It is our duty as men and women to proceed as though the limits of our abilities do not exist. We are collaborators in creation.

Pierre Teilhard de Chardin

Quarantined economics: the impact of Covid-19

The economic shock of the coronavirus pandemic inevitably invites comparisons to the 2007-08 global financial crisis. However, in many ways, it looks very different. In 2008, the crisis started most visibly in the financial sector before spreading to the real economy. Conversely, today’s crisis is first and foremost a public health emergency that is transposing itself onto the real economy, leaving financial markets to assess the extent of the economic hit.

The global pandemic is – and will continue to – affect citizens in their dual identities as savers and investors – but by how much and for how long? Can a virtue be made of a necessity as measures are taken to get the economy and society back on their feet?

Today we are in far looser territory with respect to monetary and fiscal policy than at any time in recent memory, including the 2007-08 global financial crisis. Quite rightly, central banks and governments have been quick to act. And although many EU countries have been slow to announce new fiscal measures, the US and the UK have the loosest overall monetary-fiscal policy mix probably since World War II.

In the US, lawmakers struck a $2.52tn stimulus deal to limit the damage from the virus, but it severely impacts the budget deficit (in April, the US budget deficit swelled by a record $738bn)1. Even the country’s underlying (cyclically adjusted) deficit, which attempts to smooth out variations from recessionary rises in unemployment benefits and tax revenue shortfalls looks likely to near 11.5% of GDP in 2020 and 2021, up from 6.6% in 2019.

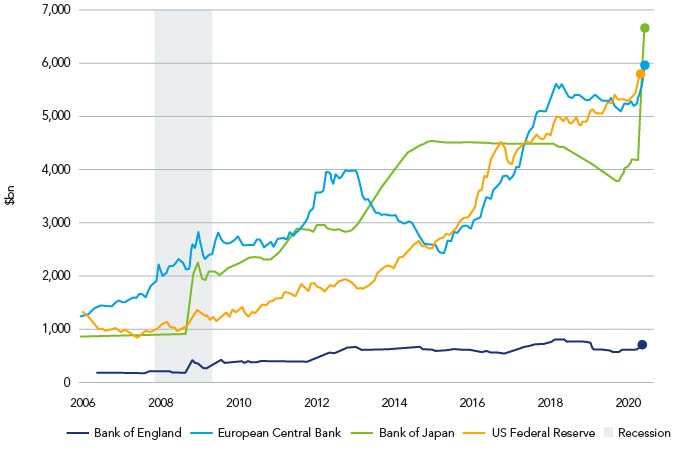

Meanwhile, the UK’s stimulus package – which so far is lower than its US counterpart (see Figure 1) – will also be raised considerably by the Chancellor’s encouraging tax-breaks and pay measures to free up cash flow. As such, we expect an underlying deficit of about 9% of GDP in 2020: this will probably increase even further should additional stimulus be released. Indeed, in April, the Office for Budget Responsibility suggested that a government debt-to-GDP ratio of 100% is likely if the lockdown is extended (up from 80% in 2019).

Figure 1. G5 central banks’ quantitative easing levels

Source: Refinitiv Datastream, based on central bank data, as at May 2020.

However, with much of the monetary ammunition already fired, the pressure to loosen policy further has fallen to fiscal policy. With escalating government debt being mopped up by record central bank quantitative easing (QE), it is difficult to see how QE can be lifted even when we return to more normal levels of economic activity. Early QE unclogged the financial system, but the transmission mechanism to consumers and companies has been woefully slow. And, by bloating asset prices rather than disposable incomes, this approach can be accused of reaching only those (i.e. asset owners) who probably needed it least. As demand stutters, central banks perpetuate a vicious circle that they now dare not break.

Tackling climate change: the green road to a resilient recovery

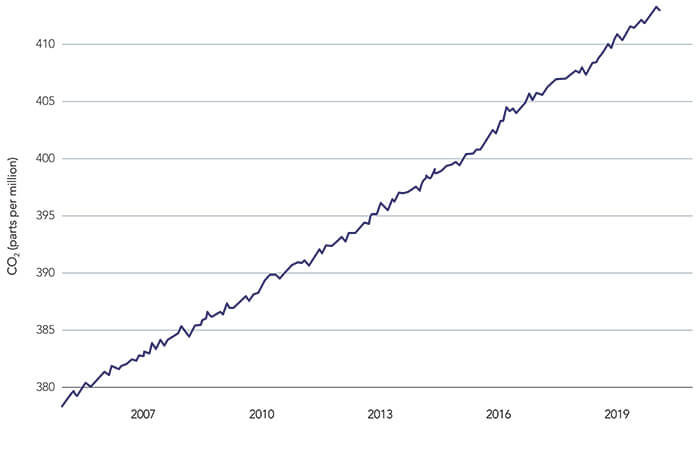

Before we began the fight against the coronavirus pandemic, climate campaigners and progressive investors, alike, were despairing at the lack of progress in curbing the exorable climb in greenhouse gas (GHG) emissions. Data from the World Meteorological Organisation showed that GHG in the atmosphere rose to new records last year and that levels of carbon dioxide were 18% higher from 2015-2019 than in the previous five years2.

Figure 2. No peak in sight? The growth of GHG emissions

The world it seemed was sleepwalking into a climate catastrophe – and any pivot away from business-as-usual behaviour to push global emissions onto the downward path it needed seemed too much to expect, especially with evidence-shy politicians in power. Moreover, with the long-held orthodoxy by Treasuries that ‘there is no money’ for social welfare or accelerating the shift to a greener economy, the net zero carbon transition seemed beyond reach.

That was life before lockdown. But when the coronavirus aggressively spread across the world this year killing more than 300,000 people, governments opened the fiscal floodgates and there was a rapid change in societal activity. In these tragic circumstances, there is hope: suddenly, a new, more equitable and resilient future seems possible – and there are two new levers at the disposal of willing governments. They can:

- Attach climate-friendly conditions where possible when fiscal sponsorship, subsidies and bailouts are targeted, perhaps to identified production sectors.

- Design a post health crisis fiscal stimulus with a built-in condition to facilitate a rapid pivot for companies that need to align operations, strategy and capital expenditure with the net-zero transition.

In the short term, of course, the economic priority must be the protection of productive corporate activity and jobs3. But the growing momentum around the just transition thesis should not be ignored: if we are to build consensus on meaningful collective climate change action, the transition must be inclusive. And although it would be distasteful and unjust to make the climate transition a condition of access to economic lifelines in the very short-term, it should not be disregarded completely as an important issue to consider.

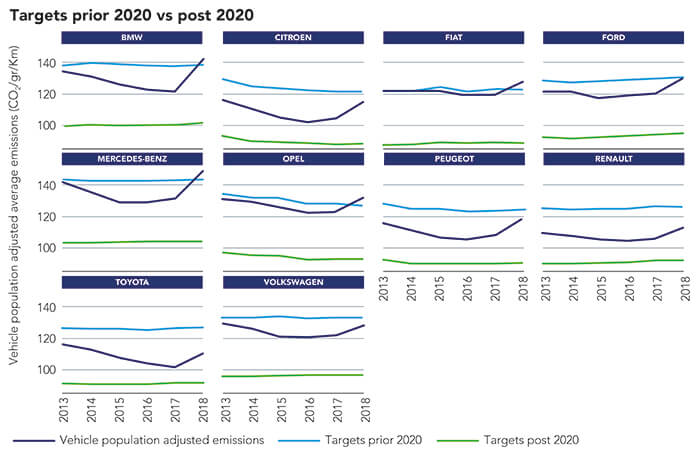

Consider the European car industry. It has singularly failed to shift its manufacturing and marketing efforts to ensure it meets stringent fleet-wide fuel efficiency standards put in place 12 years ago and reconfirmed in 2014. Nevertheless, the European car industry is both calling for immediate liquidity support for automobile companies, their suppliers and dealers. It is also urging the European Commission to delay the introduction of stricter carbon dioxide standards for new vehicles, purporting that the coronavirus pandemic limits its ability to comply with new rules. However, reports suggest that this claim is unfounded and could potentially damage the long-term sustainability of the European car industry4.

Figure 3. Mission possible? Progress made by car manufacturers towards achieving emission targets since 2008

Similarly, airlines, crippled by the growing global lockdown, have demanded lasting relief from environmental taxes – a move that pits their short-term survival against longer-term emissions goals. This looming fiscal wrangle highlights shifting environmental battle lines, raising broader questions for governments injecting billions into their ailing economies: should bailouts come before climate objectives? Or should they instead be used to advance climate action?

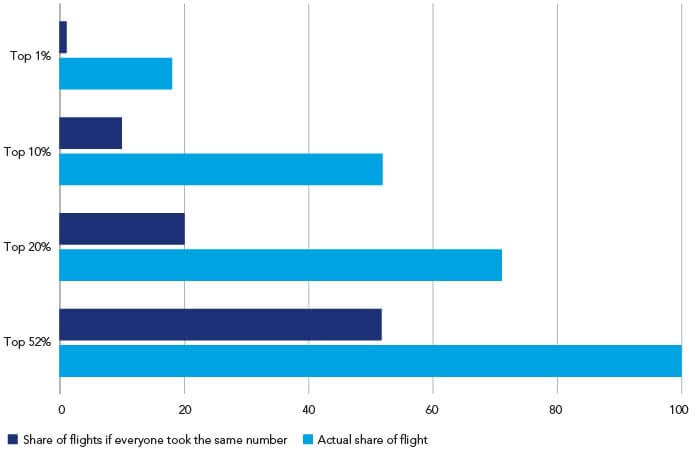

We think governments should adopt the latter approach. That’s because, before the lockdown-induced current drop of in travel, emissions from the aviation sector overall have continued to grow. If this growth resumes at those pre-coronavirus rates, by 2050 air travel threatens to consume a quarter of the entire carbon budget the world can still emit to meet the stretch climate targets set by the Paris Agreement5. Worse still, the majority of air travel is undertaken by only a fraction of the population. According to data released by the Department of Transport, 48% of people living in England did not take a single flight abroad in 2018, while the top 10% of frequent flyers in the country were responsible for almost half of all international travel.

Figure 4. 10% most frequent flyers took more than half of flights abroad in 2018

Governments have imposed new levies to slow the growth in air traffic and emissions, and the European Union plans to begin taxing jet fuel. However, this is unlikely to be enough to pivot the industry from its currently unsustainable trajectory.

Access to bailout funding would provide an opportunity to set a rapid course correction in place: airlines would be required to invest in cleaner technology and streamline service offerings to ensure flights are full. Prices would also need to increase – in part through paying taxes – to reflect the environmental damage caused by the fuel used and a frequent flyer levy would need to be set at a level appropriate to the contribution frequent flyers make to aggregate carbon emissions from the sector. Austria appears to be paving the way in this regard: there have been proposals to attach environmental conditions to state support for Austrian Airlines. Going further, if loans are provided, the interest rates could be linked to the achievement of sustainability milestones – thereby incentivising action from recipient firms.

A filter should also to be applied to ensure that bailouts are made available to businesses that have managed their balance sheets in a responsible fashion to date. For example, it has been reported that the four biggest US airlines have allocated an average of 115% of their free cash flow to share buybacks6. Consequently, arguments ensued that these airlines are now highly exposed to business interruption caused by various country-level lockdowns. However, only one of these companies – American Airlines – appears to have had an unsustainable dividend and share buyback programme when compared to levels of free cash flow7. We believe this type of information should be reflected in decisions made about who gets access to bailout capital.

Meanwhile, as the West Texas Intermediate (WTI) oil price hit an unprecedented negative price level in recent months, other industries too were seeking bailouts – and these bailouts would appear to offer no strategic return for taxpayers faced with the reality of a rapidly heating planet.

Consider the fossil energy industry. US oil producers sought a bailout in the form of a $3bn US government purchasing scheme to top up the country’s strategic petroleum reserves. This request was made despite the industry’s history of borrowing from debt capital markets during periods of lower oil prices to fund dividends so as to position themselves as attractive from an income investment perspective. This was however blocked by Democrat legislators. Otherwise, it would have served as just one of a slew of actions, including a roll back of fuel efficiency standards in cars, being taken to shore up an industry that is not changing fast enough to meet the challenges implicit in facing the climate emergency.

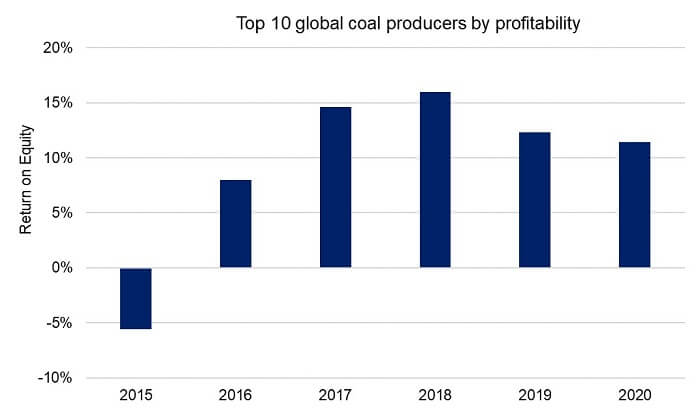

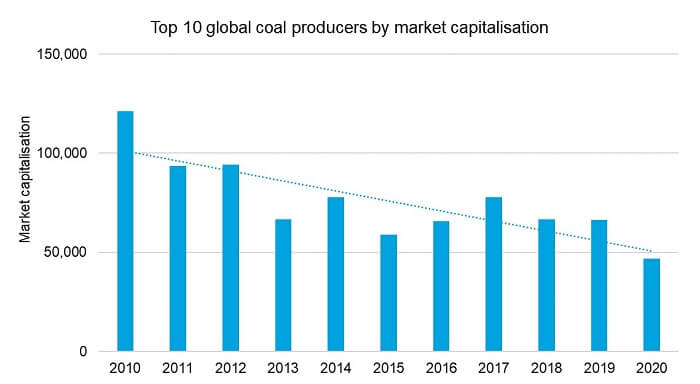

What’s more, media reports suggest that the National Mining Association is pleading for an end to taxes imposed on firms that are used to pay coal miners affected by black lung disease and fund the clean-up of high priority abandoned coal mines8. Using public funding to prop up companies whose profitability has been in steep decline over the last five years as the economy shifts to a more sustainable footing through absolving them of historical social and environmental debts seems at best a travesty.

Figure 5. The profitability of coal companies has been declining since 2010

Figure 6. The valuation of the top ten global coal companies has fallen since 2010

Of course, adding these proposed conditions to bailouts is not without precedent: in the wake of the 2008 global financial crisis, the then US President Barack Obama used the government bailouts of General Motors and Chrysler to compel them – and by extension the entire automobile industry – to accept stringent new fuel-economy standards9. This may have been the single biggest climate change policy win (President Trump is now working with the auto industry to dismantle those rules).

The principle should be clear: when you take money from society, you owe society something in return. We must drive home this message given that emerging epidemiological observations suggest that those with lung damage (including damage caused by air pollution) appear to suffer worse symptoms and higher mortality rates after contracting coronavirus than those without.

Collectively, we owe it to ourselves and future generations to use this money to put the economy on the pathway towards addressing the impending climate emergency. Put simply, companies should not qualify for government bailouts unless they promise to establish – and meet – the targets set out in the Paris Agreement on climate change and demonstrate their plan in the coming months.

This does not mean that every company will have to dismantle its business model or cut jobs. Instead, in many cases, it will require an accelerated shift in the substitution of service and product offerings to make them more sustainable as well as a plan of action attached to retrain and redeploy staff as needed.

An unprecedented wake-up: a call to action on climate change

In the long run we are all dead.

John Maynard Keynes

Mark Carney, in his role as Financial Adviser for the COP26 summit, called for action on climate change in February 2020, including integrating climate change factors into every investment decision.

However, one of the challenges for a listed securities asset manager, like Federated Hermes, is that the vast majority (that is, more than 80%) of the investible universe is not aligned to the Paris Agreement.

But we must change this – and fund managers can use two tools:

- Engagement: fund managers can engage companies to encourage/insist they shift their strategies; and

- Advocacy: fund managers can advocate for market norms or public market rules to change to incentivise or regulate a change in business models.

Governments have the chance to help investors deliver climate mainstreaming by using, where appropriate, the financial support and stimulus they deploy to restore demand and production in the economy in a manner that is consistent with the Paris Agreement. These conditions do not need to be exercised in the current crisis, of course, but they can be kept in the locker for when growth is restored.

We have an opportunity to learn from the global coronavirus pandemic and see what is possible when the public and private sectors work together, in good faith, toward a shared goal. For example, two of the world’s biggest pharmaceutical firms, GSK and CEPI, are working in partnership to develop and deliver a vaccine at an unprecedented scale and speed. Tesla is retooling parts and US-based manufacturing facilities to produce ventilators rather than cars. The beer manufacturer BrewDog is making hand sanitiser and distributing it free to the NHS and local charities – and luxury products group LVMH has done the same in France.

These are just examples of what some companies have done to play a role in fighting the pandemic. We should capitalise on what we have seen is possible in recent months when the public and private sectors come together in a spirit of shared endeavour.

We suggest that the government should follow the proposal set out by Carney – and ensure the decision-making around any stimulus includes the consideration of the role each sector can play in delivering an economy in line with Paris alignment.

The UK Committee on Climate Change, in its Net Zero 2050 report (which can be considered as a proxy for the required global action), has said a net-zero GHG target is not credible unless UK (and de facto global) policy is ramped up significantly. Most sectors will need to reduce emissions close to zero without offsetting them; the target cannot be met by simply adding the mass removal of CO2 onto existing plans in the UK for the 80% target. Delivery must progress with far greater urgency. Many current plans are insufficiently ambitious; others are proceeding too slowly, even for the current 80% target.

- Scrap commitments to build infrastructure that will make it impossible to deliver net zero in 2050 and risk asset stranding. This includes airport expansion – including the controversial third Heathrow runway in the UK – and the expansion of oil and gas infrastructure – including the US-Canada Keystone XL Pipeline.

- Instead, focus on stimulating investment in infrastructure needed to reduce emissions and invest in training to deliver the skilled workforce needed to deliver these outcomes. This should include, as a priority, rolling out nationwide programmes to deliver low-carbon buildings by insulating them to a high standard and installing solar panels and other low carbon energy sources where suitable. This must be fully funded in an equitable fashion, taking account of income levels in the case of housing. It could be a prime target for stimulus that also creates high-quality jobs.

- Invest in nationwide electric and hydrogen vehicle infrastructure to accelerate the shift to clean private transportation networks. The hydrogen network could be linked to investment in the first Carbon Capture and Storage (CCS) clusters that start to decarbonise industrial emissions. This is technological know-how that could be exported. These efforts would also go a significant way to addressing the health inequality caused by air pollution, which has been identified as one of the factors affecting the poor more than the wealthy in general – and specifically in the case of Covid-19.

- Agriculture is already facing a period of considerable change. Future success will require diversification of incomes as well as taking opportunities that come with transformational land use change. Moreover, policy that encourages farming practices to reduce emissions must move beyond the existing voluntary approach. In the UK, financial payments in the Agriculture Bill could be linked perhaps to actions that reduce and sequester carbon, though with Brexit effects yet to be borne, this may be best exercised further down the line.

- Boost spending on public transport and cycle networks to accelerate the shift to sustainable modes of transport and invest in increasing green spaces. In turn, this will improve public health overall.

- Double down on the efforts to strengthen the global digital infrastructure, notably to more remote areas that are poorly serviced. This greater connectivity, which has proven to be a lifeline during the pandemic, can enable the permanent ‘banking’ of a portion of the travel-based, GHG emissions society, who have benefitted from during the lockdown through the normalisation of more virtual meetings.

- Ensure there is a resilience ‘overlay’ to the siting and building of all infrastructure so that it is fit to withstand currently locked in climate changes, along with increased investment in flood defences.

These proposed measures combined with climate-aligned bailouts could represent a turning point in the fight against climate change and some of the environmentally driven health manifestations of inequality laid bare by the current health crisis.

The use of public money to shift the real economy onto a sustainable footing, buttressed by strong engagement by investors, will help accelerate the shift to a world in which net zero investing is mainstream. On 30 March 2020, EU leaders issued a statement in which they agreed to consider climate in the European coronavirus recovery plan. Although the details of the plan itself still have to be worked out, a statement said they had agreed that it should be consistent with the Green Deal-based « green transition ». Canada has launched a financing facility that the country’s largest employers can access to keep operations going. Among the requirements are that firms should not have been convicted of tax evasion and that they commit to publish annual climate-related disclosure reports consistent with the Task Force on Climate-related Financial Disclosures (TCFD), including how their future operations will support environmental sustainability and national climate goals. Other governments could and should follow suit.

Seeing the world anew

The pandemic is a cataclysmic event, but there is nothing inevitable about what comes next.

Since the lockdown began, something extraordinary has happened: people all over the world are waking up to a taste of the possibility of the beauty of the natural world being welcomed into day-to-day life. A noticeable and peaceful calm descended for a period over major cities, including London. With planes largely grounded and road noise reduced, birdsong became clearly audible. Nitrogen oxide (NOx) levels dropped across the world as businesses closed and vehicles stayed parked. Meanwhile, in Punjab, the Himalayas are visible to some populations for the first time in 30 years thanks to a reduction in pollution levels.

As countries begin to ease lockdown restrictions, we must remember that politics is the art of impossible made possible. Let’s turn our impossible situations into possible solutions. Governments must work with private investors to seize this opportunity, making a virtue of a necessity and putting in place the foundations of a green and resilient recovery from the disruptive heartbreak of recent months. We have a moment – let’s not let the enormous sacrifices in this crisis be without some benefit for the longer term.

1 Source: US Treasury Department, as at 12 May 2020.

2 “Global Climate in 2015-2019,” published by the World Meteorological Organisation in April 2020.

3 This may entail, of course, some so-called ‘zombie firms’ failing. However, this can be considered natural creative destructions since it allows space in the market for fresh entrepreneurial activity to emerge.

4 “EU car lobby’s renewed attack on cars CO2 targets – on the back of COVID-19,” published by Transport and Environment in March 2020.

5 “Analysis: Aviation could consume a quarter of 1.5°C carbon budget by 2050,” published by Carbon Brief in August 2016.

6 “US airlines show it is time to switch off buyback machine,” published by the Financial Times in March 2020.

7 “Airlines » Didn’t Waste All Their Cash Flow on Share Buybacks: American Airlines Did,” published by Nasdaq.com in March 2020.

9 « How the carmakers Trumped themselves, » published by The Atlantic in June 2018.