At the end of May 2023, the Federated Hermes Asia ex-Japan Strategy’s key country active overweight remains Korea, at +13.96% relative to benchmark, whereas the strategy’s main underweight is India, sitting at 16.83% below the benchmark, as shown by Figure 1 below.1

We prefer Korean stocks because they currently present very cheap valuations amid improving corporate governance laws, as authorities seek developed market status. In our view, Indian stocks remain too expensive despite a good long-term outlook. We are overweight China, believing that the geopolitical risks presented are worth taking given valuations, and are underweight Taiwan believing that the semiconductor cycle for logic has peaked.

Figure 1: Federated Hermes Asia ex-Japan, country active weight (%)

Bad news equals attractive valuations

Over the past decade, Korea’s stock market has underperformed the MSCI AC Asia ex-Japan IMI Index and several major sub-indices (including India and Taiwan), and has lagged behind other developed markets. In 2022, it was the worst performing market in the Asia ex-Japan region.2

As contrarian investors, we seek unloved companies in unloved markets. Korea is a market that tends to rise and fall quite sharply, and, when prices do fall, they tend to fall very low. Right now, earnings and revenues are depressed, but market participants are reminded that, often, ‘bad news’ can actually equal good news for investors, as any rocky periods tend to be transient and can be softened by very attractive prices.

As contrarian investors, we seek unloved companies in unloved markets.

It is perhaps unsurprising, therefore, that Korea has been a more permanent overweight in the Strategy since its inception. Korea is at 28.8% exposure at present, which is more than double the 13.96% index weight. Today, it is our biggest relative overweight position because we see a compelling opportunity in the region. This is because, despite suppressed valuations last year due to regional pressures, Korea has none of the idiosyncratic or geographic pressures of its neighbours.

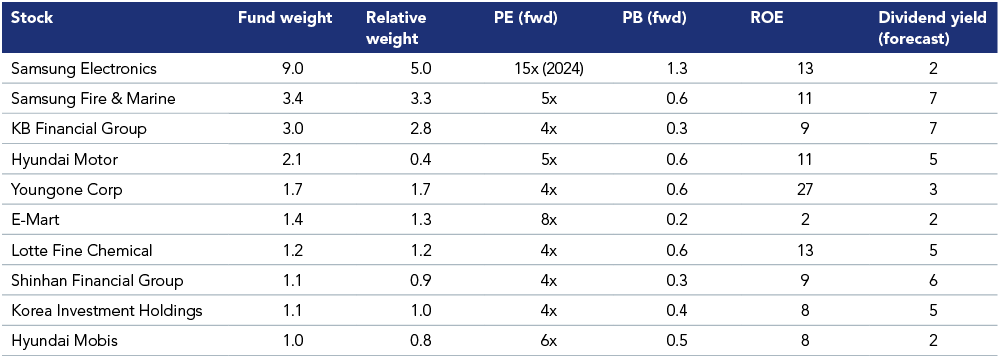

This is also evidenced by our top-10 Korean stock positions3, where Korean powerhouse Samsung is the largest individual bet, accounting for a 8.98% position versus an index allocation of 3.97%. It trades on a price-to-earning of 16x, which, while optically not cheap, is comprised of depressed earnings trading on 1.3x price book, with a third of its market cap in cash.

- Samsung is a globally competitive company; the number one in memory, number one in smartphones (in terms of market share), and a global leader in appliances and display trading at near-book value.

- KB Financial Group is the number one bank in Korea, with price-to-earnings (P/E) of 4x, price-to-book (P/B) of 0.3, dividend yield (DY) of 7%, and return-of-equity (ROE) of 9%.

- Samsung Fire & Marine, is the number one general insurer in Korea, which should benefit from rising rate environment, and trades on PE of 5x, PB of 0.6, DY of 7%, and ROE of 11%.

- E-Mart, is the number-one offline retailer, and number two online. The company trades on PE of 8x, 0.2x PB, and ROE of 2%.

The above does not represent all of the securities held in the portfolio and it should not be assumed that the above securities were or will be profitable. This information does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.

The reason we are overweight Korea is tactical, as it has always been cheap and is a market where we have found some strong stock opportunities.

Figure 2: Top-10 Korean positions (Asia ex-Japan strategy)

Source: NT, Bloomberg as at 31 May 202. Hyundai Motor weights have been combined into one line. The above does not represent all of the securities held in the portfolio and it should not be assumed that the above securities were or will be profitable. This information does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.

Swim against the stream

We are often asked why it is we have such a large overweight in Korea, given the poor long-term track record of the market, and what makes us think things will change.

Firstly, in our view, the valuations in Korea are incredible. It is a unique market where you can find high-quality companies trading extremely cheap, and lower-quality (not low quality) companies at exceptional prices.

So, the question shouldn’t be why should Korea do well, but rather why should these companies do well. Firstly, Samsung is a global leader in every one of its segments and is priced as a value company, and, secondly, some of the cheaper names are priced at extraordinary value. So, that is why we think these names should do well.

Figure 3: Forward price-to-earnings ratio

Figure 4: Valuations

While valuations in Korea are extremely cheap (similar in this regard to China), we are able to invest without the same geopolitical risk. Of course, there is some risk due to the ongoing tensions with North Korea and the questions around corporate governance, but not to the same degree of risk as the geopolitical tensions that have tempered our overweight exposure to China.

By contrast, Korea has remained relatively stable and there is the possibility of a potential catalyst for the economy and global growth to improve. Not that we look for such a catalyst – our philosophy has always been to buy attractively-priced stocks, believing that the proverbial catalyst will emerge. The challenge with identifying a catalyst is that when it does become clear, generally, everyone else can see it as well, and so is therefore already reflected in the share price.

As contrarian investors, we see value through the earnings cycle and re-rating cycle. If you look at Korea, corporate earnings are cyclical, but investors can get exposure to structural growth like technology through industry-leading businesses which are innovating, improving, expanding and growing. We look to take advantage of the earnings cycle to buy companies when earnings are depressed and when companies are trading at a trough multiple. We then look to sell them when their share prices rerate at the peak of the earnings cycle.

Learn more about our Asia ex-Japan strategy.

For further insight on Asia, please watch our video insight: Crouching tiger – the contrarian case for China.