Almost two years ago, Andrey Kuznetsov, Credit Portfolio Manager and Audra Stundziaite, Senior Credit Analyst, at Hermes Investment Management, argued that the market for European hybrids was attractive for both issuers and investors. Today, they revisit the case for hybrids and ask: in the growing global hybrid market, where is the relative value?

In 2016, we argued in favour of an increased allocation to the European hybrid market in an issue of our quarterly commentary Spectrum, “Putting two and two together: how hybrids can add up for investors.” The central premise was that hybrids were attractive for investors due to the inherent investment benefits they offer and a supportive economic backdrop1.

Today, there is still value to be found in the hybrid market. Following the recent market tumult and underperformance of investment-grade credit, we believe it is an appropriate time to revisit the case for corporate hybrids.

European issuance continues apace

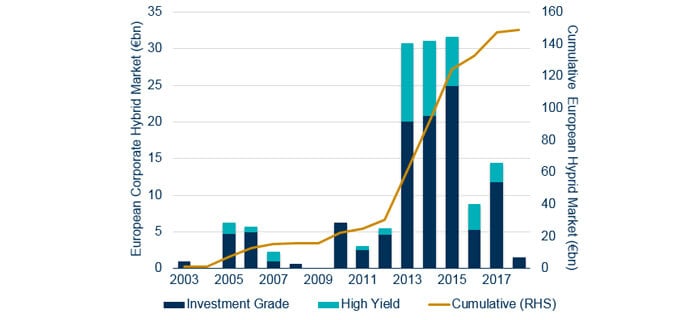

Since our 2016 commentary, hybrids have become much more mainstream buoyed by an increased appetite for – and understanding of – the asset class. Moreover, European corporate hybrid issuance has continued to increase amid an improving economic outlook, the ECB’s extension of its QE programme, strong fundamentals, and an increased awareness among investors about hybrid securities. To date, the cumulative European hybrid market issuance stands at around €150bn.

Given these favourable credit characteristics, European corporate hybrids have generally continued to outperform senior debt. Their pick-up, in basis points, relative to senior spreads has fallen from a peak of low-400s on high-yield hybrids and high-200s on investment-grade hybrids in 2016 to mid-100s and low-100s respectively in early 2018. Moreover, European corporate hybrids that were eligible for call in 2016 and 2017 were called on their first call date.

Figure 1: The European corporate hybrid bond market has continued to grow since 2016

Hybrid issuance by North American midstream companies accelerates

Across the Atlantic, there has been a significant uptick in the issuance of hybrids by North American midstream energy companies. In the second half of 2017, US midstream companies issued about $8bn of hybrid securities. Indeed, US hybrids have become a more attractive way to obtain funding following a tumultuous year for midstream equities. In the last 12 months, US midstream equities underperformed the broader market by more than 30%. This underperformance can largely be attributed to:

- Lower growth prospects for the maturing North American energy infrastructure industry, as much of the pipeline network in the region have now been developed;

- Corporate governance concerns, as most midstream companies operate under Master Limited Partnerships (MLP) – that is, a limited partnership that is traded publicly on an exchange;

- Rising interest rates; and

- Last month’s announcement by the Federal Energy Regulatory Commission that it will “no longer allow MLPs’ interstate natural gas and oil pipelines to recover an income tax allowance in the cost of service »2.

Nonetheless, we are fundamentally constructive on US midstream credits as we believe that they have stable business models due to lack of direct commodity exposure in their contracts. Moreover, midstream companies generally employ conservative financial policies, which are consistent with investment-grade companies, while long-term take-or-pay contracts eliminate volumetric risk and the current macro backdrop remains supportive, with hydrocarbon production rising in North America.

Energy exposure: an attractive relative value opportunity?

From a relative-value perspective, US midstream hybrids issued by investment-grade entities generally trade at a zero-volatility spread3 of about 345bps, 230bps relative to senior debt, and with a sub-senior multiple of 2.9x. This compares with a spread differential of about 140bps on European corporate hybrids, an average of 230bps on high-yield bonds (BB-rated), and 415bps in high-yield energy bonds (B1/B2-rated).

It is our view that midstream companies’ business models offer investors exposure to the energy sector, but with less beta than riskier high-yield upstream companies. As such, we think that some investment-grade midstream hybrids in the North American market are attractive. One such example is current holding Enbridge.

Enbridge: an energetic performer

North American pipeline company Enbridge has been active in the hybrid market. The Calgary-based firm, which has more than 18,000 miles of liquid pipelines, acquired Spectra Energy last year, in a deal valued at about $28bn. The company’s credit profile benefits from its size and scale, commitment to de-lever and its EBITDA is expected to hit $9.6bn this year.

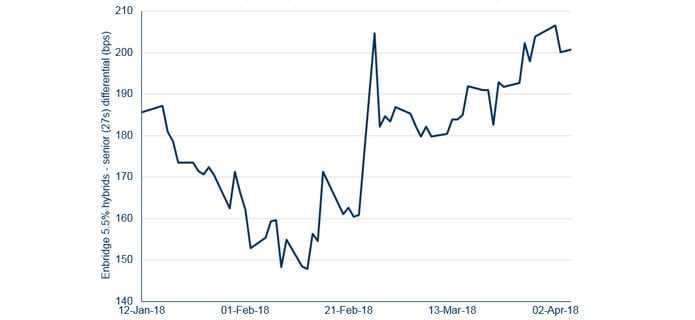

To fund its capital needs, Enbridge entered the hybrid market. Currently, the group’s hybrids trade at 340bps, 205bps relative to senior debt and with a hybrid-senior ratio of 2.5x. Enbridge’s hybrids are expected to be called on their first call date, thereby reducing extension risks and offering additional protection for investors. That’s because Enbridge’s hybrids have coupon ‘step-ups’, which increase interest rates to the issuer if they are not called at the call date.

Figure 2: Enbridge hybrids offer an attractive spread is active in hybrid markets

Source: Hermes Investment Management as at April 2018

Tapping into the North American midstream

Since our initial commentary in 2016, it is evident that the global hybrid market continued to offer robust returns on both sides of the Atlantic.

At Hermes, we continue to seek the most attractive debt instruments in corporate capital structures worldwide. And in doing so, we believe US midstream hybrids should not be overlooked.

2 “FERC revises polices, will disallow income tax allowance cost recovery in MLP pipeline rates,” published by the FERC on 15 March 2018

3 A zero-volatility spread is the constant spread that makes the price of a security equal to the present value of its cash flows.