The story of Evergrande’s default is more than a tale of a single real estate developer crumbling under the weight of its own debt. It is, instead, the story of a company caught in the crossfire between China’s past and future.

Should foreign investors be concerned?

In markets, size matters. Evergrande has RMB 2.3trn of assets on its books, which is equivalent to 2% of China’s GDP1. The company employs 123k employees and has 3.8 million contractors 2. Its eventual default will undoubtedly impact a multitude of partners, including construction and design firms, materials suppliers and other agents. Many buyers who purchased property from Evergrande off plan will potentially lose money as will direct investors in its shares and bonds.

While most foreign investors do not fall into any of the above categories, Evergrande matters for one important reason: contagion. While China’s economic growth rate has been slowing for several quarters, the evolving situation will undoubtedly harden the landing. For global markets, this is likely to be manifested, first, in slower demand, particularly among sectors that are most closely tied to Chinese growth, such as steel and copper.

This fact has inevitably worried investors, and equity markets across the world sold off in the immediate aftermath of last week’s news. But the sell-off was, in our view, a knee-jerk market reaction to an unexpected event rather than a considered response to the fundamentals. It is also worth noting that many of the companies in question declined from well above their long-term trend lines with investors clearly looking for a good opportunity to take risk off the table. Evergrande provided that opportunity.

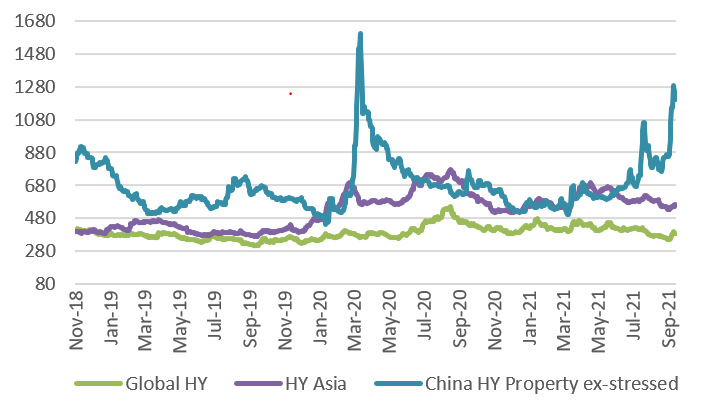

Figure 1. Global & Asian HY vs. China HY Prop - Trading Data - 3year

Past performance is not a reliable indicator of future performance.

That said, considering the inherent opaqueness of the Chinese market, we do not rule out any larger regional impact. There may be, for example, many risks related to shadow banking and off-balance-sheet liabilities that the broader market does not yet know about. Evergrande’s impending bankruptcy will be a lengthy affair and we will certainly see some surprise lenders in this process – i.e. companies that markets didn’t think had exposure to Evergrande but do, and this could result in a few unexpected casualties as the process unfolds. We believe, however, that this will remain contained under our base case scenario of an “administrative support” programme implemented by the government.

So what is likely to happen next?

Our base case scenario is for an orderly default to take place, facilitated by the Chinese government. We expect this facilitation to take the form of administrative rather than financial support.

We have reached this conclusion based on a range of government driven action over recent days, including the centralisation of all court cases against Evergrande which could prevent local courts from freezing its assets. Minsheng, Zheshang, Shanghai Pudong Development Bank all agreeing to extend some project loans which would help to slow the negative downward spiral and avert a fire sale.

So while the Chinese government is likely to allow Evergrande to fail, we agree that it will do so in the manner of a ‘controlled explosion’. China’s leadership values order above all else, and we believe it is working behind the scenes to limit the social and economic domino effect of the company’s demise. Authorities have a myriad of tools at its disposal to help it ‘disperse’ the impact of the collapse and manufacture stability. For example, we expect to see some companies asked to take over uncompleted Evergrande projects, while more banks will be instructed to extend loans to companies hit by the contagion. Doing so will achieve two things for the government: it will avert a crisis and it will weaken the future profitability of other companies in the sector triggering a much-needed cooling effect. In short, China will trade a crisis for a slowdown.

For now, while the bulk of the tail risk lies with the region’s developers, we believe this event will fundamentally reshape the market reliance on a pre-sale funding model and mark the end of the era of stellar growth in the Chinese property market.

An era-ending default

The prospect of the Chinese government allowing a company of Evergrande’s size and footprint to fail, would have been unheard of just five years ago. Today, Evergrande stands in the crosshairs of China’s demographic shift, its urbanisation and property boom, and the end of its decade-long economic growth spurt. In addition, increased personal wealth has seen property investment soar towards bubble territory.

In managing Evergrande’s exit from the market, the Chinese government is asserting its commitment to its so-called three red lines. These are the main tools of China’s effort to cool the property market against the backdrop of an aging population, slowing birth rates and a small-family culture that endures despite the end of the one-child policy. Amid signs of sector overheating, China introduced the red lines last September and developers that fail to meet one, two, or all of the ‘three red lines’, would face limits on their ability to grow their debt.

These stringent measures were accompanied by curbs on bank lending. It is ultimately all of these things – from demographics to regulation, speculation and growth – that caught up with Evergrande in the end.

Our view

We expect Evergrande to ultimately file for bankruptcy in the coming weeks. However, the contagion will be limited both globally and domestically by virtue of the Chinese authorities’ absolute power and willingness to pull whatever levers it needs to avert instability. Numerous companies across the mainland and beyond will be used to absorb the shock and spread-out the impact. While the opaqueness of the Chinese market means that interconnections are harder to predict, we can confidently say that Evergrande is far from China’s ‘Lehman event’ as some commentators have suggested.