Cosmological theories live or die based on how accurately they predict phenomena in the observable universe.

Incredibly, though, the current scientific consensus suggests the future (and past) of the cosmos hinges almost entirely on the unseen energy and matter lurking in the invisible universe.

As explained by US space agency NASA, “roughly 68% of the universe is dark energy”.

“Dark matter makes up about 27%,” NASA says. “The rest – everything on Earth, everything ever observed with all of our instruments, all normal matter – adds up to less than 5% of the universe.”

To be fair, humans have developed a reasonable understanding of the 5% of stuff we can see; a view perhaps best-encapsulated in the so-called ‘standard model’ of physics briefly sketched out in the previous Fiorino.

But while physicists might be reasonably certain that the dark forms of energy and matter exist, to date their true nature remains a mystery to science.

Like nature, however, science abhors a vacuum with many theories spun out to fill the universal knowledge gap. For example, various physicists have postulated dark matter could be composed of very low-mass stars or super-massive black holes: another hypothesis conjures up a ‘hidden valley’ in the universe, a parallel world made of dark matter well beyond the explanatory powers of the standard model.

In one sense the solution to the dark matter mystery is irrelevant; scientists already know that something other than ordinary matter is needed to explain observed gravitational effects. Cosmological theories must account for dark matter or the universe collapses.

Jim Peebles, Astrophysicist and Nobel Prize laureate

Bank stress-testing to spotlight climate risks

Meanwhile, our financial system has until recently relied almost entirely on its own insular set of ‘standard models’ to predict outcomes. The ‘efficient markets hypothesis’, for instance, and the related Capital Asset Pricing Model (CAPM) often form the basis of risk-and-return forecasts for share investors (among others).

Credit analysts, similarly, have an array of statistical tools and assumptions to weigh up the relative risks and returns of fixed income portfolios.

Of course, the standard models of finance are more art than the science practised by particle physicists but investors as a rule base their faith, and capital allocation, on these statistical analyses of market risks.

For all their internal mathematical robustness, however, financial models cannot contain all risks in their formulae – as history has a habit of proving. The 2007-8 Global Financial Crisis (GFC) was undoubtedly the most significant recent reminder that investors can’t ignore the ‘dark matter’ of markets, exerting its invisible influence beyond the boundaries of standard deviations.

Despite the systemic shock, the GFC had at least one positive side-effect in prompting regulators and investors to explore alternative models that probe risks on the fringes of the bell-curve where the fat-tailed black swans gather. The crisis saw scenario- or stress-testing rise to the fore as a tool to examine what could happen under the darkest possible circumstances.

In his aptly titled GFC memoir ‘Stress Test’, former US Treasury Secretary, Tim Geithner, points out why regulators and risk managers need to “set aside assumptions about implausibility of a major shock and study the impact of that shock if it somehow happened”.

Geithner’s warning applies just as equally to risks emanating outside the traditional financial system where the scenario-bending force of climate change is now being taken seriously by regulators, investors and the public.

Led by regulators across the world, companies and institutional investors are rapidly incorporating climate risks into their financial forecasts and strategies. The formal assessment of climate risk in financial projections is accelerating particularly in countries, or regions, where governments have put in place clear environmental policies. Europe is probably the global leader in driving the climate risk-testing agenda where French financial institutions were the first to report results according to new guidelines in April this year.

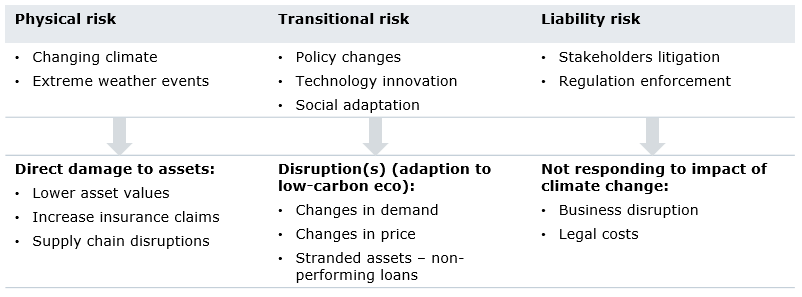

Climate scenario-testing has now evolved to consider financial risks across three broad categories, as illustrated in figure 1.

Figure 1. Taxonomy of climate risks

Source: Federated Hermes (elaborated on various sources NGFS, ECB, DNB, ACPR, BoE and Apra), as at July 2021.

Most regulators are developing climate-reporting rules in their respective jurisdictions based on the climate scenarios and guides published by the global Network for Greening the Financial System (NGFS).

The European Central Bank (ECB) is set to test significant banks in the region for climate risks in 2022 with regulators in Australia, Brazil, Canada, Hong Kong, and Singapore announcing similar exercises either this year or next.

Network for Greening the Financial System (NGFS)

The NGFS is a group of central banks and supervisors who share best-practice scenario-testing tools, backed by scientific research, for environmental and climate-risk management in the financial sector. Among other key objectives, the NGFS aims to mobilise finance to support the transition to a sustainable economy.

Figure 2. NGFS Climate Scenarios Framework

Source: NGFS, Federated Hermes, as at July 2021.

Bank of England sets data starter challenge

In 2019 the Bank of England (BoE) set a goal of assessing about 80% of the UK banking system for exposure to corporate climate-risks in its first ever stress-test of the kind1.

And this June the BoE unveiled an ambitious, and controversial, plan requiring the selected banks to apply the climate scenario-tests across their respective 100 “largest and most material” corporate counterparties.

It’s not yet clear just how the BoE climate stress-test will translate to standard bank metrics such as percentage of loan books or proportion of risk-weighted assets.

We can calculate the impact of the 100 companies on bank financial yardsticks in a number of ways – and, in any case, the BoE has set this benchmark as a minimum, expecting institutions to extend the climate risk-testing further over time.

As a rough guide, though, based on conversations with Barclays – a bank with a sound climate strategy that we own in our portfolios – the top 100 companies represent about a third of its corporate book.

Elsewhere, the ECB board member, Frank Elderson, in a speech last June highlighted the need for more work on data (Elderson’s full speech, ‘Patchy data is a good start – from Kuznets and Clark to supervisors and climate’ is available by clicking here.)

Conclusion

If climate risk is still the ‘dark matter’ in European bank financial models, the good news is that at least the financial institutions now know what they don’t know. Based on ECB data,2 about 90% of banks admitted to being only part- or not-at-all-aligned with the climate-risk reporting standards:

- over half of banks under the aegis of the ECB have no formal climate risk-assessment process;

- only 40% have identified explicit executive responsibility for managing risk; and,

- only 25% report on climate-risk to the management board.

Despite the poor baseline situation, bank and corporate environmental risk disclosure will inevitably improve under the push of regulations and the pull of investor demand for climate-related information.

Full climate-disclosure will require banks to carry out the challenging task of evaluating environmental risks in their loan and investment portfolios with the reward of long-term financial resilience through a period of accelerating planetary change.

Introducing climate-reporting into the financial universe could also bring about a broader revolution in how we understand the gravity of risk; the ‘dark matter’ dangers that lie beyond the bottom line are real, even if we can’t see them yet.

1“Key elements of the 2021 Biennial Exploratory Scenario: Financial risks from climate change,” published by the Bank of England in June 2021. See: https://www.bankofengland.co.uk/stress-testing/2021/key-elements-2021-biennial-exploratory-scenario-financial-risks-climate-change.

2“Frank Elderson: Patchy data is a good start – from Kuznets and Clark to supervisors and climate,” published by BIS in June 2021.