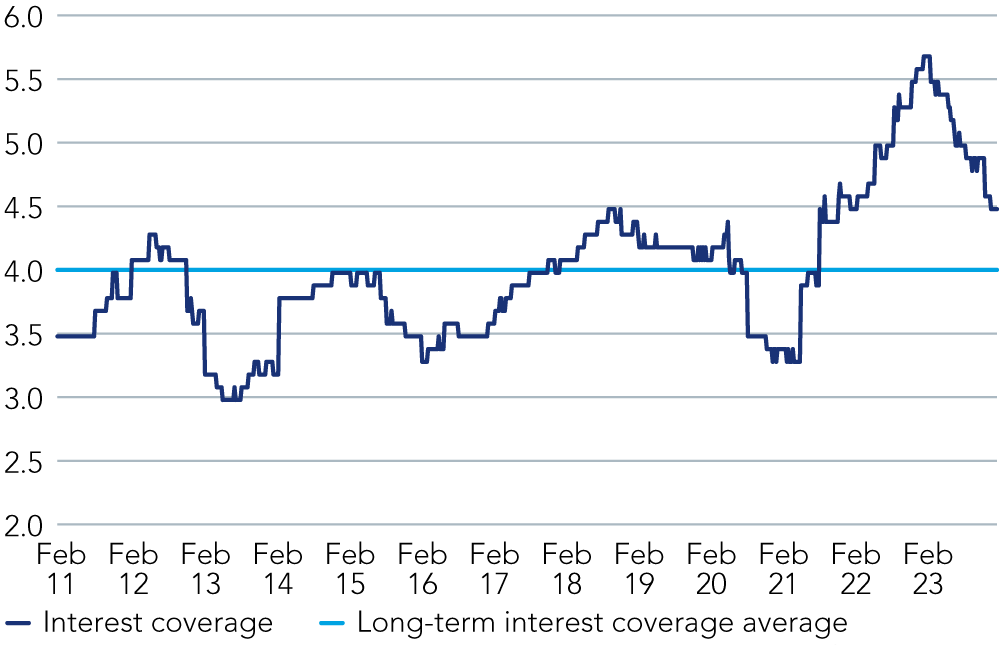

Credit fundamentals continued to modestly weaken towards the end of 2023, with both leverage and interest coverage metrics trending towards long-term averages from the lows and highs respectively witnessed a year ago, as shown in Figures 1 and 2 below.

Figure 1: Leverage increasing towards long-term averages

Source: BofA, as at 31 December 2023.

Figure 2: Interest coverage deteriorating towards long-term average

Source: BofA, as at 31 December 2023.

With the backdrop of US economic data remaining resilient (though weaker in Europe), materially lower commodity prices and somewhat improved financing conditions in the capital markets since the US Federal Reserve’s pivot in December, the current reporting season is important in reassessing our more cautious stance towards corporate credit fundamentals.

Specifically, we are looking for any signs of either improvement or deterioration in fundamentally challenged sectors and any sectors adopting a more cautious outlook, as communicated previously by a number of industries. For example, the chemical industry suffered last year from destocking and weakening European demand and has provided little visibility for the timing of recovery, non-food retail companies noted consumer spending pressures, while defensive healthcare companies delay spending decisions, despite continuous EBITDA growth.

Despite yields and cost of capital remaining historically high, the material rally of treasuries and spreads since October (100bps tighter on both) are benefitting issuers in the form of lower debt costs in the capital markets. This is potentially putting less pressure than previously anticipated on issuers’ cash flows as companies refinance upcoming maturities.

We are looking for any signs of either improvement or deterioration in fundamentally challenged sectors and any sectors adopting a more cautious outlook.

However, the situation remains fluid. The ongoing conflict in the Middle East and the threat to the shipping industry will likely result in rising costs and margin pressure in industries such as retail. Historically tight valuations on a spread basis are likely to lead to greater dispersion and severe spread underperformance in credits with disappointing earnings, especially within levered capital structures with upcoming maturities or other credit-negative idiosyncratic developments.

This uncertain environment requires vigilance from credit investors and an in-depth understanding of underlying operating and financial fundamentals as well as ESG dynamics of credits. At the same time, this of course will present investment opportunities for savvy credit investors in some of the oversold credits.

Issuer behaviour remains broadly neutral

We continue to see issue behaviour as broadly neutral with limited evidence of a shift to more creditor-friendly capital-allocation policies in the most recent 3Q23 earnings cycle, with the exception of specific idiosyncratic sectors.

Issuers in the chemicals space have cut dividends and/or explored asset sales to shore up balance sheets in the face of gloomy demands from ongoing destocking and lacklustre end markets. However, this is not a wider theme seen across the universe and we have seen buybacks and dividends continue (albeit often from a position of strength) in many sectors including retail, healthcare and energy.

M&A volumes are still depressed but premiums are very high, which may indicate opportunistic transactions at companies where equity values are depressed.

The use of proceeds of new issuance in the high yield market has been skewed towards refinancing.

On documentation, issuer-friendly qualitative changes cleared the market in 3Q23 on terms such as contribution debt, financial calculation flexibility and EBITDA add-backs.

To hear more from the team on their outlooks 2024, please follow the link below.

360°, Q1 2024: Dispersion, disparity, duration

Find out more about our wider credit offering.